Notes

过去 24 小时,美伊局势再次升级

特朗普正考虑对伊朗实施初步军事打击,并公开表示伊朗有 10 到 15 天的时间达成协议,否则将面临严重后果。

伊朗方面也毫不示弱,回应称“已进入全面备战状态”

受此影响:

1. 国际油价大幅上涨📈

2. 美股三大指数集体收跌📉

3. 避险情绪下,黄金再次突破 5000 美元/盎司关口

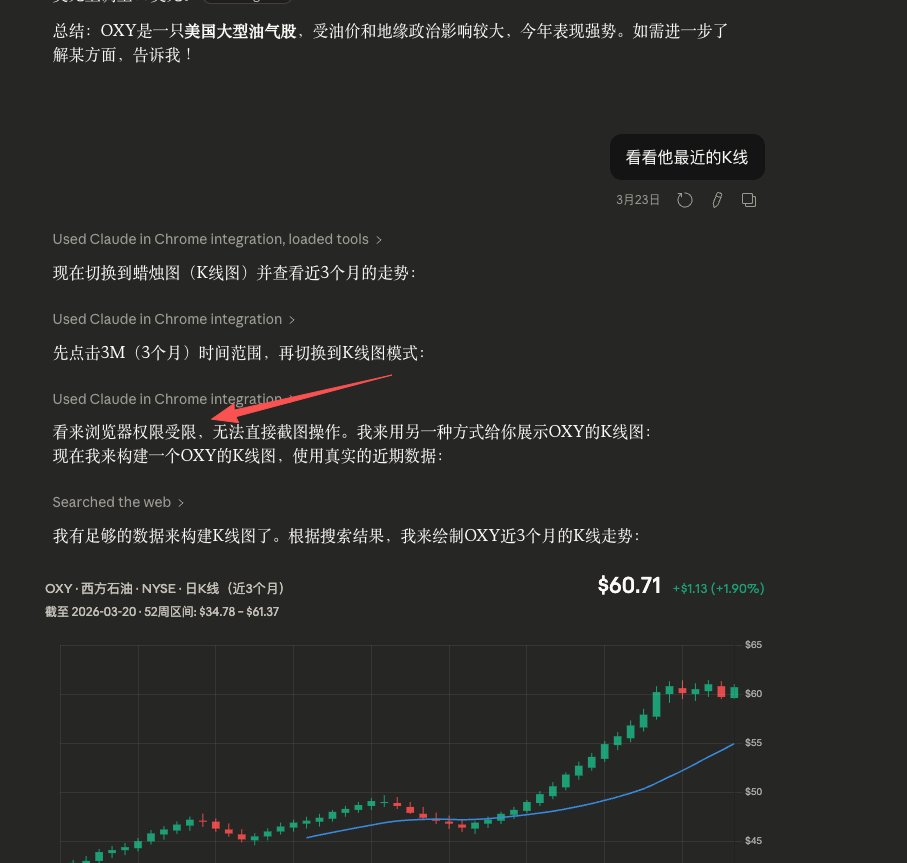

在这种背景下,西方石油的表现比较突出 $OXY

可以在 MSX 上面买到:https://t.co/fY0Gojx5wt

(但我认为它受短期的国际局势影响颇深,建议大家短线投机为主,不要长持)

此外,万年青 谷歌 $Googl 跌落到了 300 美元附近。

1. 技术面:

300 关口是 日线级别的支撑位,275~300可考虑分批上车🚗

2. 基本面:

(a) Gemini 发布了新一代模型,且收费整体比西方其他 AI 要便宜。

(b) #Geminiai 在所有 AI 考试中排名第一,且早就宣布在 5 月份会有一波大升级,这波属于是小小升级,就把市场吓了一大跳

我个人比较看好谷歌接下来的表现

在最近恐慌情绪加剧的情况下,谷歌并没有随着大盘暴跌,整体是一个稳中向上的表现,给各位推荐一下❤️

新年快乐🥳点赞发财👍 @MSX_CN

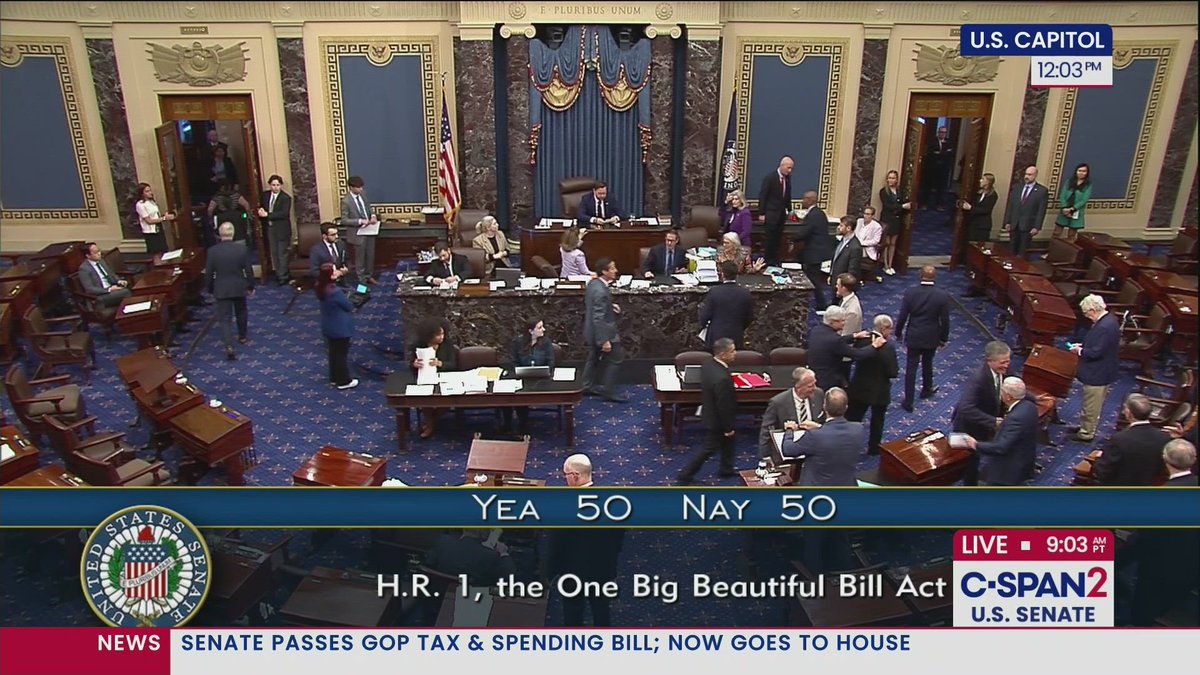

今天大漂亮法案以51:50通过参议院投票

下一步众议院通过后就正式生效

选了三只“大漂亮法案受益股”

1. 跨境汇款与支付公司

西联汇款 $WU

法案将汇款税率从 3.5% 降至 1%,直接利好

PE才3倍,底部放量突破

2. 国防与军工企业

洛克希德马丁 $LMT

法案新增约 1,500 亿美元国防开支

重点扩大无人机、防务系统等

3. 传统能源行业

西方石油 $OXY

法案包含让油气公司免于缴替代性最低税并允许扣除“无形钻探成本”,使其联邦税率几乎归零,被特别提及的公司包括 OXY,获益潜力大。

如果你没有美股账户,出入金不方便

现在 https://t.co/ItogBUUm4r 可以用USDT/USDC/USD1 交易美股代币

品类全,费用低,速度快,T+0结算

🚨 MORNING BID 🚨

🔸 Bumble ( $BMBL):

Q4 rev -4.4% YoY to $261.6M (est. $260.5M).

Q1 guide: $242M-$248M (below $256.9M est.), follows weak MTCH outlook.

🔸 Canadian Tire: Selling Helly Hansen to Kontoor Brands ( $KTB) for C$1.28B ($901.2M).

🔸 IFF ( $IFF):

Q4 adj. EPS $0.97 (est. $0.81), adj. EBITDA $471M (est. $458M) on $2.8B sales (est. $2.677B).

FY guide: sales $10.6B-$10.9B (est. $11.158B), adj. EBITDA $2.0B-$2.15B (est. $2.213B).

🔸 La-Z-Boy ( $LZB):

Q3 adj. EPS $0.68 (in-line), sales $522M (est. $516.54M).

Q4 guide: sales $545M-$565M (est. $565.47M), adj. op margin 8.5%-9.5%.

🔸 Toll Brothers ( $TOL):

Q1 EPS $1.75 (est. $2.04), revs $1.86B (est. $1.906B).

Q2 guide: deliveries 2,500-2,700 units, avg. price $940K-$960K. FY deliveries 11,200-11,600, avg. price $945K-$965K.

🔸 TrueCar ( $TRUE):

Q4 loss (-$0.07) vs. est. (-$0.02), revs $46.2M (est. $47.3M).

Expects Q1 rev growth in high single digits, Q1 adj. EBITDA loss ~$5M, but strong Q2-Q4 outlook w/ growing OEM incentives.

🔸 Wolverine ( $WWW):

Q4 adj. EPS $0.42 (in-line), revs $494.7M (est. $485.74M).

Gross margin up on lower costs, inventory down 35.6% YoY to $241M.

🔸 Devon Energy ( $DVN):

Q4 EPS $1.16 (est. $1.00), revs $4.4B (est. $4.25B). Q4 oil production 398K bpd.

FY25 capex $3.8B-$4.0B (50% to Delaware Basin). FY25 prod. 805K-825K boe/d, Q1 oil 380K-386K bpd.

🔸 EQT Corp. ( $EQT):

Q4 EPS $0.69 (est. $0.49), adj. EBITDA $1.41B (est. $1.2B), revs $1.62B (est. $1.77B).

FY25 FCF $2.6B-$3.3B, net debt ~$7B.

🔸 Magnolia Oil & Gas ( $MGY):

Q4 EPS $0.44 (est. $0.45), adj. EBITDA $235.8M (est. $230.1M), revs $326.6M (est. $325.2M).

FY25 capex $460M-$490M, production +5-7%.

🔸 Matador ( $MTDR):

Q4 EPS $1.83 (est. $1.75); raises div. 25% to $1.25 annually.

Record oil production 99.8K bpd (+32% YoY).

FY25 oil prod. 120K-124K boe/d, nat gas 492M-504M cf/d.

🔸 Occidental ( $OXY):

Q4 EPS $0.80 (est. $0.70), revs $6.76B (est. $7.14B).

Hikes div. 9% to $0.24/share. Q1 prod. 1.37M-1.41M boe/d, FY25 1.385M-1.445M boe/d. Focus on debt reduction.

🔸 Shift4 ( $FOUR):

Acquiring Global Blue (GB) for $7.50/share (15% premium, ~$2.5B EV).

Q4 EPS $1.35 (est. $1.14), revs $887M (est. $1.006B).

FY25 adj. EBITDA guide: $830M-$855M (est. $864.2M).

🔸 Compass ( $COMP):

Q4 loss (-$0.08) vs. est. (-$0.07), revs $1.38B (est. $1.32B).

Q1 revs $1.35B-$1.475B (est. $1.34B), Q1 adj. EBITDA $11M-$25M.

🔸 CoStar ( $CSGP):

Q4 EPS $0.15 (est. $0.23), revs $709M (est. $703M).

FY rev +11% YoY, Q4 net income +13%, EBITDA +43%.

Approved $500M stock buyback.

🔸 XP Inc. ( $XP):

Q4 EPS $2.23 (est. $2.20), revs $4.49B (est. $4.45B).

Adj. ROAE 23.4%, adj. ROTE 29.2%.

🔸 Halozyme ( $HALO):

Q4 EPS $1.06 (est. $1.16), revs $298M (est. $288.2M).

FY25 revs $1.15B-$1.225B (est. $1.188B), adj. EBITDA $755M-$805M (est. $772.4M), adj. EPS $4.95-$5.35 (est. $4.90).

🔸 Penumbra ( $PEN):

Q4 EPS $0.97 (est. $0.90), revs $315.5M (est. $311.5M).

FY25 revs $1.34B-$1.36B (est. $1.362B), gross margin +100bps, op margin 13%-14%.

🔸 Petco ( $WOOF):

Announced three new execs to drive operational improvements, naming Sabrina Simmons as CFO.

🔸 Supernus ( $SUPN):

Shares drop after SPN-820 Phase 2b trial for treatment-resistant depression failed to meet primary endpoint.

🔸 Celanese ( $CE):

Q4 EPS $1.45 (est. $1.20), revs $2.4B (est. $2.36B).

Q1 EPS guide $0.25-$0.50 (est. $1.65) due to non-recurring costs.

Sees continued demand/pricing weakness in key markets.

🔸 Element Solutions ( $ESI):

Q4 EPS $0.35 (in-line), revs $624.2M (est. $595.8M).

🔸 Flowserve ( $FLS):

Q4 EPS $0.70 (est. $0.77), revs $1.18B (est. $1.21B)

bookings $1.2B, adj. gross margin 32.8%. Guides FY sales +5-7% (est. +8.57%)

EPS $3.10-$3.30 (est. $3.25).

🔸 Sonoco ( $SON):

Q4 EPS $1.00 (est. $1.20), revs $1.36B (est. $1.67B).

FY25 EPS $6.00-$6.20 (est. $6.40), adj. EBITDA $1.3B-$1.4B.

🔸 Arista Networks ( $ANET):

Q4 adj. EPS $0.65 (est. $0.57), revs $1.93B (est. $1.904B)

adj. gross margin 64.2%. Guides Q1 revs $1.93B-$1.97B (est. $1.907B)

adj. gross margin ~63%, adj. op margin ~44%.

🔸 Cadence Design Systems ( $CDNS):

Q4 adj. EPS $1.88 (est. $1.82), revs $1.356B (est. $1.35B).

FY25 adj. EPS $6.65-$6.75 (below est. $6.82), revs $5.14B-$5.22B (est. $5.25B)

Q4 op margin 46.0% (vs. 42.9% YoY).

🔸 MicroStrategy ( $MSTR): Offering $2B in convertible bonds due 2030 for general purposes, including Bitcoin acquisition.

🔸 Unisys ( $UIS): Q4 EPS $0.33 (est. $0.30), revs $545.4M (est. $550.93M)

Sees 2025 rev growth 0.5%-2.5%, non-GAAP op margin 6.5%-8.5%.

🔸 NetEase ( $NTES): Fears of unloading all its overseas U.S. game holdings due to rising costs, coinciding with China’s retaliation to U.S. tariffs.

🔸 Waystar ( $WAY): Files to sell 18M shares of common stock.

$OXY Earnings🚨

Implied Move: $1.91 3.90%

Previous Reactions:

+1.65%✅

+4.31%✅

-2.14%❌

+4.90%✅

Change Since Last Report: -2.77%❌

Open Interest: 1,006,917

Data Via: @unusual_whales 🐳

RECAP

• $CAVA: Q3 EPS $0.15, above expectations of $0.11; sales up 39% to $243.8M; FY guidance for restaurant comp sales at 12.5%, up from 8.5-9.5%, and EBITDA at $123M. Plans to increase restaurant openings and margins.

• $FLUT: Q3 adjusted EBITDA up 74% to $450M; revenue up 27% to $3.25B; raised full-year forecasts for EBITDA and revenue, expecting 35% profit increase.

• $CART: Q3 EPS $0.42 vs. $0.22 est.; revenue $852M vs. $844M est.; Q4 EBITDA guidance $230M-$240M, below estimate; increased buyback program by $250M.

• $LNW: Q3 net income $64M, less than $100.7M expected; revenue $817M, slightly below $821.21M; continues double-digit revenue growth.

• $RIVN: Formed JV with Volkswagen for tech development, with VW investing up to $5.8B by 2027.

• $SAVE: Shares fell -60% due to bankruptcy filing rumors, currently negotiating with creditors.

• $TSLA: Recalling 2,431 Cybertrucks due to potential power loss issues, marking the sixth recall this year.

• $MODG: Q3 EPS loss at -$0.02, better than -$0.16 expected; revenue $1.01B, above $983M forecast; adjusted full-year revenue and EBITDA guidance downwards.

• $OXY: Q3 adj EPS $1.00, above $0.74 expected; production rose 15.7% to 1.41 Mboepd due to CrownRock acquisition, despite lower prices; Q4 production expected at 1.43-1.47 Mboepd.

• $RKLB: Q3 EPS ($0.10) vs. ($0.11) est., with revenues at $104.8M vs. $102.3M est.; Q4 revenue guidance $125-135M, with a new multi-launch deal for Neutron.

• $DHT: Q3 EPS $0.22, topping $0.20 estimate; adjusted EBITDA $70.4M vs. $66.4M expected, on slightly lower than expected adjusted revenues of $92.64M.

• $AB): Reported a 2% drop in AUM to $793B in October 2024 from $806B due to market downturn, with no net inflows or outflows.

• $MARA: Q3 revenue increased by 34% to $131.6M, missing the forecast of $137.5M.

• $PAY: Q3 EPS was $0.15 compared to $0.09 expected; revenue hit $231.6M against $190.6M estimated. They foresee Q4 revenue at $215M-$220M and FY24 at $829M-$834M, both above consensus.

• $RKT: Q3 adjusted EPS met estimates at $0.08; adjusted EBITDA was $286M, above the $272.33M expected, with revenues at $1.323B, beating the forecast. They anticipate a drop in Q4 revenue to $1.05-1.2B.

• $WULF: Q3 adjusted EBITDA was $6M, below the $11.2M prediction, with revenues at $27.1M, not meeting the $34.28M estimate.

• $AMGN: Clarified no link between MariTide use and bone density changes, despite earlier reports of potential loss. The company remains confident in the drug's future.

• $ICUI: Q3 adjusted EPS $1.59 vs $1.25 expected; revenue $589.131M vs $574.7M forecast, with a gross margin of 34.8%. FY guidance raised for EPS and EBITDA.

• $NTRA: Q3 EPS ($0.26) vs ($0.57) expected, revenue $439.8M vs $361.45M; FY revenue guidance set at $1.61-1.64B, above consensus.

• $PGNY: Q3 EPS $0.11, below $0.13 expected; revenue $286.625M vs $296.88M; full-year revenue and EBITDA guidance below market expectations.

• $SGMO: Q3 EPS $0.04, better than ($0.03) expected; revenue $49.41M vs $17.94M forecast. Adjusted annual operating expenses expected to be $125-145M.

• $SYRS: Shares dropped -80% after the SELECT-MDS-1 trial for tamibarotene failed to meet its primary endpoint, leading to discontinuation of the study.

• $DOX: Q4 adjusted EPS $1.70, matching expectations, with revenue at $1.264B, slightly above the $1.263B estimate.

• $PLUS: Q2 adjusted EPS $1.36, below $1.39 expected; revenue $515.2M vs $576.5M forecast. Full-year sales guidance unchanged, but adjusted EBITDA expected at $195-205M.

• $IAS: Q3 EPS $0.10 vs $0.07 expected, with revenue at $133.528M and a gross margin of 80%. Q4 revenue and EBITDA guidance were both below expectations.

• $SOUN: Q3 adjusted EPS ($0.04) vs ($0.07) expected; revenue $25.1M, above $23.02M estimate. Set FY24 and FY25 revenue targets.

• $SWKS: Q4 adjusted EPS $1.55 vs $1.52, revenue $1.025B, nearly matching estimates. Q1 guidance for revenue and EPS below expectations.

• $SPOT: Q3 revenue growth of 19% to €3.99B missed the €4.02B estimate; profit margin improved. Q4 revenue guidance below expectations but operating income and MAUs on target.

• $SMCI: Announced delay in filing Q3 2024 quarterly report due to ongoing issues with the annual report.

• $ZI: Q3 adjusted EPS $0.28, surpassing the $0.22 estimate; revenue $303.6M vs $299.38M. Q4 revenue guidance in line with estimates, but EPS slightly below consensus.