Notes

这两天一直在留意 $PAY Mint 的进度,说真的,节奏比我想的快得多。

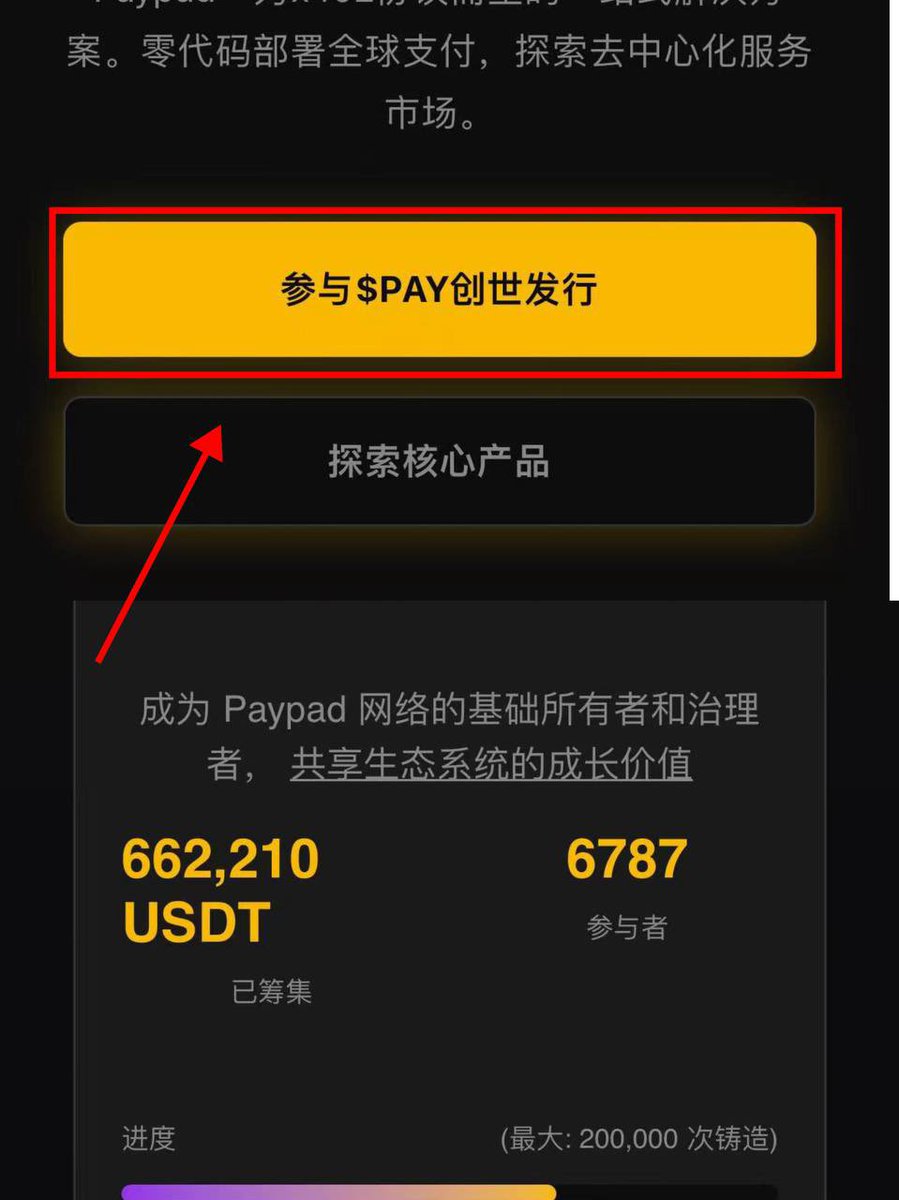

短短几个小时又进来四千多人,整个募资马上要摸到 200 万美金,有点像突然被点着了那种感觉。

我自己会关注,是因为它不是那种噱头项目,而是 @paypadxyz 把 x402 协议认真落在 BSC 上,让 AI agent 在链上“自动付钱”这件事真的能跑起来了。

以后 BSC 生态里那些 AI 代理要做无 Gas 的小额结算,路子基本都得从 $PAY 走过,这就是它被越来越多人盯到的原因。

为什么我觉得它空间不止 Ping 那个级别?

简单讲讲我自己的想法:

1. BSC 上的 AI 代理和微支付流量未来会很夸张,一天五亿美金的交易量并不难想象,而这些都是 $PAY 的通道价值。

2. $PAY 本身又是 Paypad 的平台币,手续费、平台权益、回购这些都会跟它绑定,

是有业务闭环的。

3. 项目团队资源不弱,现在已经能看到一些 VC 靠过来的迹象,这种级别的项目,未来上 Alpha 或合约都挺顺理成章。

AI + Web3 在 BSC 的节奏就像刚吹起的风,不一定要重仓,但这种底层能力型的机会,看看也不亏。

Mint 很简单,一次 10U:https://t.co/Rzp8UG3BQK

就当我今天随口跟你们分享一眼机会,

合不合适,你们自己心里都有数。

这两天一直在留意 $PAY Mint 的进度,说真的,节奏比我想的快得多。

短短几个小时又进来四千多人,整个募资马上要摸到 200 万美金,有点像突然被点着了那种感觉。

我自己会关注,是因为它不是那种噱头项目,而是 @paypadxyz 把 x402 协议认真落在 BSC 上,让 AI agent 在链上“自动付钱”这件事真的能跑起来了。

以后 BSC 生态里那些 AI 代理要做无 Gas 的小额结算,路子基本都得从 $PAY 走过,这就是它被越来越多人盯到的原因。

为什么我觉得它空间不止 Ping 那个级别?

简单讲讲我自己的想法:

1. BSC 上的 AI 代理和微支付流量未来会很夸张,一天五亿美金的交易量并不难想象,而这些都是 $PAY 的通道价值。

2. $PAY 本身又是 Paypad 的平台币,手续费、平台权益、回购这些都会跟它绑定,

是有业务闭环的。

3. 项目团队资源不弱,现在已经能看到一些 VC 靠过来的迹象,这种级别的项目,未来上 Alpha 或合约都挺顺理成章。

AI + Web3 在 BSC 的节奏就像刚吹起的风,不一定要重仓,但这种底层能力型的机会,看看也不亏。

Mint 很简单,一次 10U:https://t.co/Rzp8UG341c

就当我今天随口跟你们分享一眼机会,

合不合适,你们自己心里都有数。

$PING 这波暴冲带来的 x402 热度 是真看得见的。

我一直说——AI + Web3 的叙事,走到 可交付 / 可落地 / 有行业应用 这一层,一定会出现超越「只靠情绪」的叙事。

而 x402 这个协议,就是目前少数把 “AI可落地数据交互” 做到链上真能跑的那种脉络。

最近我看到很多地推圈子已经把话题转向 $PAY

BSC 上、基于 x402 协议的 AI 支付赛道龙头,

上线不到 24 小时,Mint 金额 50 万美金+ —— 在这种流动性都干掉一半的当前一级市场,这个数据真的算漂亮。

这种 “不是空 talk、不是纯情绪、不是 meme、是有协议 Underlay 的 AI 支付方向”

值得盯。

如果你想入场 Mint:

只需要 10 USDT 就能试水

Mint 教程:

1)准备 10 USDT

2)打开官网 https://t.co/ikmlKdCOsR

3)直接点击 Mint 按钮 就 Mint 成功

(不用复杂交互、不用填一堆表、没有奇怪流程)

专案方推特: @paypadxyz

AI Narrative 不是概念炒作的回马枪

而是下一阶段 Web3 能跑出 “真收入模型” 的那一条赛道

我反而觉得这种 “协议底→支付应用层→有真场景” 的 x402 线

比铭文那种纯 MEV 情绪周期

更像是能跑 6 个月甚至 1 年的叙事

$PAY

先研究、再决定要不要参与

但至少:这不是那种看了五秒就知道是垃圾的项目

这种题材

我是真的愿意花时间研究的

刚刚刷到@paypadxyz打新

感兴趣的朋友可以参加一下 👉 https://t.co/qOs2O0VIbd

玩法简单,10U打一次

热度还可以,现在参与了4000多个

Paypad x402 是一个 AI 代理经济基础设施平台,基于 BSC 链。核心功能:用 零代码工具 让 AI/开发者快速创建可收费的服务(Paypad Checkout)

构建 AI 服务市场(Paypad Market),用户和 AI 都能发现并付费使用

支持 机器间自动微支付(x402 协议)

代币 $PAY:平台结算资产,已于 11月1日 公平发射,现已超 40 万美元注入。

一句话:

让 AI 能自己赚钱的“支付+市场”一站式平台。

前几天的Base x402 真是火了一波,现在BSC 又来了个@paypadxyz ,使用Bsc 402架构补全 BSC AI 支付短板,是唯一原生 x402 协议

✅ 零代码部署 x402 端点

✅ $PAY 唯一结算币,后台强制兑换

✅ 单笔成本 0.0006 USDC,比 Base 能打

✅11月1号早上10:00开始铸造

🔥 $PAY Mint 教程:准备好 10 USDT,打开官网:https://t.co/c3MLnkmgvK直接点击 Mint 按钮

兄弟们顺手做一下 @okxchinese 和 Astra 500K $PAY 奖励活动

🔗完成任务

为 5,000 名获奖者提供 500,000 个 $PAY 代币。完成以下任务即可获得资格。

总共将选出 5K 名获奖者,每位获奖者在 TGE 后将获得 100 $PAY。

RECAP

• $CAVA: Q3 EPS $0.15, above expectations of $0.11; sales up 39% to $243.8M; FY guidance for restaurant comp sales at 12.5%, up from 8.5-9.5%, and EBITDA at $123M. Plans to increase restaurant openings and margins.

• $FLUT: Q3 adjusted EBITDA up 74% to $450M; revenue up 27% to $3.25B; raised full-year forecasts for EBITDA and revenue, expecting 35% profit increase.

• $CART: Q3 EPS $0.42 vs. $0.22 est.; revenue $852M vs. $844M est.; Q4 EBITDA guidance $230M-$240M, below estimate; increased buyback program by $250M.

• $LNW: Q3 net income $64M, less than $100.7M expected; revenue $817M, slightly below $821.21M; continues double-digit revenue growth.

• $RIVN: Formed JV with Volkswagen for tech development, with VW investing up to $5.8B by 2027.

• $SAVE: Shares fell -60% due to bankruptcy filing rumors, currently negotiating with creditors.

• $TSLA: Recalling 2,431 Cybertrucks due to potential power loss issues, marking the sixth recall this year.

• $MODG: Q3 EPS loss at -$0.02, better than -$0.16 expected; revenue $1.01B, above $983M forecast; adjusted full-year revenue and EBITDA guidance downwards.

• $OXY: Q3 adj EPS $1.00, above $0.74 expected; production rose 15.7% to 1.41 Mboepd due to CrownRock acquisition, despite lower prices; Q4 production expected at 1.43-1.47 Mboepd.

• $RKLB: Q3 EPS ($0.10) vs. ($0.11) est., with revenues at $104.8M vs. $102.3M est.; Q4 revenue guidance $125-135M, with a new multi-launch deal for Neutron.

• $DHT: Q3 EPS $0.22, topping $0.20 estimate; adjusted EBITDA $70.4M vs. $66.4M expected, on slightly lower than expected adjusted revenues of $92.64M.

• $AB): Reported a 2% drop in AUM to $793B in October 2024 from $806B due to market downturn, with no net inflows or outflows.

• $MARA: Q3 revenue increased by 34% to $131.6M, missing the forecast of $137.5M.

• $PAY: Q3 EPS was $0.15 compared to $0.09 expected; revenue hit $231.6M against $190.6M estimated. They foresee Q4 revenue at $215M-$220M and FY24 at $829M-$834M, both above consensus.

• $RKT: Q3 adjusted EPS met estimates at $0.08; adjusted EBITDA was $286M, above the $272.33M expected, with revenues at $1.323B, beating the forecast. They anticipate a drop in Q4 revenue to $1.05-1.2B.

• $WULF: Q3 adjusted EBITDA was $6M, below the $11.2M prediction, with revenues at $27.1M, not meeting the $34.28M estimate.

• $AMGN: Clarified no link between MariTide use and bone density changes, despite earlier reports of potential loss. The company remains confident in the drug's future.

• $ICUI: Q3 adjusted EPS $1.59 vs $1.25 expected; revenue $589.131M vs $574.7M forecast, with a gross margin of 34.8%. FY guidance raised for EPS and EBITDA.

• $NTRA: Q3 EPS ($0.26) vs ($0.57) expected, revenue $439.8M vs $361.45M; FY revenue guidance set at $1.61-1.64B, above consensus.

• $PGNY: Q3 EPS $0.11, below $0.13 expected; revenue $286.625M vs $296.88M; full-year revenue and EBITDA guidance below market expectations.

• $SGMO: Q3 EPS $0.04, better than ($0.03) expected; revenue $49.41M vs $17.94M forecast. Adjusted annual operating expenses expected to be $125-145M.

• $SYRS: Shares dropped -80% after the SELECT-MDS-1 trial for tamibarotene failed to meet its primary endpoint, leading to discontinuation of the study.

• $DOX: Q4 adjusted EPS $1.70, matching expectations, with revenue at $1.264B, slightly above the $1.263B estimate.

• $PLUS: Q2 adjusted EPS $1.36, below $1.39 expected; revenue $515.2M vs $576.5M forecast. Full-year sales guidance unchanged, but adjusted EBITDA expected at $195-205M.

• $IAS: Q3 EPS $0.10 vs $0.07 expected, with revenue at $133.528M and a gross margin of 80%. Q4 revenue and EBITDA guidance were both below expectations.

• $SOUN: Q3 adjusted EPS ($0.04) vs ($0.07) expected; revenue $25.1M, above $23.02M estimate. Set FY24 and FY25 revenue targets.

• $SWKS: Q4 adjusted EPS $1.55 vs $1.52, revenue $1.025B, nearly matching estimates. Q1 guidance for revenue and EPS below expectations.

• $SPOT: Q3 revenue growth of 19% to €3.99B missed the €4.02B estimate; profit margin improved. Q4 revenue guidance below expectations but operating income and MAUs on target.

• $SMCI: Announced delay in filing Q3 2024 quarterly report due to ongoing issues with the annual report.

• $ZI: Q3 adjusted EPS $0.28, surpassing the $0.22 estimate; revenue $303.6M vs $299.38M. Q4 revenue guidance in line with estimates, but EPS slightly below consensus.