In March 2026, as the escalation of the Iran-Israel conflict drives up the energy geopolitical risk premium, the Korean semiconductor sector (represented by $EWY), along with Samsung and SK Hynix, has once again faced emotional sell-offs triggered by the "Hormuz Black Swan" narrative and fears of an energy crisis. This should be viewed as a golden buying opportunity for Samsung and SK Hynix — the selling is primarily clearing out leveraged positions and panic sentiment, without altering the fundamental demand picture. Here are the reasons:

The complete official 2025 LNG import data for South Korea was just released at the end of January by MEES (Middle East Economic Survey), based on Korean Customs/KOGAS/KESIS figures. Total imports reached a record 46.72 million tons (+1% YoY).

- Australia: 14.68 million tons (all-time high, +29%), accounting for 31.4% (a new record high, and the main route avoiding the Strait of Hormuz).

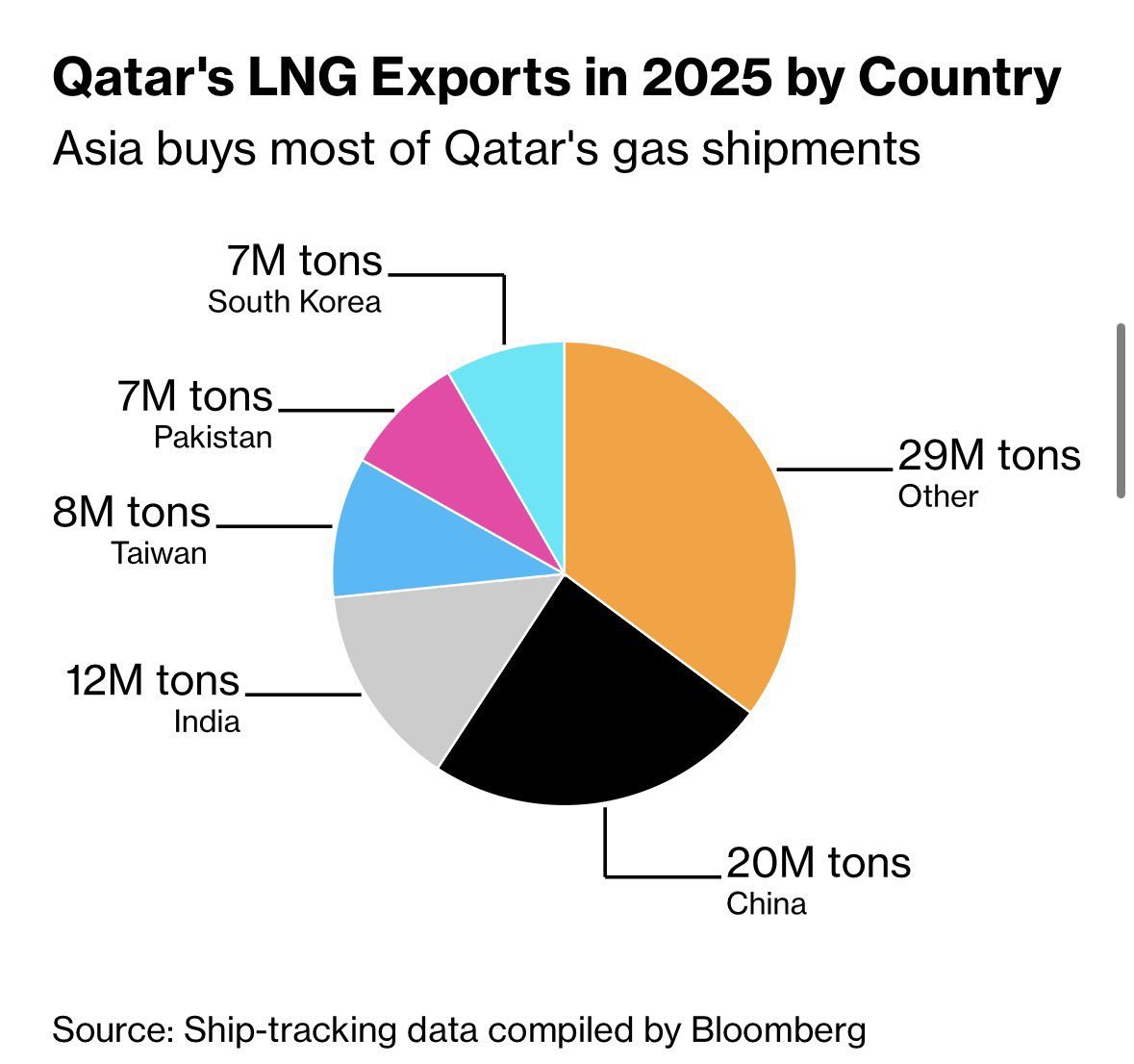

- Qatar (via Hormuz): 6.97 million tons (-22%, a 16-year low), with the Middle East/MENA share continuing to decline sharply.

Overall, routes avoiding the Strait of Hormuz still account for more than 80% (Australia + Malaysia + Indonesia + US + Russia, etc.), and the proportion of long-term contracts remains high (no exact new 2025 figure, but the trend aligns with 2024's 82%).

This demonstrates that South Korea's "energy firewall," rapidly built since the 2022 Russia-Ukraine conflict, is effective — with 80% of LNG imports routed away from Hormuz, 82% locked in via long-term contracts, and diversified sources (Australia + US + Indonesia + Russia together exceeding 60%). This has effectively shifted any potential cost shocks to AI hyperscalers rather than Korean companies' own OPEX.

As global duopolies in HBM/DRAM/NAND, SK Hynix and Samsung Electronics are benefiting from structural AI compute demand (with pre-order phenomena reappearing). Their pricing power and capacity expansion far outweigh short-term crude oil/LNG volatility. They are now entering a true upcycle phase, and market expectations of massive profits by 2028 further highlight the overwhelming advantage of the "demand black hole" over supply. While a few reminders about bottlenecks like helium are worth monitoring, these are supply-chain details rather than systemic risks.

Since the 2022 Russia-Ukraine war, South Korea's energy firewall (diversification + long-term contracts + government buffers) has proven its resilience. Sell-offs similar to the DeepSeek-Nvidia panic are typically windows for deleveraging, not reversals in logic.

In the long run, the geopolitical irrelevance of AI compute demand far outweighs sensitivity to energy fluctuations: Korean semiconductors are not "energy-vulnerable entities" but "rigid-demand beneficiaries."

Ultimately, this once again confirms that assessing geopolitical resilience in the AI industry chain must go beyond index weights and headline narratives. What truly determines winners are contract lock-ins, diversification execution, and downstream demand stickiness. During periods of high volatility, investors should prioritize data-driven logic — as Korean semiconductors have proven through real actions, strategic foresight outperforms panic reactions in navigating black swans. Short-term geopolitical fluctuations may push up spot prices, but long-term contracts + diversification keep the fundamentals of the Korean semiconductor sector rock-solid. This pullback remains an emotional washout, and we hope it turns into a golden pit for the memory/HBM industry going forward.

#SamsungElectronics #samsung #SKhynix

From X

Disclaimer: The above content reflects only the author's opinion and does not represent any stance of CoinNX, nor does it constitute any investment advice related to CoinNX.