Notes

Those $WULF $10 January calls are in-the-money and up over 450% since the alert here on X in August and with @unusual_whales

$.50 to $2.86 as #WULF trades at $11.19 — we caught the flow AHEAD of the Google news & analyst upgrades in August. ✅📝😎

Those $WULF $10 January calls are now in-the-money and up over 400% since the alert last week here on X and with @unusual_whales

$.50 to $2.76 as #WULF trades at $10.28 — we caught the flow AHEAD of the Google news and analyst upgrades last week. ✅📝😎

Makes sense why we saw all of those $WULF $10 calls for January come through on Wednesday 📝😎 @unusual_whales

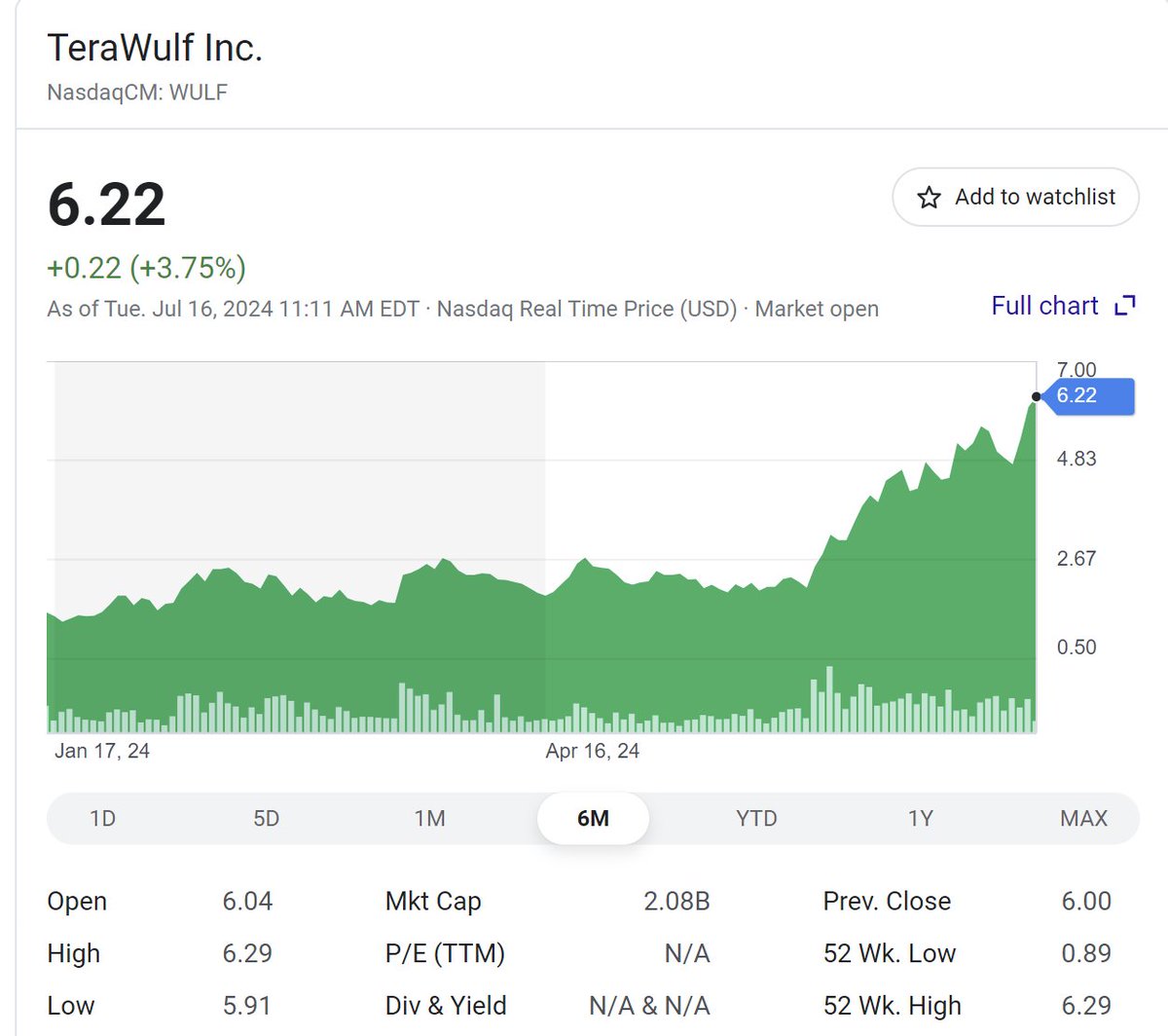

Also traders were loading $6.50 short-dated OTM calls — ahead of the news today as Terawulf surges 30% in premarket trading #WULF

Yesterday, I posted about a $138K call buy on $WULF options. Today, the stock surged 59%, turning those contracts into an incredible 1600% gain. If this whale is still holding, they’re up $2.2 million in just 24 hours!

Data from @unusual_whales

Those $WULF $10c January 2026 saw a high of $1.93 and were alerted on Wednesday on @unusual_whales and filling at $.50 — up 286% and were loaded ahead of the Google news today and analyst upgrades.

Get access to real-time flow and actionable alpha 📝✅😎

I hope everybody had a nice week. Great to see the reactions we did as a lot of impulse signals triggered where we expected them to(when the least were expecting it once again)💪Lots to unpack and dive into this weekend

Subscriber Agenda

Video: Why did miners fade into the close?

Charts:

New Impulse- #BTC LTF potential paths, $MARA, $RIOT, $CLSK, $IREN, $WULF, $CIFR, $SMLR, $XRP, $LINK, $LTC, $HOOD, $QQQ, $IWM, $SPY, $MSTR, $ETH, $DOGE

Ongoing Corrective- $TSLA, $PLTR, $SOFI, $MBLY, $MU, $PYPL, $CELH, $UPST(some of these names made big moves this week but I'm not sold corrections are over)

Correction Nearing Completion?- $CGC, $SQ, $NIO, $JD, $AMC, $LMND

Subscriber Requests- $XLM, $RUNE

MORNING BID

🔸 $NET: Upgraded to Buy by Citigroup, target price to $145 from $95, expecting 27%-30% annual revenue growth.

🔸 Citigroup: Positive 90-day watchlist for $OKTA, negative for $CRWD.

🔸 $WDC: Q2 revenue expected at $4.30B (below consensus $4.24B, EPS at $1.75-$2.05; CFO Jabre resigning.

🔸 $CRM: Upgraded to Buy from Hold by TD Cowen.

🔸 TikTok: Trump's advisor supports keeping app if deal viable; Schumer urges Biden to extend shutdown deadline by 90 days.

🔸 $OZK: Q4 EPS $1.56 vs. est. $1.44; NII $379-398M; book value up 11.5% to $47.30/share.

🔸 $CFG: Q4 EPS $0.85 vs. est. $0.83; revenue $1.99B; NIM 2.87%; provisions $162M.

🔸 $INDB: Q4 adj. EPS $1.21 vs. est. $1.16; NIM 3.33%; Q3 pre-tax profit $62.93M.

🔸 $RC: Announces $150M share buyback.

🔸 $RF: Q4 EPS $0.56 vs. est. $0.55; revenue $1.845B; Q1 NII to decline; NIM 3.55%; provisions $120M.

🔸 $WULF: Files for mixed shelf offering, size undisclosed.

🔸 $TFC: Q4 EPS $0.91 vs. est. $0.88; revenue $5.11B; tangible book value $30.01/share; CET1 ratio 11.5%; provisions $471M; Q1 revenue down 2% Q/Q; FY revenue up 3-3.5%.

🔸 $JBHT: Q4 EPS $1.53 vs. est. $1.61; revenue down 5% to $3.15B, due to declines in various segments including Intermodal (down 2%).

🔸 $DD and $AXTA: Upgraded to Outperform by Wolfe Research.

🔸 $OTIS: Authorizes $2B share repurchase program.

🔸 Shield AI: In talks to raise significant funding from $PLTR and $LMT, per The Information.

🔸 $CROX: Downgraded to Hold from Buy by Williams Trading due to weakening trends.

🔸 $RIVN: Finalizes $6.6B loan agreement with U.S. DOE for Georgia manufacturing.

Fisker: U.S. auto safety probe closed on 6,971 Ocean SUVs, no further investigation expected post-bankruptcy.

So it's the weekend and that means time to relax/take it easy...what that looks like over hear is 2 a days in the gym, loading up on nature's medicine(steak, eggs, fruit, veggies), and diving into the charts 💪

-Weekend Agenda for Subs

Video: $BTC Miners what I saw in $MSTR prior to its 4x move that I'm now seeing in the miners

Charts: Speculative paths+Upside/Downside targets

Early Expansion- $LCID, $MBLY, $RIVN, $LTC

Expansion- $BTC, $SQ, $PLTR, $ARKK, $NVDA, $DOGE, $XRP, $AMZN, $MSTR

Pre-Expansion- $MARA, $CLSK, $RIOT, $IREN, $BTBT, $WULF, $CIFR, $BITF, $WGMI

Bottom Formations- $BLNK, $AMC, $ARKG, $CELH

On-Going Corrective- $TSLA, $AMD, $MU, $LMND

Requests- Subscribers chart requests will be posted

RECAP

• $CAVA: Q3 EPS $0.15, above expectations of $0.11; sales up 39% to $243.8M; FY guidance for restaurant comp sales at 12.5%, up from 8.5-9.5%, and EBITDA at $123M. Plans to increase restaurant openings and margins.

• $FLUT: Q3 adjusted EBITDA up 74% to $450M; revenue up 27% to $3.25B; raised full-year forecasts for EBITDA and revenue, expecting 35% profit increase.

• $CART: Q3 EPS $0.42 vs. $0.22 est.; revenue $852M vs. $844M est.; Q4 EBITDA guidance $230M-$240M, below estimate; increased buyback program by $250M.

• $LNW: Q3 net income $64M, less than $100.7M expected; revenue $817M, slightly below $821.21M; continues double-digit revenue growth.

• $RIVN: Formed JV with Volkswagen for tech development, with VW investing up to $5.8B by 2027.

• $SAVE: Shares fell -60% due to bankruptcy filing rumors, currently negotiating with creditors.

• $TSLA: Recalling 2,431 Cybertrucks due to potential power loss issues, marking the sixth recall this year.

• $MODG: Q3 EPS loss at -$0.02, better than -$0.16 expected; revenue $1.01B, above $983M forecast; adjusted full-year revenue and EBITDA guidance downwards.

• $OXY: Q3 adj EPS $1.00, above $0.74 expected; production rose 15.7% to 1.41 Mboepd due to CrownRock acquisition, despite lower prices; Q4 production expected at 1.43-1.47 Mboepd.

• $RKLB: Q3 EPS ($0.10) vs. ($0.11) est., with revenues at $104.8M vs. $102.3M est.; Q4 revenue guidance $125-135M, with a new multi-launch deal for Neutron.

• $DHT: Q3 EPS $0.22, topping $0.20 estimate; adjusted EBITDA $70.4M vs. $66.4M expected, on slightly lower than expected adjusted revenues of $92.64M.

• $AB): Reported a 2% drop in AUM to $793B in October 2024 from $806B due to market downturn, with no net inflows or outflows.

• $MARA: Q3 revenue increased by 34% to $131.6M, missing the forecast of $137.5M.

• $PAY: Q3 EPS was $0.15 compared to $0.09 expected; revenue hit $231.6M against $190.6M estimated. They foresee Q4 revenue at $215M-$220M and FY24 at $829M-$834M, both above consensus.

• $RKT: Q3 adjusted EPS met estimates at $0.08; adjusted EBITDA was $286M, above the $272.33M expected, with revenues at $1.323B, beating the forecast. They anticipate a drop in Q4 revenue to $1.05-1.2B.

• $WULF: Q3 adjusted EBITDA was $6M, below the $11.2M prediction, with revenues at $27.1M, not meeting the $34.28M estimate.

• $AMGN: Clarified no link between MariTide use and bone density changes, despite earlier reports of potential loss. The company remains confident in the drug's future.

• $ICUI: Q3 adjusted EPS $1.59 vs $1.25 expected; revenue $589.131M vs $574.7M forecast, with a gross margin of 34.8%. FY guidance raised for EPS and EBITDA.

• $NTRA: Q3 EPS ($0.26) vs ($0.57) expected, revenue $439.8M vs $361.45M; FY revenue guidance set at $1.61-1.64B, above consensus.

• $PGNY: Q3 EPS $0.11, below $0.13 expected; revenue $286.625M vs $296.88M; full-year revenue and EBITDA guidance below market expectations.

• $SGMO: Q3 EPS $0.04, better than ($0.03) expected; revenue $49.41M vs $17.94M forecast. Adjusted annual operating expenses expected to be $125-145M.

• $SYRS: Shares dropped -80% after the SELECT-MDS-1 trial for tamibarotene failed to meet its primary endpoint, leading to discontinuation of the study.

• $DOX: Q4 adjusted EPS $1.70, matching expectations, with revenue at $1.264B, slightly above the $1.263B estimate.

• $PLUS: Q2 adjusted EPS $1.36, below $1.39 expected; revenue $515.2M vs $576.5M forecast. Full-year sales guidance unchanged, but adjusted EBITDA expected at $195-205M.

• $IAS: Q3 EPS $0.10 vs $0.07 expected, with revenue at $133.528M and a gross margin of 80%. Q4 revenue and EBITDA guidance were both below expectations.

• $SOUN: Q3 adjusted EPS ($0.04) vs ($0.07) expected; revenue $25.1M, above $23.02M estimate. Set FY24 and FY25 revenue targets.

• $SWKS: Q4 adjusted EPS $1.55 vs $1.52, revenue $1.025B, nearly matching estimates. Q1 guidance for revenue and EPS below expectations.

• $SPOT: Q3 revenue growth of 19% to €3.99B missed the €4.02B estimate; profit margin improved. Q4 revenue guidance below expectations but operating income and MAUs on target.

• $SMCI: Announced delay in filing Q3 2024 quarterly report due to ongoing issues with the annual report.

• $ZI: Q3 adjusted EPS $0.28, surpassing the $0.22 estimate; revenue $303.6M vs $299.38M. Q4 revenue guidance in line with estimates, but EPS slightly below consensus.