Autonomous Polymarket agents were always inevitable.

The question was who builds the version that doesn’t require a dev setup to run.

The terminal-and-MCP approach works if you’re already technical. But most traders aren’t.

Sides Agent putting plain English strategy input, Telegram-native execution, Kelly sizing, and auto-pause on failures into one package is a different surface area entirely.

EV calculation and basket arb running 24/7 inside a budget cap is the version of this that actually gets adoption.

The free first 500 activations will tell you fast whether the retention follows.

Cold-stored XRP → yield vaults in two XRPL signatures.

➜ @DCENTWALLETS is now a native XRPFi access point through Flare Smart Accounts.

No more new wallet, FLR gas management and bridging.

Users sign directly from hardware: FXRP mints on Flare and deploys into vaults automatically.

D’CENT has deep roots across Asia and Korea specifically, which is exactly why this integration matters for XRPFi distribution.

The bottleneck was never protocol quality.

It was putting yield access inside the wallets XRP holders already trust.

🔗 Easiest and safest place to put your XRP to work: https://t.co/iz6gxGDuYy

❗️D'CENT supported at launch, with more wallet integrations coming

Platforms still treat perps and options like separate worlds.

And honestly talking, it’s a nightmare for managing margin.

I moved my setup to @aevoxyz because it’s the first place where I can actually run a unified account.

Directional perps and hedging with options from can be traded through one single balance.

The best part is that I don't have to cycle into stables to trade.

I keep my $BTC and $ETH as collateral so they stay in my portfolio while I work.

Want to try their "PERPS+" for one-click structured trades??

🔗 Use my link for a 10% discount on fees: https://t.co/SBCAzGMEQx

Many will read the @grvt_io x @centrifuge announcement as another RWA integration.

But the counterparty selection tells a different story.

Coinbase made a strategic investment in Centrifuge last week and named it preferred tokenization infrastructure on Base.

- S&P Global gave it the highest tokenized fund rating in the category

- Spark allocated $200M to it in a $1B Grand Prix

- Janus Henderson's JTRSY already sits at $1.4B market cap

This infrastructure has been validated at every layer before grvt touched it.

What actually changes with this partnership though: idle margin earning institutional Treasury yield from $1, no bridging, no custody handoff, collateral stays fully tradable throughout.

That gap between how capital behaves inside a perp DEX today and how it behaves inside Grvt after this integration has a name.

One Balance. Infinite Productivity.

Oil is quietly becoming one of the most important charts to watch if you’re long $ETH

The chart is hard to ignore.

Crude has been grinding higher since the war began.

ETH moved the other way.

Now back near $2,100 and still far from its cycle highs.

WTI and Brent pushed higher again after Trump’s Strait of Hormuz comments.

ETF outflows are adding pressure.

Exchange reserves are rising.

Whales are distributing.

ETH is still underperforming BTC.

But the structural case is not dead.

60%+ RWA market share.

BlackRock and JPMorgan live on Ethereum.

Agentic AI payment rails still point back to ETH.

So the real question is simple:

Does oil peak before the market loses patience with the thesis?

Most coverage of Alpenglow frames it as a speed upgrade.

That misses the point.

Finality dropping from 12.8 seconds to 100 to 150 milliseconds is a category change.

The apps it enables barely exist onchain today 👇

◢ What Alpenglow Brings

Alpenglow replaces Solana’s current consensus stack.

Approved by 98.27% of validators in September 2025, it swaps Proof of History, TowerBFT, and Turbine for Votor and Rotor.

Votor compresses TowerBFT’s 32 round voting process into one or two rounds.

With 80%+ validator stake online, finality lands around 100ms.

With 60 to 80% participation, it takes two rounds and around 150ms.

Both paths run together, and the winner finalizes the block.

The bigger shift is that Votor moves voting offchain.

BLS aggregation combines thousands of validator signatures into one small certificate.

Today, validator votes make up around 75% of all Solana transactions.

Alpenglow removes that overhead and frees major block space for real user activity.

Rotor replaces Turbine’s relay structure with direct validator to validator communication.

Fewer hops means faster propagation.

◢ The Design Space At 100ms

Solana DeFi today relies on optimistic confirmation.

Protocols treat transactions as settled after 2 to 3 seconds because waiting 12.8 seconds for true finality is not commercially viable.

At 100 to 150ms finality, three DeFi categories change completely.

Order book DEXs can offer real price discovery with a much smaller front running window.

Onchain order books can move closer to CEX latency while staying permissionless.

Liquidation systems can react in real time.

At 100ms, the delay between detecting bad debt and confirmed settlement starts to look like centralized infrastructure.

Options and structured products also become more practical.

Sub second finality allows expiry mechanisms and payoff structures that need near instant confirmation.

◢ The Fault Tolerance Tradeoff

Alpenglow uses a 20+20 framework.

It tolerates up to 20% Byzantine validators and 20% crashed validators at the same time.

Traditional BFT supports up to 33% faulty nodes, so pure Byzantine tolerance drops from 33% to 20%.

The tradeoff reflects how real networks fail.

Because 80% plus 60% equals 140%, conflicting forks cannot both reach quorum.

Safety holds, and liveness still holds even if 20% of stake goes dark.

For DeFi, this matters because Solana outages during congestion have historically hurt protocols the most.

Alpenglow’s fixed 400ms block time and local clock timeouts remove TowerBFT’s stress failure mode at the architecture level.

◢ Validator Economics

Onchain voting currently takes up a huge share of Solana throughput.

For smaller validators, voting costs are a real operating expense.

That structurally pushes stake toward larger operators.

Alpenglow removes onchain voting completely.

This lowers the breakeven point for running a validator.

Lower costs mean less pressure on smaller operators.

Solana’s decentralization profile should improve as a mechanical result, not just as a stated goal.

◢ Competitive Map Change

Ethereum post Glamsterdam targets around 10,000 TPS on L1 with 12 second block times.

Full cryptographic finality on Ethereum still takes 12 to 13 minutes.

Solana post Alpenglow targets 100 to 150ms finality with comparable throughput.

These chains are no longer competing for the exact same applications.

Ethereum’s thesis is composability, security, and deep liquidity.

Solana’s post Alpenglow thesis is raw execution speed for apps that need near real time finality.

The Coinbase and Hyperliquid USDC integration is the institutional signal.

Coinbase chose a high performance execution environment as a primary USDC deployment target.

Alpenglow makes Solana competitive on the metric that justified separate chains: finality speed.

Mainnet is targeted for Q3 2026 if testing holds.

Do protocols exist to capture the design space Alpenglow opens before the window closes?

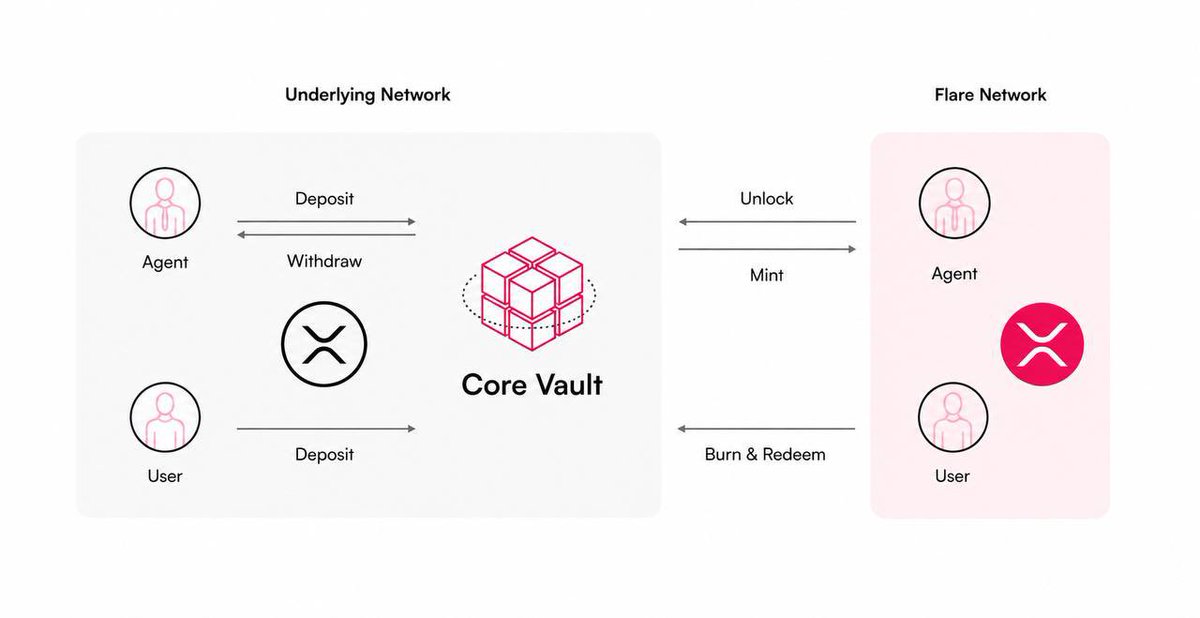

Big slice of $XRP supply has never touched DeFi.

Not because holders don’t want yield. Because the path to get there was genuinely broken.

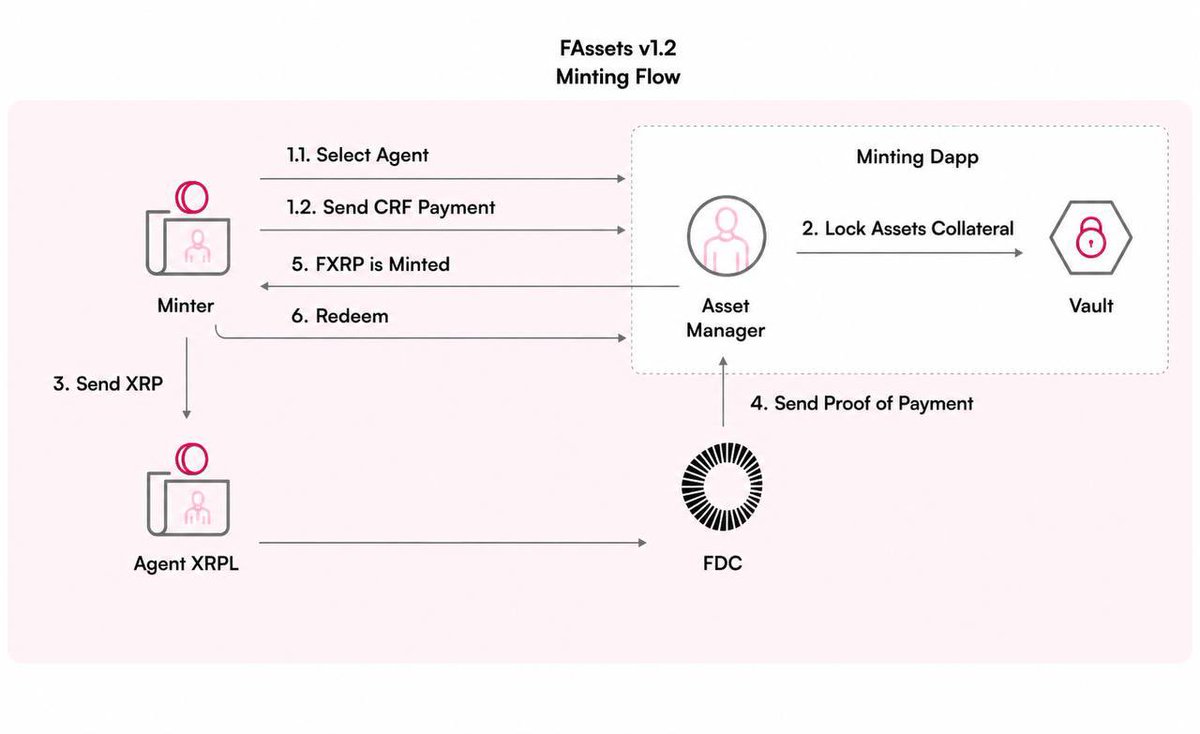

FAssets v1.3 mainnet went live on @FlareNetworks to fix it 👇

◢ The Structural Problem

XRP is the second largest non-stablecoin asset by exchange holdings.

Almost none of it is in DeFi.

Before v1.3, minting FXRP required selecting a specific agent, working around their collateral availability, completing a reservation step, and executing smart contract interactions that no exchange supports natively.

Exchanges process withdrawals as standard XRPL transactions out of hot wallets.

They don’t run Flare contract logic on behalf of users.

That mismatch meant the XRP sitting across Binance, Kraken, OKX, Coinbase and everywhere else was operationally unreachable by FAssets.

The infrastructure existed. The distribution path didn’t.

◢ What v1.3 Changes

v1.3 reduces the entire mint flow to a single XRPL transaction with a destination tag.

Reserve a tag once, map it to your Flare address, and every mint after that runs as a standard XRPL withdrawal.

An executor relays proof of payment to Flare where the mint completes.

Destination tags are already how every exchange credits accounts, how every custodian routes payments, how every XRPL wallet labels deposits.

Flare didn’t ask the XRP ecosystem to learn something new. They built the mint path around what already exists everywhere.

Redemption mechanics are unchanged: agents, overcollateralization, liquidation rails all remain in place on the way out.

The safety model is intact. The entry point moved.

◢ Why No Bridge Competes

This is worth being precise about.

Squid, wXRP, and other bridge solutions don’t offer a CEX-direct mint path in the same class as v1.3. A destination-tagged XRP withdrawal that routes directly into another chain’s DeFi ecosystem is a Flare-specific capability: nothing else has built this for XRP at the exchange layer.

155 million FXRP minted and the ecosystem hasn’t come close to the available surface.

The reason is distribution, not demand.

◢ Exchange and Wallets Calculus

Exchanges are built to keep users on their own rails.

That’s rational. v1.3 changes what it costs them to change that.

The integration surface for FXRP minting went from “build Flare-aware contract choreography into your withdrawal flow” to “treat it as a destination-tagged XRP withdrawal.”

That’s a fundamentally different conversation to have with an exchange’s engineering team. The barrier dropped.

The first exchanges to move get the XRPFi narrative.

The ones that wait explain to users why competitors have it.

Flare doesn’t need to apply pressure. The race runs itself.

◢ What’s Actually Unlocked

v1.3 sits between v1.2 and the full v2 vision: it pulls forward direct minting and tag-based routing without touching the redemption-side collateral structure.

What it actually delivers is distribution surface.

Wallets, exchanges, custodians that already route XRP through destination tags now have a direct integration path for FXRP minting.

An exchange withdrawal becomes a mint. A custodian flow does the same.

XRPFi doesn’t scale through more apps built on Flare alone.

It scales when the surfaces XRP holders already trust can move them into productive onchain positions without asking them to change tools.

v1.3 isn’t the product. It’s the precondition.

Uphold, VivoPower, every integration Flare has lined up: none of it scales without a mint path that exchanges and custodians can actually run.

That path exists now. The floodgates aren’t a metaphor anymore.

XRP sitting in cold storage is such a missed opportunity.

The XRP Alliance pulls the entire Ripple ecosystem into one hardware wallet.

RLUSD, @FlareNetworks integrations, cross-chain swaps, fiat on-ramps. Zero extra fees. Full self-custody throughout.

Flare Campaign opens May 19.

Perfect timing to wake up those sleeping assets!

Web3 "metaverses" still ask you to configure a wallet, mint an avatar, bridge funds and read three articles before you can look at anything.

PanduVerse by @pandulabs is different because lets you walk in easily.

Real-time multiplayer, live chat, video billboards, animated environment and a guest mode that removes every barrier between curiosity and actually being there.

That frictionless entry is harder to build than it looks and most projects never bother.

The beta is live.

Worth five minutes of your time to feel the difference!

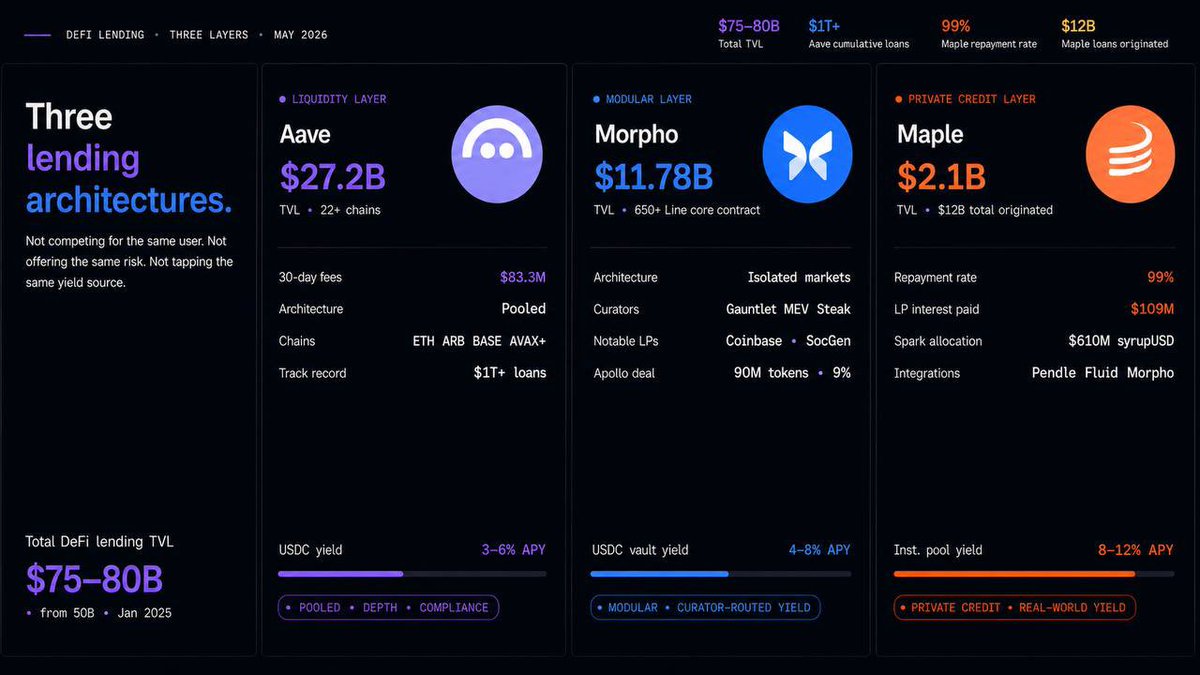

“Where should I lend in DeFi?” is the wrong question.

The right question is: what kind of lender are you?

Because the three protocols that now dominate DeFi lending are not competing for the same user 👇

◢ Market Context

DeFi lending TVL crossed $75-80 billion in April 2026, up from $50 billion at the start of 2025.

✚ Aave crossed $1 trillion in cumulative loans, a first for the sector

✚ Morpho hit $11.78 billion in TVL on May 12, becoming the clear second-largest lending protocol

✚ Maple sits at $2.1 billion with a 99% repayment rate and $12 billion in total loans originated since 2021

Three protocols. Three architectures. Three different bets on DeFi lending.

◢ The Liquidity Layer: Aave

Aave is the benchmark.

✚ $27.2 billion in TVL

✚ 22+ chains

✚ $83.3 million in fees over the past 30 days

Its architecture is pooled: every USDC supplier earns the average rate generated by that pool’s borrowing demand.

Aave’s depth means large positions can move with minimal friction, while its multi-chain footprint gives access to markets across Ethereum, Arbitrum, Base, Avalanche, and more.

Current USDC yield: 3-6% APY depending on chain and utilization.

◢ The Modular Layer: Morpho

Morpho’s core contract is 650 lines of Solidity.

The architecture separates three functions other lending protocols bundle together:

✚ Market creation

✚ Risk curation

✚ Liquidity provision

Anyone can create an isolated market with custom parameters: loan asset, collateral asset, LTV ratio, oracle, and interest rate model.

Curators like Steakhouse Financial, Gauntlet, and MEV Capital assemble those markets into Vaults that optimize depositor yield.

USDC vault rates often run 4-8% APY, outperforming Aave on equivalent assets because capital is routed to stronger borrowing demand.

✚ Coinbase chose Morpho as infrastructure for its USDC lending product

✚ Apollo Global Management signed a 48-month agreement to acquire up to 90 million MORPHO tokens, around 9% of total supply

✚ Société Générale deploys through Morpho vaults

Choosing a vault means choosing a curator, and curator quality affects returns.

◢ The Private Credit Layer: Maple

Maple is not really competing with Aave or Morpho at the protocol level.

It is bringing institutional private credit onchain.

Capital providers supply stablecoins to professionally managed pools, while borrowers draw loans at pre-agreed rates with off-chain credit assessment and on-chain enforcement.

syrupUSD turns this into a permissionless entry point: deposit USDC and receive yield-bearing tokens backed by short-duration overcollateralized loans.

The numbers behind this model are unusual for DeFi:

✚ $12 billion in total loans originated since 2021

✚ $109 million in interest paid to LPs

✚ 99% repayment rate

✚ syrupUSD integrated with Spark, Morpho, Fluid, and Pendle

✚ Spark allocated $610 million to syrupUSD pools directly

Permissioned institutional pools sit around 8-12% APY, structurally higher because Maple accesses a different risk market.

◢ Three Lenders, Three Markets

The common mistake is applying a retail liquidity framework to a decision that requires understanding architecture.

✚ If your priority is depth, chain coverage, and zero setup: Aave

✚ If your priority is optimized stablecoin yield with professional risk management: Morpho, and spend 20 minutes choosing a curator

✚ If your priority is the highest available dollar-denominated yield with a defined risk model: Maple’s syrupUSD, or institutional pools if you qualify

The protocols are not interchangeable.

They were built for different users, risk models, and yield sources.

The $75-80 billion across DeFi lending is not one homogeneous pool of capital. It is three distinct markets running in parallel on the same rails.

Which layer is your capital actually in and why?

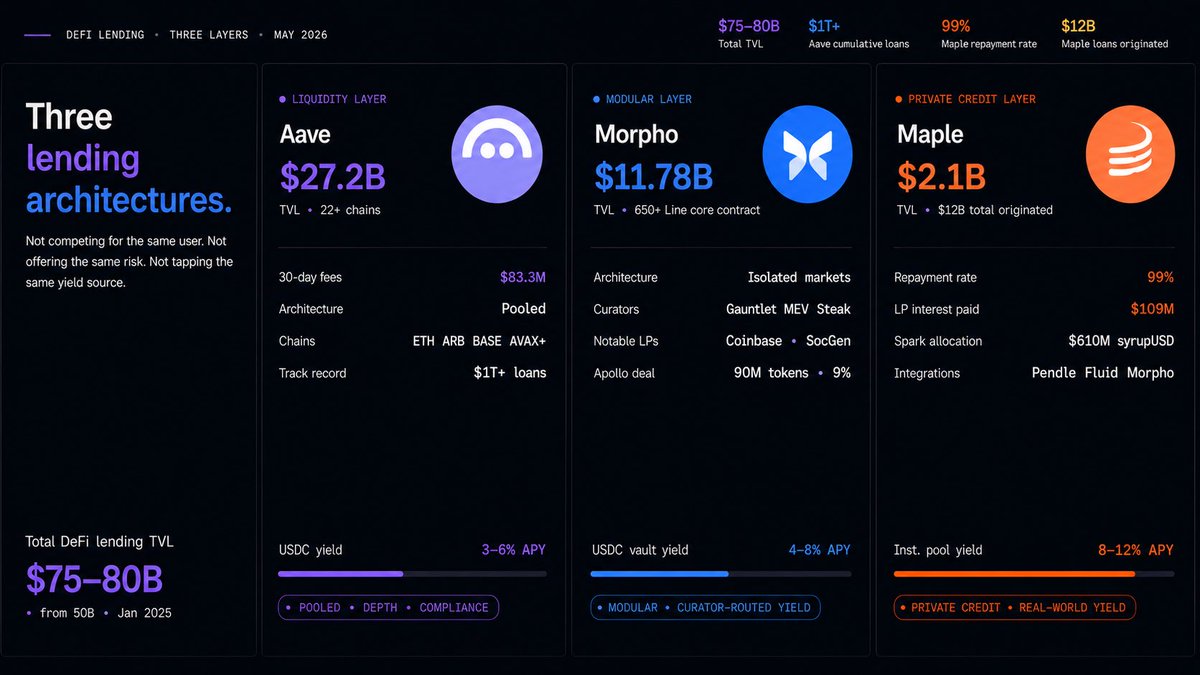

“Where should I lend in DeFi?” is the wrong question.

The right question is: what kind of lender are you?

Because the three protocols that now dominate DeFi lending are not competing for the same user 👇

◢ Market Context

DeFi lending TVL crossed $75-80 billion in April 2026, up from $50 billion at the start of 2025.

✚ Aave crossed $1 trillion in cumulative loans, a first for the sector

✚ Morpho hit $11.78 billion in TVL on May 12, becoming the clear second-largest lending protocol

✚ Maple sits at $2.1 billion with a 99% repayment rate and $12 billion in total loans originated since 2021

Three protocols. Three architectures. Three different bets on DeFi lending.

◢ The Liquidity Layer: Aave

Aave is the benchmark.

✚ $27.2 billion in TVL

✚ 22+ chains

✚ $83.3 million in fees over the past 30 days

Its architecture is pooled: every USDC supplier earns the average rate generated by that pool’s borrowing demand.

Aave’s depth means large positions can move with minimal friction, while its multi-chain footprint gives access to markets across Ethereum, Arbitrum, Base, Avalanche, and more.

Current USDC yield: 3-6% APY depending on chain and utilization.

◢ The Modular Layer: Morpho

Morpho’s core contract is 650 lines of Solidity.

The architecture separates three functions other lending protocols bundle together:

✚ Market creation

✚ Risk curation

✚ Liquidity provision

Anyone can create an isolated market with custom parameters: loan asset, collateral asset, LTV ratio, oracle, and interest rate model.

Curators like Steakhouse Financial, Gauntlet, and MEV Capital assemble those markets into Vaults that optimize depositor yield.

USDC vault rates often run 4-8% APY, outperforming Aave on equivalent assets because capital is routed to stronger borrowing demand.

✚ Coinbase chose Morpho as infrastructure for its USDC lending product

✚ Apollo Global Management signed a 48-month agreement to acquire up to 90 million MORPHO tokens, around 9% of total supply

✚ Société Générale deploys through Morpho vaults

Choosing a vault means choosing a curator, and curator quality affects returns.

◢ The Private Credit Layer: Maple

Maple is not really competing with Aave or Morpho at the protocol level.

It is bringing institutional private credit onchain.

Capital providers supply stablecoins to professionally managed pools, while borrowers draw loans at pre-agreed rates with off-chain credit assessment and on-chain enforcement.

syrupUSD turns this into a permissionless entry point: deposit USDC and receive yield-bearing tokens backed by short-duration overcollateralized loans.

The numbers behind this model are unusual for DeFi:

✚ $12 billion in total loans originated since 2021

✚ $109 million in interest paid to LPs

✚ 99% repayment rate

✚ syrupUSD integrated with Spark, Morpho, Fluid, and Pendle

✚ Spark allocated $610 million to syrupUSD pools directly

Permissioned institutional pools sit around 8-12% APY, structurally higher because Maple accesses a different risk market.

◢ Three Lenders, Three Markets

The common mistake is applying a retail liquidity framework to a decision that requires understanding architecture.

✚ If your priority is depth, chain coverage, and zero setup: Aave

✚ If your priority is optimized stablecoin yield with professional risk management: Morpho, and spend 20 minutes choosing a curator

✚ If your priority is the highest available dollar-denominated yield with a defined risk model: Maple’s syrupUSD, or institutional pools if you qualify

The protocols are not interchangeable.

They were built for different users, risk models, and yield sources.

The $75-80 billion across DeFi lending is not one homogeneous pool of capital. It is three distinct markets running in parallel on the same rails.

Which layer is your capital actually in and why?

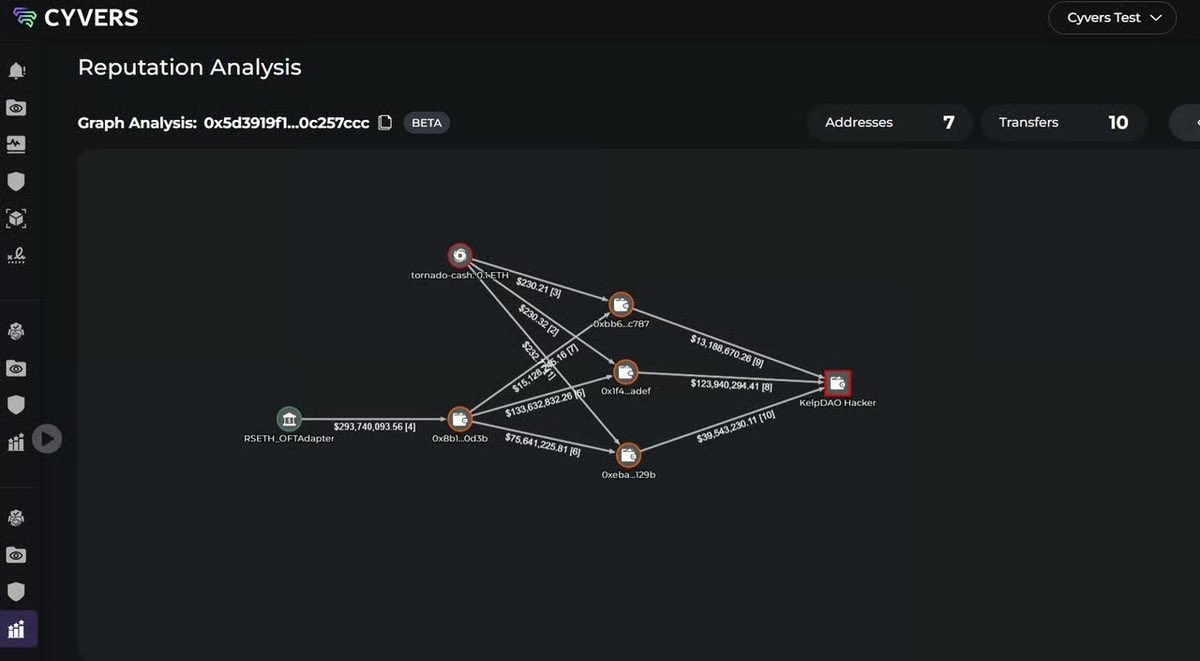

Kelp burned the exploiter’s 117,132 rsETH.

The move is part of a two-week recovery window with withdrawals tentatively live within 24 hours.

What OpenZeppelin flagged is the part worth sitting with: the system failed operationally.

That’s a fundamentally different category of risk and most DeFi protocols are exposed to the same thing right now without knowing it.

Chainlink CCIP migration, four independent attestors, 64 block confirmations.

The rebuild is serious.

But when users get their withdrawal button back after a $293M Lazarus hack… do they exit or do they stay? 👀

Everyone is watching $BTC around $80K.

But the real story may be underneath.

Stablecoins are quietly becoming the settlement layer of the internet.

➜ $USDC supply is up 28% to $77B and transaction volume jumped 263% to 21.5T.

That is not hype.

That is payment infrastructure finding product market fit.

The next cycle may not be won by the loudest narratives.

It may be won by whoever owns distribution, wallets, stablecoin rails, and real payment flow.

PumpFun made $971M in 2025.

Now it’s annualizing at $320M in 2026.

The bonding curve model works. But the moat is cracking… and every major chain has noticed.

Here’s what the data shows 👇

◢ The Machine

January 2024. @Pumpfun launches on Solana.

Key principles: a bonding curve, a token factory, and a $0.02 launch fee.

By July 2025 it had generated $677M in protocol revenue before it even had a native token.

✚ The PUMP ICO sold out in under 12 minutes at a $4B FDV

✚ $138M in a single month

✚ $15.5M in a single day

For context: more daily revenue than most mid-sized CEXs were posting at the time.

And Solana built the infrastructure that made the cycle possible.

◢ The Numbers

2025 full-year launchpad data on Solana:

✚ 11.6M tokens created, more than double 2024

✚ 105,000 graduated off bonding curves

✚ 0.89% success rate

✚ $762M in combined launchpad revenue

✚ 6 platforms each crossed $1B in trading volume

The ecosystem produced extraordinary fee revenue from tokens that mostly went to zero.

The operators sell picks and shovels. The gold rush does the rest.

◢ BNB Moment

October 9, 2025. CZ tweets “#BNB meme szn.”

What happens next is worth tracking:

✚ BNB Chain DEX volume hits $20.5B in 24 hours, topping Solana’s $12.7B

✚ Four meme posts $1.43M in protocol fees vs PumpFun’s $1.14M

✚ 812,000 daily unique users on Four meme

✚ Over 600 new tokens deployed in the first hour

One tweet. One day. A data point. But the first time the gap closed.

BNB’s edge is Binance itself: 100M+ users, wallet integration, and CZ’s ability to activate retail globally in a post.

The question is whether activation can be sustained without a permanent narrative.

◢ Tron: The Flash Peak

SunPump launched August 2024 with Justin Sun’s $10M incentive program behind it.

On August 21, 2024 it briefly flipped PumpFun in daily token launches: 7,500 vs 6,900 and posted $3.84M in daily fees, Tron’s highest at the time.

2.35M active wallet addresses in a day. More than any network, including Solana.

Then incentives ran out.

By early 2025, Tron’s memecoin market cap sat around $80M vs Solana’s $9.73B.

SunPump’s story matters because of how it ends: distribution without community is a spike, not a cycle.

Justin Sun can bring users to a chain but he can’t make them stay.

◢ Base: The Slow Burn

Where Solana memecoins peak fast and crash hard, Base tokens show longer survival curves.

A clear signal about the user cohort more than the platform.

✚ Zora lets creators launch tokens with a single tweet.

✚ Flaunch and BoopFun give builders infrastructure without Coinbase’s direct stamp.

The edge is structural: Coinbase’s regulatory positioning, 100M+ user base, and the implicit compliance cover institutional capital needs.

Base is building the venue the next cycle runs through when CT stops being the only audience.

◢ PumpFun Current Positioning

The cycle has turned.

$971M revenue in 2025. Annualizing at ~$320M in 2026.

Monthly trading volume down from $11.6B in Jan 2025 to $2.1B in Jan 2026.

But the business is restructuring:

✚ PUMP token launched July 2025, raised $1B in 12 minutes

✚ 36% of circulating supply permanently burned in April 2026

✚ 50% of future net revenue locked into buybacks via smart contract

✚ Platform expanding to WBTC, USDC, and external token trading

✚ Multi-chain expansion signals across Ethereum and Monad

73% of active wallets now profitable as of April 2026, up from 30% at the June 2025 low.

The casino still has the house edge. But the operator is getting smarter about who it lets in.

◢ Conclusion

The bonding curve is not a moat.

Any chain can deploy one. BNB did. Tron did. Sui did. More will.

The actual moat is liquidity depth, wallet density, developer velocity, and the cultural layer that makes degens choose one chain’s tokens without thinking about it.

Solana has all four for me.

The next retail wave lands somewhere.

Which chain is ready when it does?

Crypto projects spend all on the token and nothing on what makes people actually care.

IP is the long game.

A registered character design goes beyond a legal formality… it’s the first brick in building something that outlasts a market cycle.

The asset that keeps generating value when the hype is gone.

@pandulabs filing for US copyright before the narrative catches up is the kind of quiet move that looks obvious three years from now.

Bitcoin dominates 60% of total crypto market cap.

$1.4 trillion.

Yet only 0.46% of all $BTC is in DeFi.

That number is the entire thesis 👇🏻

◢ Long story short

BTCFi TVL went from $304 million in January 2024 to over $7 billion by December 2024.

A 22x in one year.

Then momentum faded.

Bitcoin L2 TVL fell 74% from peak, while total BTCFi TVL dropped from 101,721 BTC to 91,332 BTC.

The ecosystem grew faster than almost anything in DeFi, then stalled.

Tiger Research even revised its BTCFi fundamental indicator down to its Q2 2026 floor, noting that surface-level growth has not become real network expansion.

◢ Where the growth is concentrated

Babylon holds 56,853 BTC in native staking vaults.

That is $5.6 billion TVL, without wrapping or bridging.

Native BTC. Full self-custody.

The token side is more interesting.

BABY is still down massively from its April 2025 all-time high, yet Babylon sits at roughly $78 million market cap against $5.6 billion TVL.

That ratio is either a screaming signal or a warning that TVL and token value are completely disconnected.

✚ a16z invested $15 million into Babylon in January 2026 to develop Trustless Bitcoin Vaults, letting users lock native BTC on Bitcoin while using it as verifiable collateral elsewhere.

✚ Bedrock reached $1.2 billion TVL through uniBTC and brBTC after integrating with Babylon.

✚ Lombard sits around $1 billion. Stacks at $208 million.

✚ Rootstock is targeting the $260 billion in idle institutional Bitcoin through vault strategies.

◢ The structural problem

The Block said it clearly in its 2026 Digital Assets Outlook:

copying EVM DeFi primitives onto Bitcoin chains is not enough to attract liquidity or developers.

That is the honest diagnosis.

BTCFi has restaking covered. Babylon and Lombard own that lane.

But it still lacks:

✚ a mature lending market

✚ a DEX with real liquidity

✚ a meaningful stablecoin layer

Rootstock has 150 partners and eight years of uptime, yet its TVL is still a fraction of Babylon’s.

The composability layer that makes Ethereum DeFi useful at scale has not really appeared on Bitcoin.

Babylon’s multi-staking model, where one BTC deposit secures multiple networks, is the closest thing so far.

◢ The institutional argument

At Consensus Miami 2026, Adam Back said sovereigns, pension funds, and treasury companies are the next wave of Bitcoin adoption.

These entities already hold BTC.

They are not just speculating on price.

They want yield.

Predictable, auditable, non-custodial yield on an asset they already own.

✚ Rootstock’s institutional initiative and Animoca Japan’s corporate treasury deployment are targeting that exact use case.

✚ Babylon’s Trustless Bitcoin Vaults are the infrastructure version of the same bet.

If native BTC can become usable collateral in DeFi without leaving the Bitcoin security model, the addressable market is not the 0.46% currently in BTCFi.

It is the 99.54% that is not.

◢ An honest framing

BTCFi is winning narrowly in native staking, where Babylon and Lombard have built something real.

But the rest is still early.

✚ lending is underdeveloped

✚ Bitcoin L2 TVL is contracting

✚ most BTCFi primitives have not attracted meaningful usage

Still, 0.46% is not just a weakness.

It is a gap.

Either Bitcoin holders have made a philosophical choice to keep BTC inert, or the infrastructure to make it productive is arriving now and the market has not priced it yet.

Both can be true at the same time.

What is your point of view?

AI projects still talk in abstracts.

210k submissions in a single week tells me something very different: people are actually showing up and contributing.

@StoryProtocol is building the infrastructure layer quietly in the background, while Numo is proving there’s real demand for human-driven AI data participation with actual earnings attached.

That combination is worth watching.

A lot of projects say they’re building for the long term.

Very few are willing to make supply tighter while attention is growing.

@pandulabs is one of them.

Burning 284M+ $PANDU shows they’re actually thinking about sustainability while the brand is still expanding.

Curious to see where they take it from here

Been thinking about this for a while.

The bottleneck for AI agents was never the model. GPT-4 level reasoning has existed for two years.

The bottleneck was always: how does an agent pay for things without a human babysitter?

And now @kojiru_com is fixing it.

Pre-funded wallets are a dressed-up to-do list.

The agent stops, you get pinged, you top up, it continues.

Models Like this are not autonomy but automation with extra steps.

The cold start problem here is real and underappreciated.

No credit history means no credit. No credit means no autonomous action at scale.

Kojiru’s ACS scoring is built specifically for machines, updating after every task.

For me, is also the first serious attempt at solving that loop I’ve seen.

Infra before the narrative catches up is usually where the interesting stuff happens.

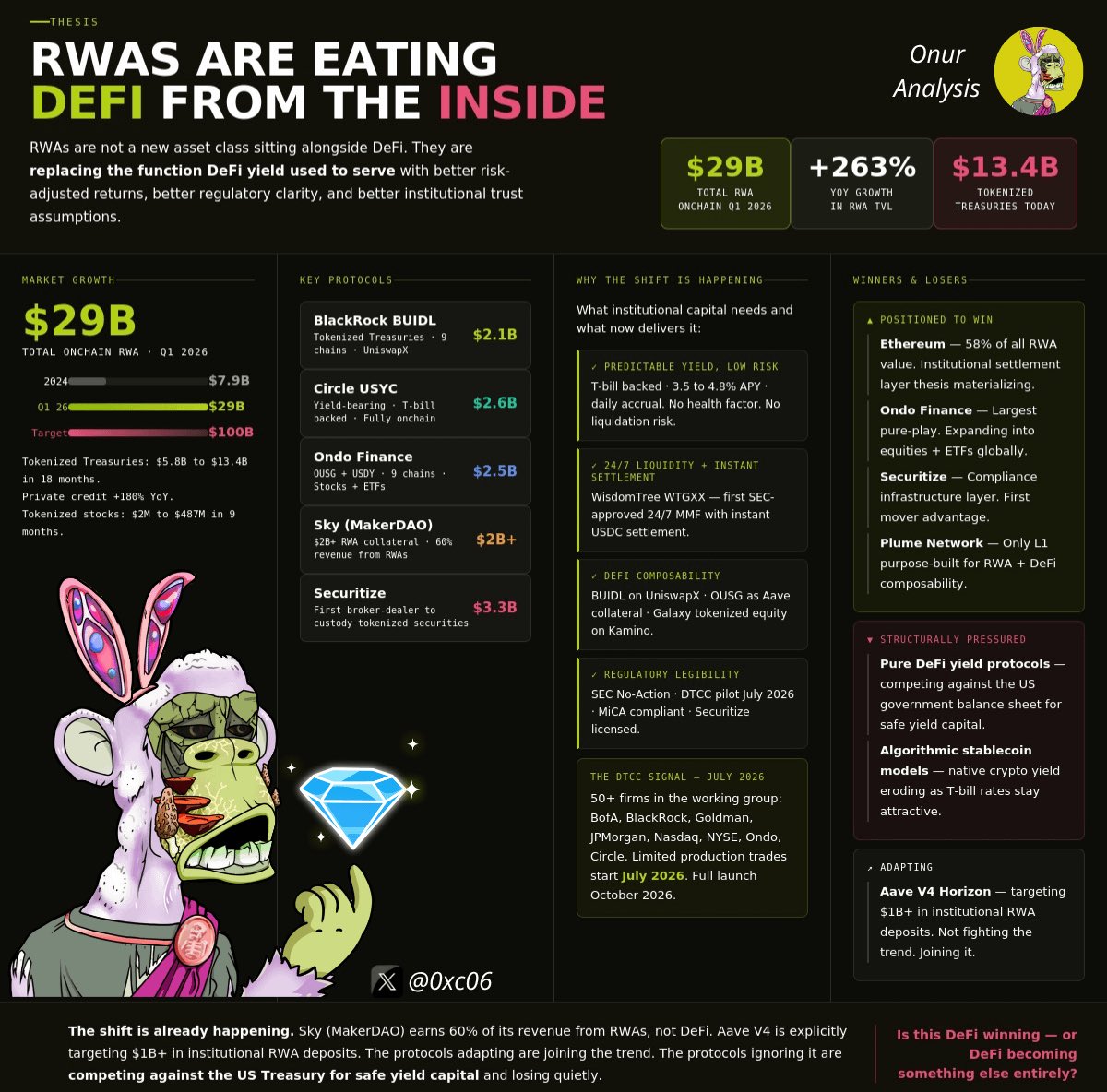

$6.1 billion in tokenized US Treasuries 18 months ago.

$13.4 billion today. Total tokenized RWA market at $29 billion in Q1 2026. +263% year over year.

Do you think it's bullish? This is how it will dismantle the yield layer DeFi was built on.

◢ The yield problem DeFi doesn't want to admit

DeFi's value proposition was always simple: higher yields than tradfi, accessible to anyone with a wallet.

Then US rates climbed above 5%. And the risk-adjusted comparison flipped.

Why take smart contract risk, bridge risk, and liquidation risk for 6% on Aave... when BlackRock's BUIDL on Ethereum pays 4.8% backed by US Treasuries with no health factor to monitor?

Institutional capital stopped trying to answer that question. It left.

◢ In numbers

✚ @BlackRock BUIDL: $2.1B AUM, live on 9 chains, now integrated into Uniswap

✚ @circle USYC: $2.6B market cap, yield-bearing, fully onchain

✚ @OndoFinance: $2.5B TVL across OUSG and USDY, live on 9 blockchains

✚ @SkyEcosystem: $2B+ in RWA collateral generating 60% of protocol revenue from real-world assets

Read again that last one number.

The largest decentralized stablecoin protocol on Ethereum now earns most of its revenue from tokenized real-world assets.

◢ What RWAs are replacing

RWAs shouldn't be considered a new asset class sitting alongside DeFi.

They're replacing the function DeFi yield used to serve... with better risk-adjusted returns, better regulatory clarity, and better institutional trust assumptions.

What does a treasury desk actually need?

✚ Predictable yield with low counterparty risk

✚ 24/7 liquidity and near-instant settlement

✚ Onchain composability: usable as collateral, across protocols

✚ Regulatory legibility: something compliance signs off on

Two years ago, nothing in DeFi met all four.

Today BUIDL does. USDY does. WisdomTree's WTGXX just got SEC approval for 24/7 trading with instant USDC settlement.

The product institutional capital was waiting for now exists. Several versions of it.

The DTCC confirmed limited production trades begin July 2026, full launch October with BofA, BlackRock, Goldman, JPMorgan, Morgan Stanley, Nasdaq, NYSE, Ondo, and Circle all in the working group.

This is the post-trade infrastructure of global capital markets being rebuilt onchain.

◢ Winners

✚ Ethereum: 58% of all tokenized RWA value. The institutional settlement layer thesis is no longer theoretical.

✚ Ondo — $2.5B TVL, largest pure-play RWA protocol, now tokenizing equities and ETFs

✚ @Securitize $3.3B under management, first broker-dealer approved to custody tokenized securities

✚ @plumenetwork: only L1 purpose-built for tokenized asset issuance with native DeFi composability

◢ Losers

Basically any protocol whose value proposition is primarily yield generation.

You're now competing against the US government's balance sheet.

@aave already knows this and their V4 Horizon platform is explicitly targeting $1B+ in institutional RWA deposits.

Protocols that don't adapt will watch TVL quietly migrate toward instruments offering T-bill yield with DeFi mechanics.

◢ Conclusions

Analysts project $100B in tokenized RWAs by end of 2026: a further 3-4x from here.

If that happens, "DeFi TVL" starts looking fundamentally different.

✚ Less algorithmic. Less reflexive.

✚ More institutional. More boring. More real.

RWAs aren't coming to DeFi. They're replacing what DeFi promised to be and delivering it better than DeFi ever did.

Is that the vision winning? Or the vision dying?

Bitcoin ETFs pulled $532M in a single day while $BTC is back above $80K for the first time in 3 months.

Looks clean on the surface.

But 63% of those inflows came from BlackRock alone. Fidelity added most of the rest. Every other fund printed zero.

And the trigger wasn't on-chain. It was a ceasefire agreement between the US and Iran flipping risk sentiment overnight.

The Fed's NFP data this week will do more for price action than anything happening on-chain right now.

Lose $77K-$78K and the narrative flips back fast. That's the level leveraged longs are sitting on.

Is the market actually ready for a world where the Fed press conference matters more than the next halving narrative?

Here you go:

Genuinely didn’t expect to get attached to an AI buddy but here we are.

Started using @pandulabs to bounce ideas off when I’m mid-thought and don’t want to lose the thread.

Now, id the thing I open before I post anything… like a second brain that doesn’t judge the half-baked stuff.

If you haven’t actually sat with it for more than 5 minutes, you’re probably underestimating it !

Been following Pandu from a while now.

And this is probably the first time it actually feels like things are picking up naturally.

Trending on MagicEden and the floor slowly moving at the same time.

Also noticed the IG page growing past 5k which tells me it’s not only crypto people paying attention anymore.

Those phases are usually the ones that matter more

Feels like one to follow closely from here!

🔗 Check the collection with your eyes: https://t.co/3jkIDiNReI

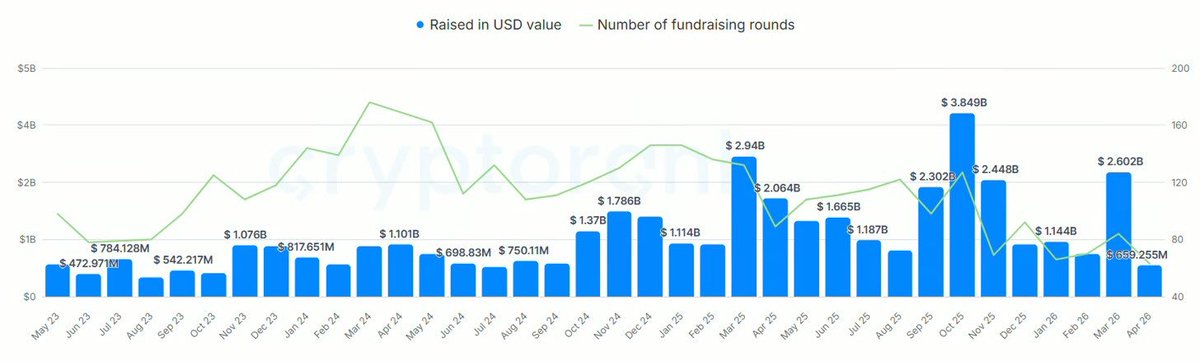

VC funding dropped hard.

Capital pulled back sharply month over month, deal count slowed, and the trend has been drifting lower for months now alongside weaker market conditions.

This usually signals a shift in behavior

less spray and pray, more selective bets

What stands out for me is where activity still exists: DeFi, infra, and AI-linked projects continue to attract attention even as overall funding compresses

So, capital is not leaving but concentrating.

Are we watching a slowdown… or the start of a much tighter capital cycle?

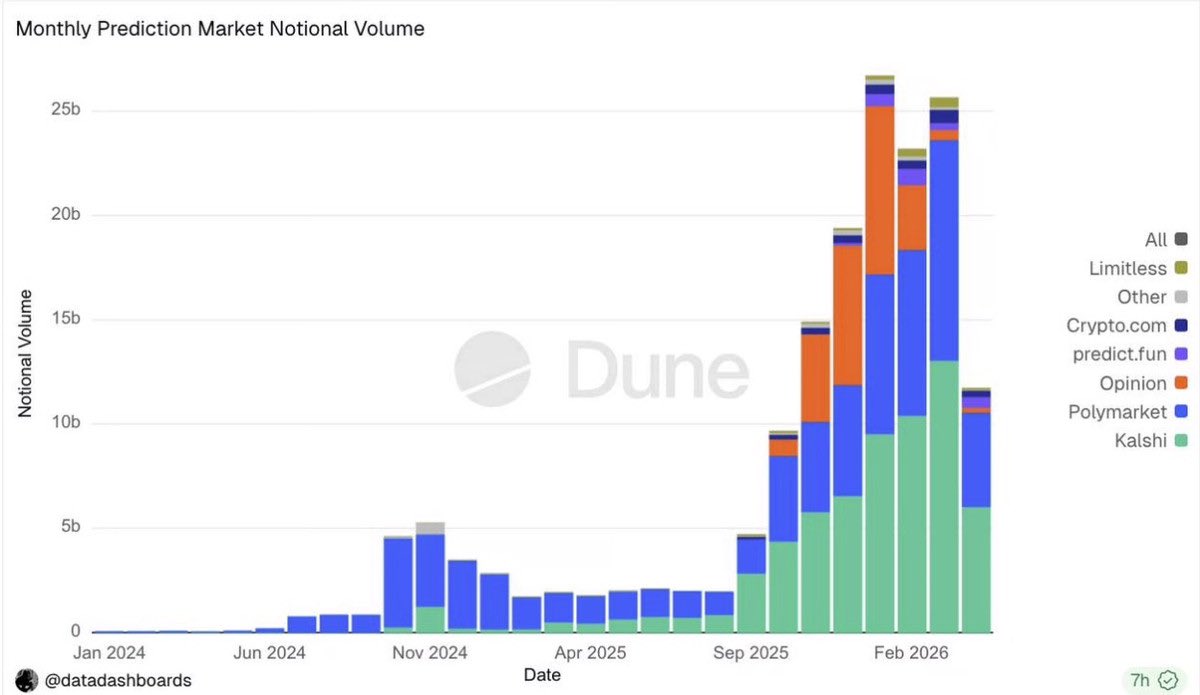

prediction markets are trending lately.

But the more interesting part for me is how people are using them.

Users are no longer showing up only for big events.

More like checking in regularly, placing smaller bets across different topics, building a rhythm.

Mostly retail driving it too, which says a lot.

Sports keeps things active, politics brings attention, but the real shift feels behavioural.

Overall it’s less about one outcome, more about staying engaged over time.

Does this model become how people express conviction going forward?

Treasuries usually look like a number on a dashboard.

But they actually say a lot about how a project thinks over time.

On @Pandupandas, buybacks feeding into a shared pool creates a loop between activity and resources.

More usage → more accumulation → more room to build and expand.

It’s a simple mechanism, but it changes how value circulates inside the system.

🔗 Fully viewable and verifiable on https://t.co/kNL6NegZGH

Most traders are still playing capped games.

@42space flips that.

42 just launched a new product, Price Markets, which introduces a new playbook for trading short-term price action, with uncapped payouts and instant execution.

Instead of guessing direction with up/down, you’re trading where price will land by selecting a range.

Each range = its own outcome token, priced on a bonding curve.

No order books, no MMs, no waiting for order fills.

Prices move with demand, and execution is instant.

What actually matters:

• Early entry → better cost basis as prices move up with time and market maturity

• Payouts scale with the pool → bigger participation, bigger upside.

• Positioning → size into conviction or hedge across adjacent ranges as the market evolves

And the key unlock: the pool is the payout.

If the range you hold wins, it absorbs the entire market pool of the entire event, no fixed ceiling on returns.

→ Your edge comes from being early, and being positioned better than the crowd.

🔗 Talking about it is one thing, but trying it firsthand is different: https://t.co/1RmXLCM8yG

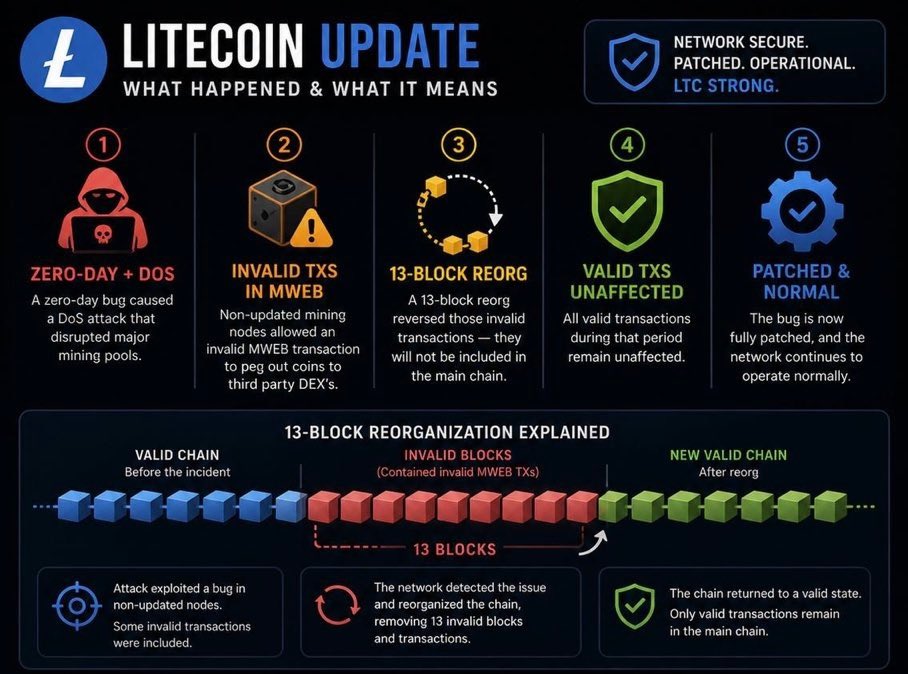

So, Litecoin experienced a 13 block reorg… and it wasn’t as random as it sounds.

A bug + DoS weakened part of the network, older nodes pushed invalid txs, then everything got rolled back once hashpower came back

Nothing “lost” on main chain, but still messy.

What I personally find interesting is that some devs think this wasn’t a true zero-day, more like something known and timed.

This changes the read completely and highlights the usual weak point:

lower hashrate chains + cross-chain activity.

Do events like this start to change how people trust smaller L1s as collateral layers?

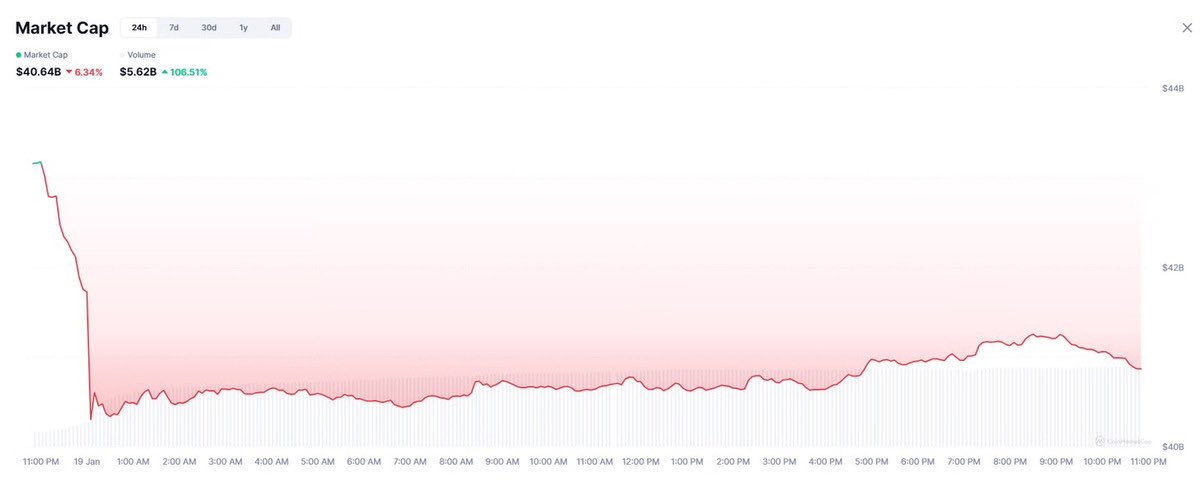

Volume up, market cap down… that’s usually not strength.

Memecoins just did ~$5.6B volume in a day (+100%+) while mcap dropped ~6%.

More than fresh money coming in this is a churn → profit taking, quick flips, capital rotating.

And it cooled fast too: volume already back near ~$3.6B

Seen this before… activity spikes around hype, then fades once fast money exits

Early-year move ($38B → ~$47B) already lost momentum, so this still feels like rotation, not expansion

At the end of the day, memecoins are just a proxy for risk appetite, and that still leans heavily on $BTC direction

So, are we resetting for another rotation… or starting to see appetite actually cool off?

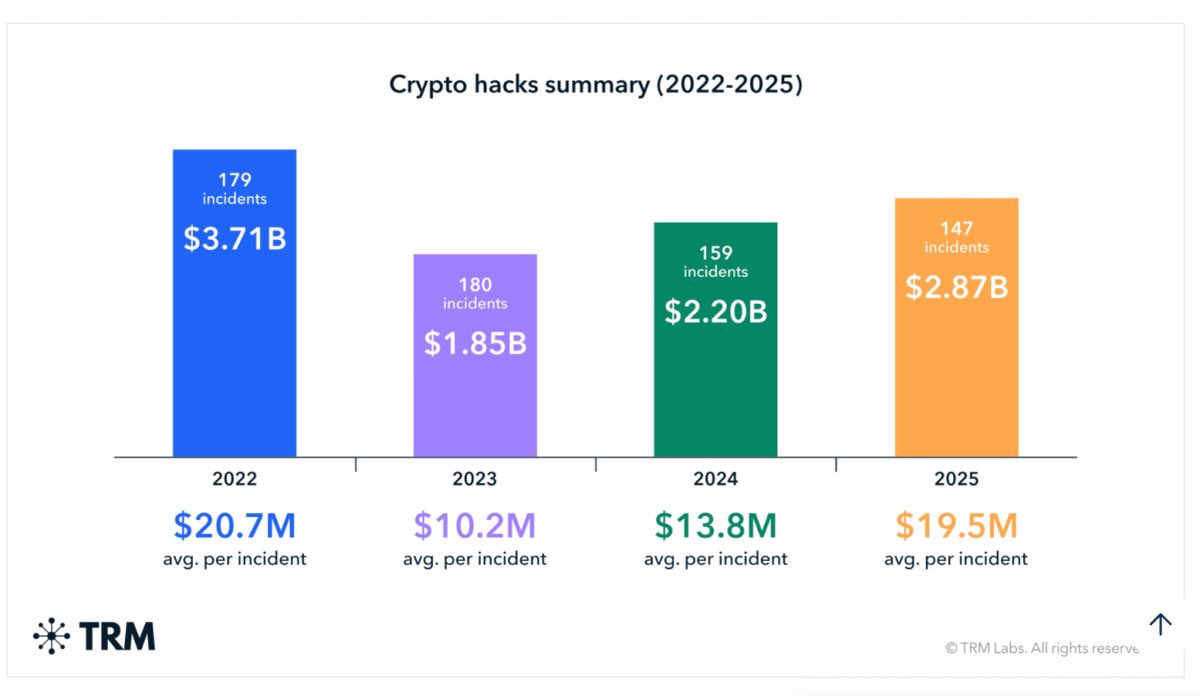

Something’s off about how these recent hacks are happening.

Already $600M+ lost in 2026, and it’s not really about smart contract bugs anymore

Recent attacks are coming from:

– Phishing + AI social engineering

– Deepfakes impersonating teams

– Supply chain hits on infra

– Cross-chain weak points

Kelp (~$293M) is a good example, failure wasn’t code, it was trust in the system around it

At the same time, tools to attack are getting faster and easier to use

So, the surface is expanding while defenses still look pretty basic

How much of this is new risk vs outdated assumptions?

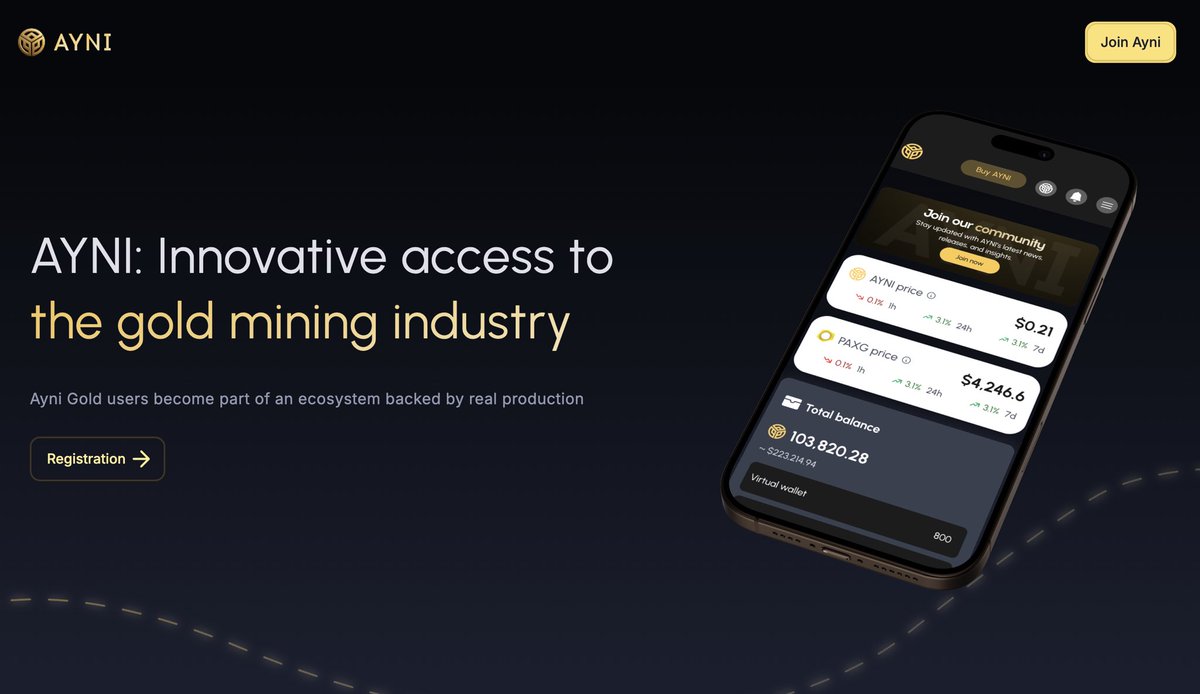

Gold has been absorbing flows again as crypto keeps rotating inside its own loop.

What made me look closer at @aynigold is the model.

Most tokenized gold gives you exposure to the price of gold.

@aynigold brings a different layer onchain by tying exposure to real mining capacity.

Each $AYNI represents 4 cm³/hour in the Minerales SH concession in Peru.

Stake $AYNI and receive PAXG, tokenized gold on Ethereum, with rewards linked to actual mining output from licensed operations in Peru.

Sign Up here 🔗 https://t.co/gf7pXKglD1

That gives the model a far more direct link to real asset activity.

The protocol relies on the fully licensed mining operations of Minerales San Hilario in Peru, and its smart contracts are audited by @CertiK and @peckshield.

If more capital starts moving toward RWAs backed by real production and more predictable reward streams, models like this could sit in a category of their own.

Perpdex volume slowing down rn.

But @grvt_io still gaining share says more than growth during hype cycles.

When the whole sector expands ~4x and one player captures 26x more share, that’s positioning.

What kept my attention even more is the overall design.

Yield on margin changes how capital behaves

idle collateral becomes productive

and once that standard is set, others are forced to adapt.

This is how categories evolve quietly.

Starting to look less like a perpdex

more like a broader onchain finance layer.

Can’t wait to see how far this model can go.

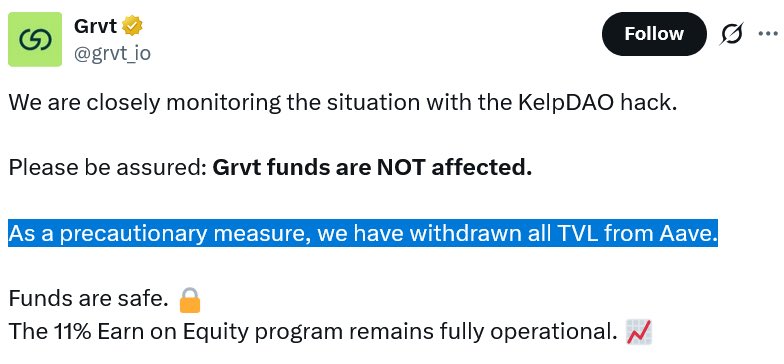

Decentralization gets tested in moments like this.

After the @KelpDAO exploit, Arbitrum froze ~$71M in ETH tied to the attacker, moving funds into a controlled wallet governed by its security council.

The decision followed internal voting and coordination with external authorities.

Technically effective, but it raises deeper questions.

Freezing funds limits damage and protects users, yet it also introduces a layer of discretionary control that many assume doesn’t exist in these systems.

So, where should the line sit between protecting the ecosystem and preserving credible neutrality?

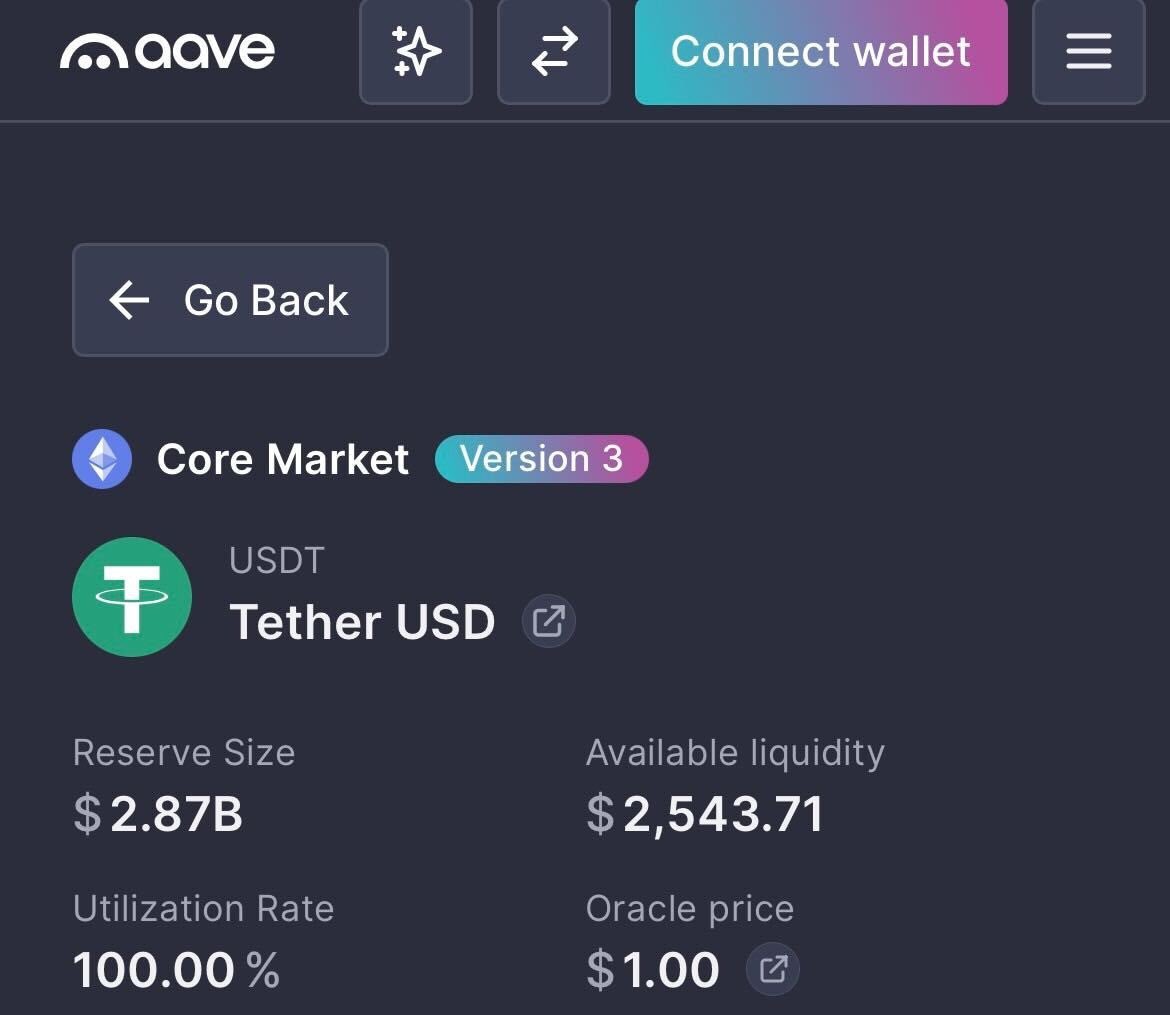

DeFi went through a serious stress moment, and the reaction was instant.

After the Kelp exploit, Aave saw a sharp drop in TVL as capital moved out quickly.

What made it worse was how the attack flowed through the system.

A compromised asset got used as collateral, and suddenly the issue wasn’t isolated anymore.

Liquidity tightened, withdrawals slowed, and confidence took a hit.

This is the tradeoff of deep composability.

It makes DeFi powerful, but also fragile under pressure.

Does this lead to stronger risk frameworks?