Notes

미국 프리마켓 특징주, 이슈

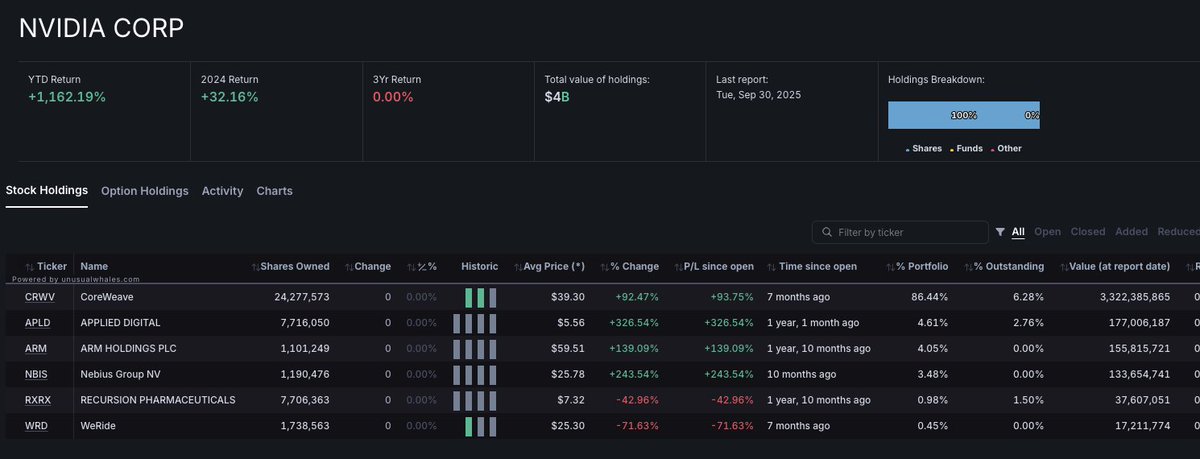

• $NVDA +0.30%

: 중국, 빠르면 이번 분기 내 일부 H200 칩 구매 승인 예정

• $JEF -2.75%

: 실적은 호조였으나, 투자자들은 First Brands 익스포저 관련 손실에 주목

• $STZ +2.0%

: 시장 예상 상회 실적 발표

• $APLD +4.6%

: 조정 EPS 및 매출 모두 예상치 상회

• $RTX +4.5% / $LMT +7.9% / $NOC +8.4%

: 트럼프, 국방 예산을 기존 1.0조 달러 → 1.5조 달러로 증액해야 한다고 발언

• $ABBV -1.1%

: 연간 조정 EPS 가이던스 하향

: $RVMD -7.3%, 인수설 부인 영향

• $GOOGL +1.1%

: Cantor Fitzgerald, 투자의견 ‘중립’ → ‘비중확대’ 상향

• $MQ -9.5%

: Mizuho, 투자의견 ‘시장수익률 상회’ → ‘중립’ 하향

• $AA -4.0%

: JPMorgan, 투자의견 ‘중립’ → ‘비중축소’ 하향

• $NKE -1.1%

: Needham, 투자의견 ‘매수’ → ‘보유’ 하향

MTS, @MSX_CN 로 국장, 미장 깔짝깔짝

50 minutes before market closed on Friday, $APLD whale purchased over $187k worth of the 10 calls expiring 7/18exp. Looks like they rolled to the 12 calls

$APLD by the way is up over 52% today

Great flow @unusual_whales

MORNING BID

🔸 $CVGW: Q4 EPS 5c vs. -2c last year; revenue up 19.5% to $170M vs. $161.93M est.; adj EBITDA $6.7M.

🔸 $GM: Multi-year deal with Vianode for synthetic graphite for EV batteries.

🔸 $TSLA: SEC sues Elon Musk for late disclosure of Twitter stake in 2022.

🔸 $VAL, $RIG, $NE, $HP, $SLB, $NOV: Downgraded to In Line from Outperform by Evercore/ISI.

🔸 $Oil Market: IEA reports 2025 oil surplus at 725k b/d, down from 950k b/d.

🔸 $Aluminum: Prices up slightly; EU eyes import limits from Russia, China's growth slows.

🔸 $PKE: Q3 EPS $0.08, sales $14.4M.

🔸 $BK: Q4 adj EPS $1.72 vs. $1.56 est.; AUM $2T; fee revenue +9% to $3.51B; net interest +8% to $1.19B; AUC/A $52.1T, up 9%.

🔸 $BHLB: Files for offering of up to 3.45M shares.

🔸 $BLK: Q4 adj EPS $11.93 vs. $11.22 est.; revenue +23% to $5.68B; AUM record $11.55T; operating margin 45.5%; $281B inflows Q4.

🔸 $DFS: Charge-off rate 2.55%, delinquency rate 1.76% at Dec 2024.

🔸 $JPM: Q4 EPS $4.81 vs. $4.04 est.; revenue $42.8B; charge-offs 1.63%, delinquencies 0.84%; FICC trading $5.01B vs. $4.37B est.; credit loss $2.63B; ROE 17%, ROTCE 21%; $486B inflows 2024.

🔸 $WFC: Q4 EPS $1.43 vs. $1.35 est.; net interest $11.84B; revenue $20.38B; commercial banking $3.17B, investment banking $4.61B, wealth management $3.96B.

🔸 $KROS: Paused dosing in TROPOS trial for pulmonary hypertension due to pericardial effusion concerns in safety review.

🔸 $VCEL: Lowers FY24 revenue forecast to $237M-$237.5M from $238M-$242M; raises gross margin to 72.5%; maintains EBITDA margin at 22%; Q4 revenue expected at $75.2M-$75.7M, under consensus.

🔸 $APLD: Q2 adj EPS ($0.06) vs. ($0.15) est.; EBITDA $21.4M vs. $19.68M est.; revenue $63.9M; cloud services +523% to $27.7M.

🔸 $PI: Maintains Q4 revenue and EBITDA guidance; expects EBITDA $13.6M-$15.1M, revenue $91M-$94M.

🔸 $LRCX: Downgraded to Peer Perform from Outperform by Wolfe Research.

🔸 $LASR: Q4 revenue forecast $46M-$48M, below $52M est.; lower than expected margins and EBITDA.

🔸 $MGNI: Expands partnership with Samsung Ads for programmatic ads in Southeast Asia.

🔸 $S: Downgraded to Neutral from Buy by UBS.

🔸 U.S. Policy: New regulations planned to limit chip exports to China from TSMC, Samsung, and others.

MORNING BID

🔸 $ACMR: Raises 2024 revenue forecast to $755M-$770M from $725M-$745M; sees 2025 at $850M-$950M vs. consensus $902.95M.

🔸 $APLD: Shares up 30% after Macquarie's $5B investment for 15% stake in AI data centers.

🔸 $AVGO: Secures $7.5B five-year credit facility.

🔸 $IAC: To spin off $ANGI stake to shareholders; Joey Levin steps down as CEO.

🔸 $TTAN: Q3 revenue $199.3M; Q4 expected at $199M-$201M vs. consensus $193.58M; FY25 revenue projected at $761.6M-$763.6M vs. consensus $755.37M.

🔸 $DHR: Q4 revenue expected to rise by low single digits year-over-year.

🔸 $INGN: Q4 revenue forecast at $79.0M-$80.0M, above $73.9M estimate; FY24 revenue guidance raised to $334.5M-$335.5M from $329M-$331M, vs. $329.62M consensus.

🔸 $KIDS: Q4 revenue at $52.7M vs. $50.73M estimate; FY25 revenue guidance $235-242M vs. $239.95M estimate, adjusted EBITDA $15-17M vs. $20.14M forecast.

🔸 $RGNX: Stock up after deal with Nippon Shinyaku for gene therapies; $110M upfront and potential $700M in milestones.

🔸 $TDOC: New partnership with $AMZN to broaden access to chronic care programs.

🔸 $RILY: Shares rise after Q2 2024 report showing a $14.35 per share net loss, delayed due to Franchise Group issues; expects normal filing schedule in 2025.

🔸 $AB: AUM fell to $792B in December 2024 from $813B, a 2.6% drop due to market and outflow issues.

🔸 $IVZ: AUM dropped to $1,846B, down 0.6% with $12.6B in net long-term inflows but $42B reduction from market returns.

🔸 $VRTS: Total client assets at $177.3B in December 2024, down due to outflows and market performance.

🔸 $URI: Acquiring $HEES for $92/share, valuing the deal at $4.8B including debt.

Insurance Industry: LA wildfires might cost insurers over $30B, with significant damage from Palisades and Eaton fires.

🔸 $AVAV: Secures $55.3M order for Switchblade Systems under U.S. Army's LUS program.

🔸 $CE: Upgraded to Buy from Underperform by Bank of America on valuation.

🔸 $FANG: Q4 unhedged prices at $69.48/bbl oil, $0.48/mcf gas, $19.27/bbl NGLs; hedged prices at $68.72/bbl oil, $0.82/mcf gas, $19.27/bbl NGLs.

🔸 $WAB: Agrees to purchase Evident's inspection tech division for $1.78B.

🔸 $KBH: Q4 EPS $2.52 vs. $2.45 est., revenue $1.999B vs. $2.008B est.; FY25 housing revenue guidance $7.00-7.50B, avg selling price $488-498K.

🔸 $NOMD: 2025 organic revenue growth expected at 1%-3%; confident in meeting 2024 guidance.

🔸 $SIG: Q4 adj. operating income forecast at $337M-$347M, below previous $397M-$427M; sales expected at $2.32B-$2.34B, under prior $2.38B-$2.46B.

🔸 $ADM: Downgraded to Underperform from Neutral by Bank America.

🔸 $LVS: Downgraded to Equal Weight from Overweight by Morgan Stanley.