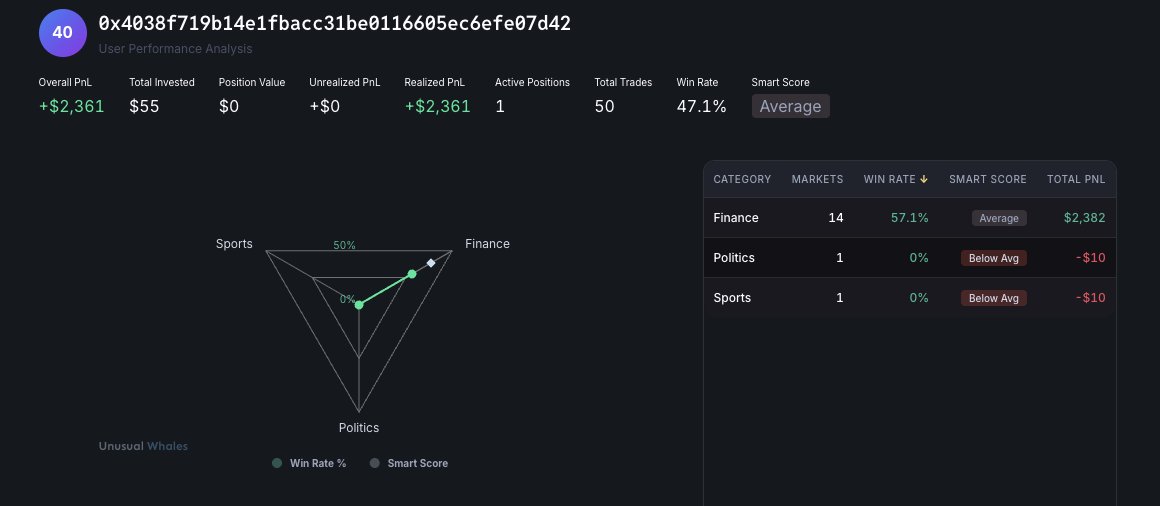

Notes

Woah, look at this.

There is a group of wallets that has bet on earnings of $HD, $DASH, $KMX, $THO and $SNEX, per EventWavesIO.

They often only have that ONE position.

All of these companies are reportedly audited by KMPG.

What do they know?

See one of the wallets below: https://t.co/oyHGMFuPnu

亲爱的,新的一星期开始啦!你有什么新的规划吗?

自从 #Bitget 平台的股币交易功能越来越完善之后,月光最近确定了一件事

2026 年,美股会变成币圈人的主流交易资产之一

Bitget 的链上美股已经支持 200+ 美股资产,用起来是真的省事

而且,手续费低,操作又很顺

也不用海外开户、不用处理复杂的税务

现在已经有 100 万用户在上面交易美股了!

🔗还没有BG账号的宝子,赶紧点击注册:https://t.co/BSPjRBNtdY

同时,用 Bitget 直接就能买美股和 ETF,特别方便

🔗传送门:https://t.co/4oYy39B3R5

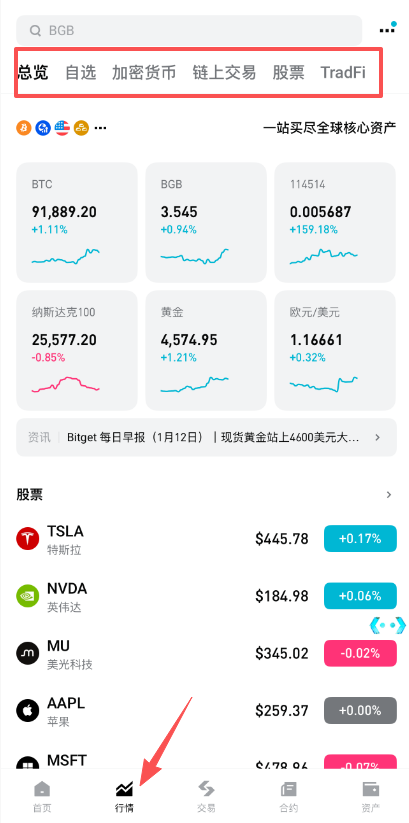

这次 @Bitget_zh @BitgetTC 又新上了 98 个资产,阵容很能打

美股主流包含

$TMUS $HD $SOFI $BAC $XOM

中概股则是有

$BILI $PDD $TCOM $NIO $LI $NTES

加上ETF

$TQQQ $SQQQ $USO

最近道琼和标普500 双双新高,从趋势可以看出来,AI + 芯片依然是主线:Google 、美光 、英特尔 继续强

军工、能源、太空也在轮动,例如 $ONDS ,最近直接 +20%

预测一下, 2026年,几个赛道还是很火热

尤其是AI、高端制造、能源转型、高股息 & 低估值的公司

无论你是不是已经在车上,美股这条线,2026 年真的不能缺席呀!

最近美股市场持续火热,道琼斯和标普500指数双双创下历史新高。📈

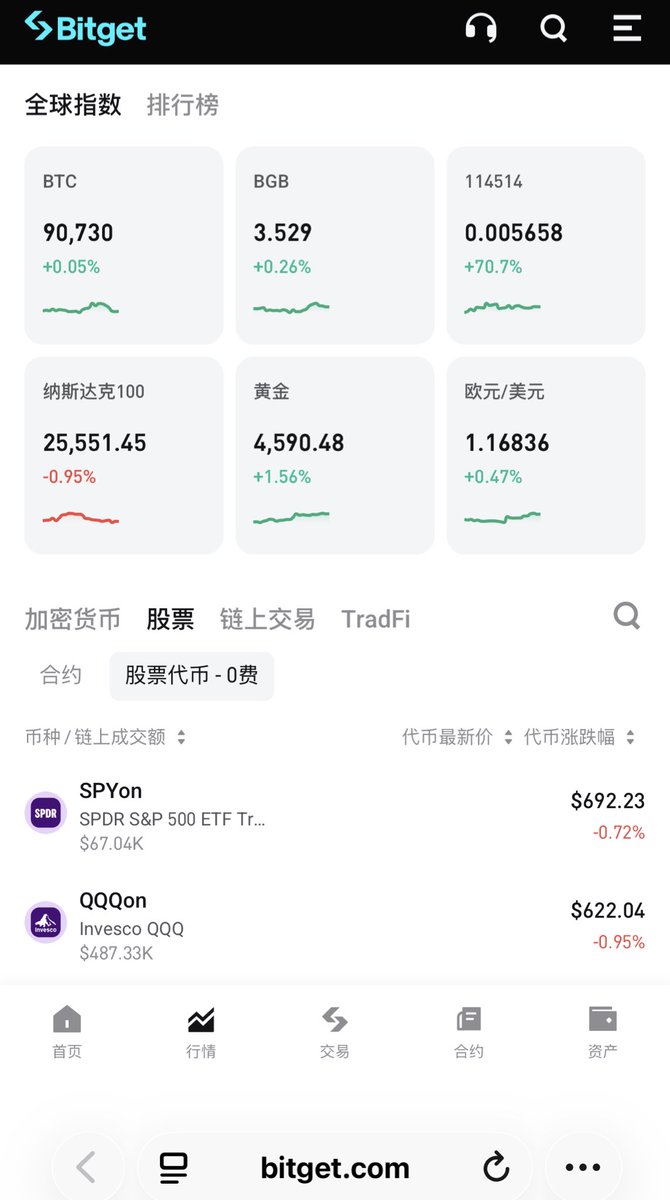

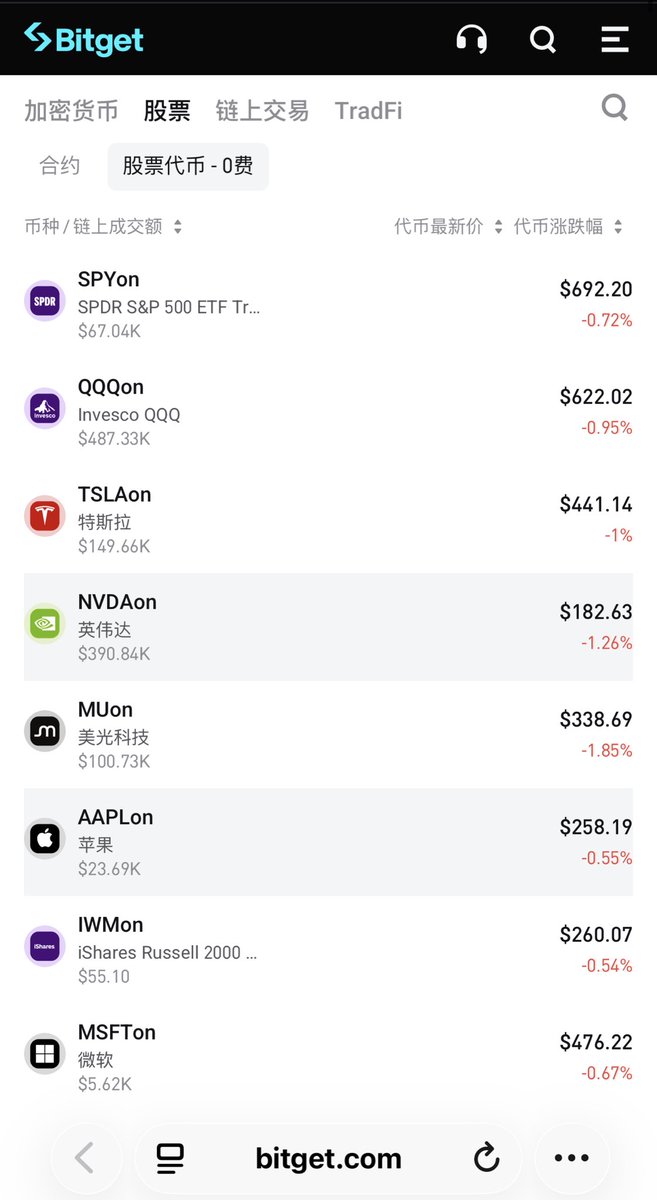

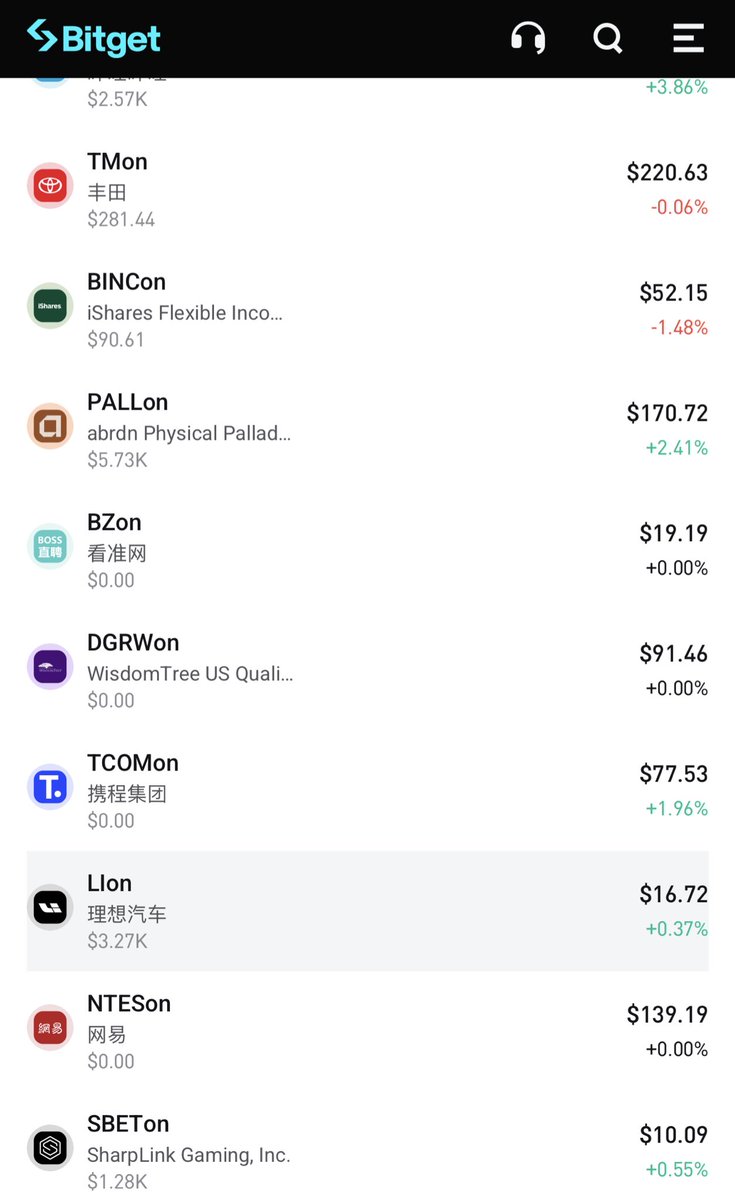

#Bitget 在这个风口下,通过与Ondo的深度合作,从去年年底上线美股交易后,最近又继续新增 98 个美股和 ETF,总数突破 200 个,而且已经有 100 万用户在平台交易股票了。 @Bitget_zh

以前要买美股,得开美股账户,填各种表格,还要考虑资金进出 、税务等问题,特别麻烦。

现在直接用 USDT 就能直接在Bitget购买代币化的股票,而且开户便利、无税务负担、操作丝滑。

本月还是「美股狂欢月」,股票代币交易限时0手续费。

🌟这次新增的资产覆盖面很广:

• 美国主流公司: $TMUS $HD $SOFI $BAC $XOM

• 中概股: $BILI $PDD $TCOM $NIO $LI $NTES

• ETF:$TQQQ $SQQQ $USO

• 黄金、原油、稀土等大宗商品ETF

对于我这种不想开通各种账户又想参与到多种资产配置的web3用户来说,实在太方便了 !

最近行情那么好,所以宝子们有什么不错的股票或者ETF推荐嘛?!🤔

参与路径我也附在下图了👇:🔗https://t.co/7yp5Q70UW7

#Bitget 美股版图进一步完善,目前支持的美股已超过200个。很显然,你来BG 交易美股的原因是👉开户便利、无税务负担、低费用、操作丝滑!

用户需要什么,Bitget 上什么。这次一口气上了98个新资产,包括中国股民关注度最高的几只中概股:拼多多、携程、蔚来。还有这几年的高成长性躺平之选TQQQ。

美股0手续费活动持续到本月16日,欢迎体验!

RECAP

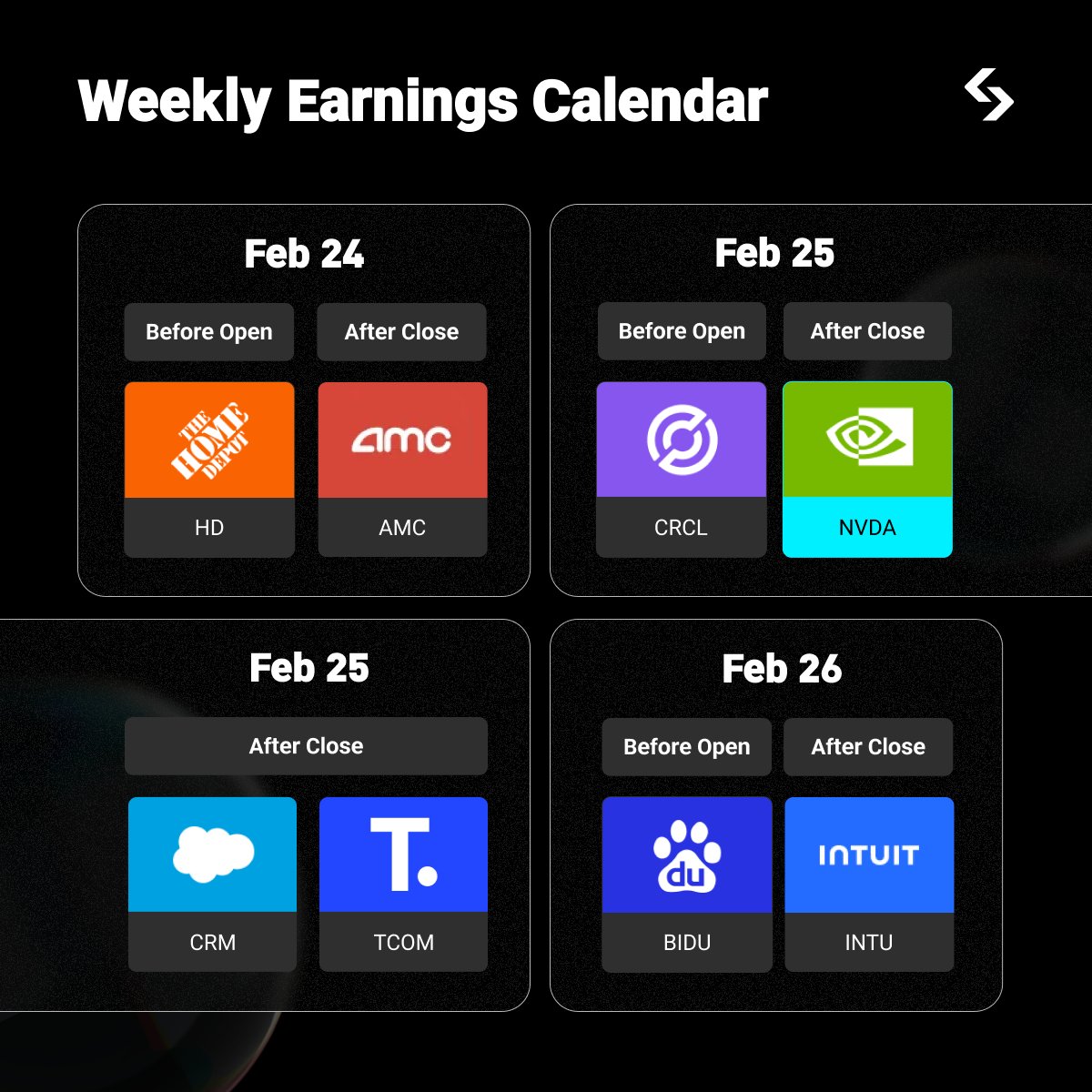

• $HD: Q3 EPS $3.78 vs. $3.65 est., revenue up 6.6% to $40.22B. Comp sales down 1.3%, better than expected. Raised FY24 sales forecast to 4% growth.

• $BABA: Strong sales growth during Singles' Day, 45 brands hit over 1 billion yuan GMV.

• $LYV: Q3 operating income $909.8M vs. $856.6M est., revenue down 6.2% to $7.65B. Ticket sales for 2024 up 3%.

• $ONON: Q3 EPS CHF 0.16, below est. CHF 0.20. Sales CHF 635.8M, up from expected CHF 617.3M. Increased FY sales forecast.

• $VIK: Upgraded by Morgan Stanley due to robust cruise demand.

• $APAM: AUM as of October 31, 2024, was $162.8B, with $78.8B in Artisan Funds and $84.0B in other accounts.

• $AGO: Q3 EPS $2.42 vs. $1.42 est., revenue down 33% to $269M, premiums up 53% to $61M.

• $CNS: AUM decreased to $89.7B by October 31, 2024, from $91.8B, due to market depreciation and distributions.

• $IVZ: AUM dropped to $1.772T, down 1.3%, with $2B in net inflows but losses from market returns.

• $JRVR: Q3 premiums grew 6%, with a high combined ratio of 136.1% but a better current year ratio at 92.6%.

• $RMR: Q4 EPS $0.34 below $0.40 est., EBITDA slightly above estimate at $21.8M.

• $HOOD: October showed 24.4M funded customers, $159.7B in assets, with significant growth in deposits.

• $VCTR: Reported AUM of $172.3B, total client assets of $176.5B for October 31, 2024.

• $ASRT: Q3 EPS $0.03 vs. ($0.05) est., EBITDA $5.3M vs. $4.7M est., revenue $29.2M vs. $28.87M est.

• $AZN: Upgraded full-year guidance due to strong Q3, expects high teens growth for earnings and revenue in 2024.

• $BAYRY: Stock dropped after forecasting lower earnings next year due to weak ag markets.

• $NGNE: Shares fell despite positive trial data for Rett Syndrome drug, due to an adverse event.

• $NVRO: Q3 EPS ($0.41) vs. ($0.81) est., improved EBITDA, raised FY revenue guidance.

• $STXS: Q3 EPS ($0.08) vs. ($0.05) est., revenue beat expectations, kept flat year-over-year revenue guidance.

IAC: Considering spinning off Angi, which IAC controls 85% of, valued at $1.25B, after exceeding Q3 revenue forecasts due to Dotdash Meredith.

• $IVAC: Q3 EPS loss was ($0.08) vs. ($0.15) est., revenue significantly beat estimates at $28.5M.

• $OKTA: Downgraded to hold by Deutsche Bank.

• $SE: Q3 EPS $0.24 missed estimates by $0.02, but revenue hit $4.3B, beating estimates.

• $ZETA: Q3 EBITDA $53.6M vs. $49.93M est., revenue $268M vs. $252.5M est., raised Q4 guidance.

#Upgrades - Oct 09, 2024

$AFRM: Morgan Stanley Upgrades to Equalweight from Underweight - PT $37 (from $20)

$HD: Loop Capital Upgrades to Buy from Hold - PT $460

$HON: CFRA Upgrades to Buy from Hold - PT $235

$INTR: JPMorgan Upgrades to Overweight from Neutral - PT $8.50 (from $7.50).

$LOW: Loop Capital Upgrades to Buy from Hold - PT $30

$LPLA: Wells Fargo Upgrades to Overweight from Equal Weight - PT $285 (from $235)

$LUV: Jefferies Upgrades to Hold from Underperform - PT $32 (from $24)

$MSCI: Redburn-Atlantic Upgrades to Buy from Neutral - PT $680

$RJF: JMP Securities Upgrades to Market Outperform from Market Perform - PT $146

$SAIA: Wolfe Research Upgrades to Outperform from Peerperform

$VLO: Wells Fargo Upgrades to Overweight from Equal Weight - PT $165 (from $172)

$VNET: HSBC Upgrades to Buy from Hold - PT $5.20

#Upgrades - Oct 02, 2024

$PARR: JPMorgan Upgrades to Overweight from Neutral - PT $30 (from $36)

$CVBF: KBW Upgrades to Outperform from Market Perform - PT $22 (from $20)

$TMP: KBW Upgrades to Outperform from Market Perform - PT $68 (from $59)

$BOH: KBW Upgrades to Market Perform from Underperform - PT $67 (from $60)

$HAFC: KBW Upgrades to Outperform from Market Perform - PT $22 (from $20)

$TOWN: KBW Upgrades to Outperform from Market Perform - PT $40 (from $35)

$RIO: Berenberg Upgrades to Buy from Hold - PT $79 (from $71)

$MTB: Evercore Upgrades to Outperform from In Line - PT $210 (from $187)

$HD: Gordon Haskett Upgrades to Buy from Accumulate - PT $450

$BAH: JPMorgan Upgrades to Overweight from Neutral - PT $170 (from $150)

$SAIC: JPMorgan Upgrades to Overweight from Neutral - PT $170 (from $150)

$FANG: Barclays Upgrades to Overweight from Equalweight - PT $210

$RRC: Barclays Upgrades to Equalweight from Underweight - PT $34

$DQ: HSBC Upgrades to Buy from Hold - PT $29.30

$SPHR: Wolfe Research Upgrades to Outperform from Peerperform - PT $60

$ULTA: UBS Upgrades to Buy from - PT $505

$CRM: Northland Upgrades to Outperform from Market Perform - PT $400