Notes

Only one hour left until the jobs report is released. 🚨

How could the latest US jobs report and rising Middle East tensions shape the markets this Friday?

2026年值得关注的顶级增长主题

• 加密货币 | $HOOD $COIN $BMNR

• 量子 | $IONQ $RGTI $QBTS

• 机器人 | $TSLA $SYM $ISRG $RR

• 核能 | $OKLO $LEU $GEV $UUUU

• AI 公用设施 | $CRWV $NBIS $IREN $CIFR

• AI 芯片 | $NVDA $TSM $ASML $AMD

• 电网与电力 | $CEG $NEE $VST $EOSE

• 无人机 | $ONDS $UMAC $DPRO $AVAV

• AI 数据平台 | $PLTR $SNOW $MDB

• AI 安全 | $CRWD $ZS $PANW $RBRK

• 太空经济 | $RKLB $ASTS $PL $RDW

• AI 网络 | $AVGO $ALAB $MRVL $CRDO

• AI 云 | $MSFT $AMZN $GOOGL $DOCN $ORCL

cc @BTCBruce1

$HOOD

-3.97%

$COIN -10.98%

$BMNR -0.19%

$IONQ $RGTI $QBTS $TSLA -27.76%

$SYM $ISRG $RR $OKLO $LEU $GEV $UUUU $CRWV -4.78%

$NBIS $IREN $CIFR $NVDA +5.46%

$TSM -8.8%

$ASML -3.29%

$AMD -0.57%

$CEG $NEE $VST $EOSE $ONDS $UMAC $DPRO $AVAV $PLTR -3.6%

$SNOW $MDB $CRWD $ZS $PANW $RBRK $RKLB $ASTS $PL $RDW $AVGO $ALAB $MRVL $CRDO $MSFT -0.85%

$AMZN -0.88%

$GOOGL +0.69%

$DOCN $ORCL +2.77%

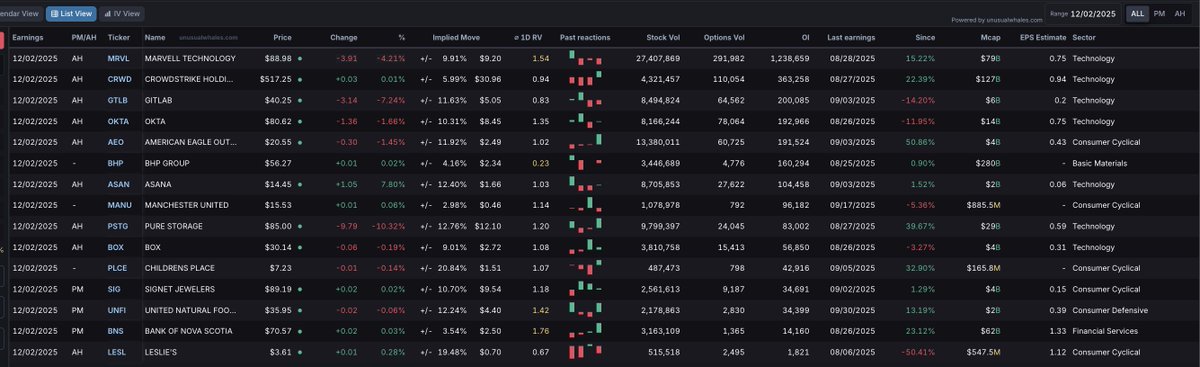

Earnings results for today:

Crowdstrike $CRWD

EPS $0.96 vs $0.94

Revenue $1.23B vs $1.21B expected

American Eagle $AEO

EPS $0.53 vs $0.44

Revenue $1.36B vs $1.32B

Box $BOX

EPS $0.31 vs $0.31 expected

Revenue $301M vs $298.93M expected

Asana $ASAN

EPS $0.07 vs $0.06

Revenue $201M vs $198M

GitLab $GTLB

EPS $0.25 vs $0.2

Revenue $244M vs $239M

Marvell $MRVL

EPS $0.76 vs %0.74

Revenue $2.075B vs $2.07B

Link to all earnings for today: https://t.co/bXFFJ7Mrp6

最近半年团队主要研究 #AI 和 #RWA 赛道比较多,被问及最多的问题:‘#AI 是不是已经过了最热的“炒作期”?’,因为我们看到很多 #AI 加密项目或股票,貌似涨速有点慢或者不涨了!

我的看法是——远远没有。现在的 #AI,差不多就相当于1995年、1996年互联网的阶段。那时候大家刚开始上网,浏览器才出来没几年,亚马逊、谷歌都还没真正爆发,但趋势已经很清晰了。#AI 现在也差不多这样,刚进入加速成长期。

🧐为何这么说?

1️⃣算力依旧是瓶颈,也是最大机会,做AI要训练大模型,需要巨量的算力。美国这边有英伟达,芯片卖到断货。中国这边因为美国的出口管制,反而倒逼出一条本土产业链。比如寒武纪(Cambricon)这种公司,股价和市值都翻了好几倍。背后逻辑很简单:没有芯片,AI走不动。这就是最底层的“铲子生意”。我自己投股票的时候,最看重这种“确定性刚需”,不管AI应用做得怎么样,算力永远少不了。

2️⃣中国的“Buy China”逻辑,中美关系其实是把“双刃剑”。美国不卖顶级芯片给中国,看似是打压,但反过来成了国产替代的超级机会。没有封锁,中国的AI公司可能还在用英伟达的GPU,也不会有动力自己研发芯片。现在反而逼出了一个完整的国产生态。我在看中国半导体、算力相关公司的时候,这一点就是核心逻辑:自给自足是国家战略,市场够大,需求也刚性。

3️⃣政府是超级风投,你要看中国的模式,其实很像10年前的新能源车。那时候政府补贴电池、补贴买车,硬是把比亚迪、宁德时代推起来了。现在AI和机器人也一样,地方政府出补贴、投基金,相当于官方当“早期VC”,先给产业打地基。剩下的就交给企业家去拼执行力。作为投资人,我的判断是:政府方向决定赛道,企业家决定龙头。

投资的衡量标准,我们看一个AI或者机器人项目,最关键是两个问题:

✅它能不能真正解决痛点?比如机器人,能不能真的在家庭里帮老人、能不能在仓库里搬货,不是光好看、噱头大。

✅它有没有产品市场匹配度(PMF)?就是说,这个产品是刚需,还是锦上添花?如果只是“看上去很酷”,但没人愿意为它买单,那就不行。在AI模型上也是一样。现在模型满大街都是,但能真正跑通商业模式的,要么解决企业的需求(比如代码自动化、办公提效),要么解决消费者的需求(比如智能助手、娱乐)。我投项目时,最怕那种“炫技”型公司,看上去技术牛,但没落地场景。

长期趋势我判断,未来3-5年里,AI算力的需求会是现在的10倍甚至100倍。这意味着:

· 上游的芯片、算力基础设施公司,还是最稳的“吃肉”位置。

· 中游的大模型会越来越分化,能落地的会脱颖而出,光靠堆钱堆算力的可能会被淘汰。

· 下游的应用场景(比如机器人),现在看起来还早,但一旦找到像电动车那样的突破口,成长会非常惊人。

所以我们在 #AI 赛道的投资思路:

第一层:算力/芯片 → 确定性最强,国家战略支持,需求无限大(加密也是类似逻辑,分布式GPU算力依旧有空间)。

第二层:大模型 → 拼资源和落地场景,要慎重挑选,差距很快拉开。

第三层:应用(机器人等) → 风险大,但如果踩中龙头,可能是百倍回报。

所以我现在看AI,就像看当年的互联网和新能源车。远远没到泡沫破灭的时候,反而刚刚进入“加速跑道”。🧐

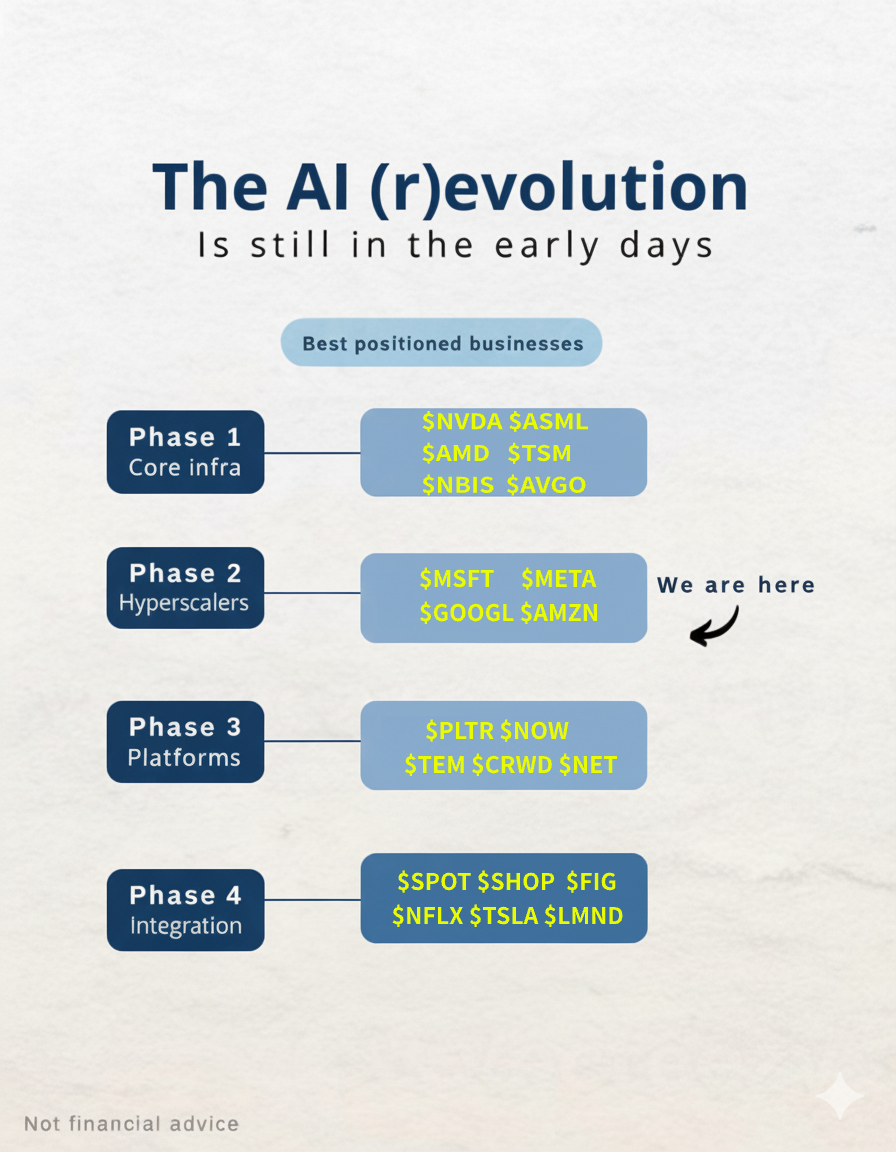

#AI 时代,👇是我们比较看好的美股 #AI 公司:

最近英伟达老板黄仁勋提到,我们仍处于人工智能的早期阶段。现阶段仍然处于超大规模企业部署阶段,属于第二阶段,如👇图。

• 第一阶段(核心基础设施): $NVDA , $ASML , $AMD , $TSM , $AVGO , $NBIS

• 第二阶段(超大规模企业): $MSFT , $META , $GOOGL , $AMZN

• 第三阶段(平台型): $PLTR , $NOW , $TEM , $CRWD , $NET

• 第四阶段(应用集成): $SPOT , $SHOP , $NFLX , $TSLA , $LMND , $FIG

WEDBUSH’S DAN IVES RELEASED THE “IVES AI 30,” FEATURING TOP AI PLAYS:

🔸 Hyperscalers: $MSFT, $GOOGL, $AMZN, $ORCL

🔸 Software: $PLTR, $CRM, $IBM, $NOW, $SNOW, $PEGA, $MDB, $SOUN, $INOD

🔸 Consumer Internet: $BABA, $AAPL, $META, $BIDU, $RBLX

🔸 Cybersecurity: $PANW, $ZS, $CRWD

🔸 Autonomous/Robotics & Power: $TSLA, $OKLO, $GEV

🔸 Semiconductors/Hardware: $NVDA, $AMD, $TSM, $AVGO, $MU, $NBIS

在等减息的无聊日子里,开始进军mystonk的美股交易

对于没有美股账号的国内用户,mystonk毫无疑问是参与美股交易的最短路径。

比如说对于我爸,mystonk是他交易美股最简单的选择,手续费低至千3。拥有mystonk账号的我,是离他最近的“券商”。

美股交易门槛非常低,只需要身份证正反面,以及手持身份证照片KYC通过即可。

https://t.co/kK5Loh6EGW

原理:

MyStonks将美股以1:1的比例映射为ERC-20代币(如AAPL.M),这些代币在Coinbase发行的Base区块链上铸造,由chainlink喂价,为用户提供T+0交易,代表真实股票的所有权。链下资产托管与富达(Fidelity)进行合作,首批托管规模达5000万美元。

Mystonk方案会是RWA的终局形态吗?显然不是。

就像U卡不是支付的终局一样。但他确实有着实实在在的需求,make it work first

如果所有人都只着眼终局,那么谁来走第一步呢?

万事开头难,先看看mystonk新上线的两只股票开始吧

战争+AI概念: $PLTR.M

Ai+战争网络安全概念: $CRWD.M

$PLTR.M (Palantir)以其强大的嵌入式AI平台和政府合同闻名,股价年内涨幅超74%,成为标普500指数中表现第二的股票。

-关键驱动因素:2025年4月与美国移民与海关执法局签订3000万美元合同,商业部门Q1收入同比增长71%。Kol讨论度第一。

近期其AI系统已在美军中东司令部(CENTCOM)全面部署,并收获五大战区司令部合同。

市场情绪:尽管市盈率高达238.10,但Loop Capital将目标价上调至155美元,看好其在企业AI领域的领导地位。

未来展望:预计到2025年底,股价可能在107美元至207美元之间波动,长期来看,部分预测认为到2030年PLTR可能达到351.41美元。

$CRWD.M(CrowdStrike)

-全球顶级网络安全公司:CrowdStrike以其云原生Falcon平台和AI驱动的威胁检测闻名,股价年内上涨约38%。

-核心产品:Falcon平台包含29个模块,适用于从中小企业到大型企业的各种需求,2025年推出的Falcon Go进一步拓展了中小企业市场。

近期动态:本次Falcon威胁情报网重点跟踪伊朗APT 33/34/35(Kitten系),为政府和关键基础设施推送IOC/TTP,防御高级威胁。KOL讨论度美区前五

-财务表现:2025财年第一季度收入11亿美元,同比增长20%,调整后每股收益0.73美元,超预期。

-未来展望:预计2025财年收入为47.4亿至48.1亿美元,调整后每股收益3.44至3.56美元。长期来看,部分分析师预测到2030年CRWD可能突破1000美元。

最后

📈 投资有风险,入市需谨慎!

MORNING BID

🔸 $NET: Upgraded to Buy by Citigroup, target price to $145 from $95, expecting 27%-30% annual revenue growth.

🔸 Citigroup: Positive 90-day watchlist for $OKTA, negative for $CRWD.

🔸 $WDC: Q2 revenue expected at $4.30B (below consensus $4.24B, EPS at $1.75-$2.05; CFO Jabre resigning.

🔸 $CRM: Upgraded to Buy from Hold by TD Cowen.

🔸 TikTok: Trump's advisor supports keeping app if deal viable; Schumer urges Biden to extend shutdown deadline by 90 days.

🔸 $OZK: Q4 EPS $1.56 vs. est. $1.44; NII $379-398M; book value up 11.5% to $47.30/share.

🔸 $CFG: Q4 EPS $0.85 vs. est. $0.83; revenue $1.99B; NIM 2.87%; provisions $162M.

🔸 $INDB: Q4 adj. EPS $1.21 vs. est. $1.16; NIM 3.33%; Q3 pre-tax profit $62.93M.

🔸 $RC: Announces $150M share buyback.

🔸 $RF: Q4 EPS $0.56 vs. est. $0.55; revenue $1.845B; Q1 NII to decline; NIM 3.55%; provisions $120M.

🔸 $WULF: Files for mixed shelf offering, size undisclosed.

🔸 $TFC: Q4 EPS $0.91 vs. est. $0.88; revenue $5.11B; tangible book value $30.01/share; CET1 ratio 11.5%; provisions $471M; Q1 revenue down 2% Q/Q; FY revenue up 3-3.5%.

🔸 $JBHT: Q4 EPS $1.53 vs. est. $1.61; revenue down 5% to $3.15B, due to declines in various segments including Intermodal (down 2%).

🔸 $DD and $AXTA: Upgraded to Outperform by Wolfe Research.

🔸 $OTIS: Authorizes $2B share repurchase program.

🔸 Shield AI: In talks to raise significant funding from $PLTR and $LMT, per The Information.

🔸 $CROX: Downgraded to Hold from Buy by Williams Trading due to weakening trends.

🔸 $RIVN: Finalizes $6.6B loan agreement with U.S. DOE for Georgia manufacturing.

Fisker: U.S. auto safety probe closed on 6,971 Ocean SUVs, no further investigation expected post-bankruptcy.

$APLT: Baird's target price adjustment: $14 to $5.

RBC's target price change: $12 to $4, rating shift from outperform to sector perform.

$ADSK: Citigroup's slight target price increase: $358 to $361.

$BFb: Barclays' target price reduction: $53 to $49.

$CF: Berenberg's target price elevation: $69 to $74.

$CRWD: Citigroup's significant target price hike: $300 to $400.

$DSGX: RBC's target price upgrade: $115 to $133.

$DOMO: TD Cowen's minor target price lift: $9 to $10.

$EQIX: Truist Securities' substantial target price increase: $935 to $1,090.

$GNL: Truist Securities' target price reduction: $8.50 to $8.

$SJM: Citigroup's target price rise: $134 to $137.

Barclays' target price elevation: $121 to $126.

$PASG: Wedbush's initiation of coverage with outperform rating, target price set at $4 from a previous $3.

$PEB: Stifel's target price adjustment: $15 to $16.25.

$PFE: Berenberg's target price uptick: $27 to $29.

$PLL: BMO's target price increase: $9.50 to $14.

$PLYM: Truist Securities' price target cut: $27 to $22.

$RDNT: Truist Securities' target price boost: $80 to $94.

$SW: JP Morgan's target price adjustment: $65 to $69.

$SBEV: H.C. Wainwright's target price decrease: $1 to $0.50.

$TXNM: Barclays' target price elevation: $46 to $52.

$ULTA: Citigroup's target price increase: $345 to $390.

$URBN: Citigroup's rating upgrade to buy from neutral, target price rise from $42 to $59.

$VYGR: Wedbush's initiation of coverage with outperform rating, target price set at $11 from $7.

$WMG: Citigroup's target price adjustment: $31 to $34.

DAILY RECAP

$AAPL saw minimal smartphone shipment growth in 2024 amidst a strong market rebound, according to IDC.

$AMBA Q3 adj EPS $0.11 vs $0.03 est., revenue $82.7M vs $79.02M est.; Q4 rev guidance $76-80M.

$ADSK Q3 EPS $2.17 vs $2.12 est., revenue $1.57B vs $1.562B est.; Q4 revs $1.623-1.638B, FY revs $6.115-6.13B.

$CRWD Q3 EPS $0.93 vs $0.81 est., revenue $1.01B vs $982.36M est.; Q4 revs $1.029-1.035B.

$DELL Q3 EPS $2.15 vs $2.06 est., revenue $24.4B vs $24.72B est.; strong growth in infrastructure, slight decline in client solutions.

$HPQ Q4 EPS $0.93 as expected, revenue $14.1B vs $13.986B est.; Q1 and FY EPS guidance lowered.

$NTNX Q1 EPS $0.42 vs $0.32 est., revenue $591M vs $571.8M est.; Q2 rev guidance $635M-$645M.

$PD Q3 EPS $0.28 vs $0.17 est., revenue $118.9M vs $116.52M est.; Q4 revs $118.5-120.5M, FY revs $464.5-466.5M.

$WDAY Q3 EPS $1.89 vs $1.76 est., revenue $2.16B vs $2.13B est.; Q4 subscription revs lower than expected.

$DDD Q3 EPS ($0.12) vs ($0.10) est., revenue $112.9M vs $115.27M est.; FY rev guidance $440-450M, improving adj EBITDA.

$GES reported Q3 EPS at $0.34, under $0.38 expected, with revenue up 13% to $738.5M. They've cut FY25 EPS and revenue growth forecasts.

$JWN beat with Q3 EPS of $0.33 vs. $0.22, revenues up 4.3% to $3.46B, and raised FY24 revenue outlook.

$URBN excelled with Q3 EPS at $1.10 vs. $0.85, revenue up 6.3% to $1.36B. Growth in Anthropologie, Free People, and Nuuly, but a decline at Urban Outfitters.

$GRO priced its IPO at $15/share, offering 2M shares instead of the planned 4.25M.

$BYDDY is seeking supplier price reductions, bracing for tougher competition in China's EV market.

$SEDG is ending its storage division, cutting jobs by 500, with expected charges for assets and inventory.

$VWAGY has agreed to divest from its Xinjiang plant amidst human rights concerns.

$IREN reported a Q1 Bitcoin mining revenue drop to $49.6M from $54.3M due to higher network difficulty and lower Bitcoin prices, despite increased hashrate. AI Cloud Services revenue rose by 28% to $3.2M from $2.5M with new GPU's added. Adjusted EBITDA fell to $2.6M from $12.2M, with 813 Bitcoins mined compared to 821 in the prior quarter.

$ACAD has secured exclusive rights to SAN711 from Saniona for global development and sales.

$GRFS stock fell after Bloomberg reported Brookfield is set to abandon its €6.45 billion acquisition attempt due to pricing disagreements.