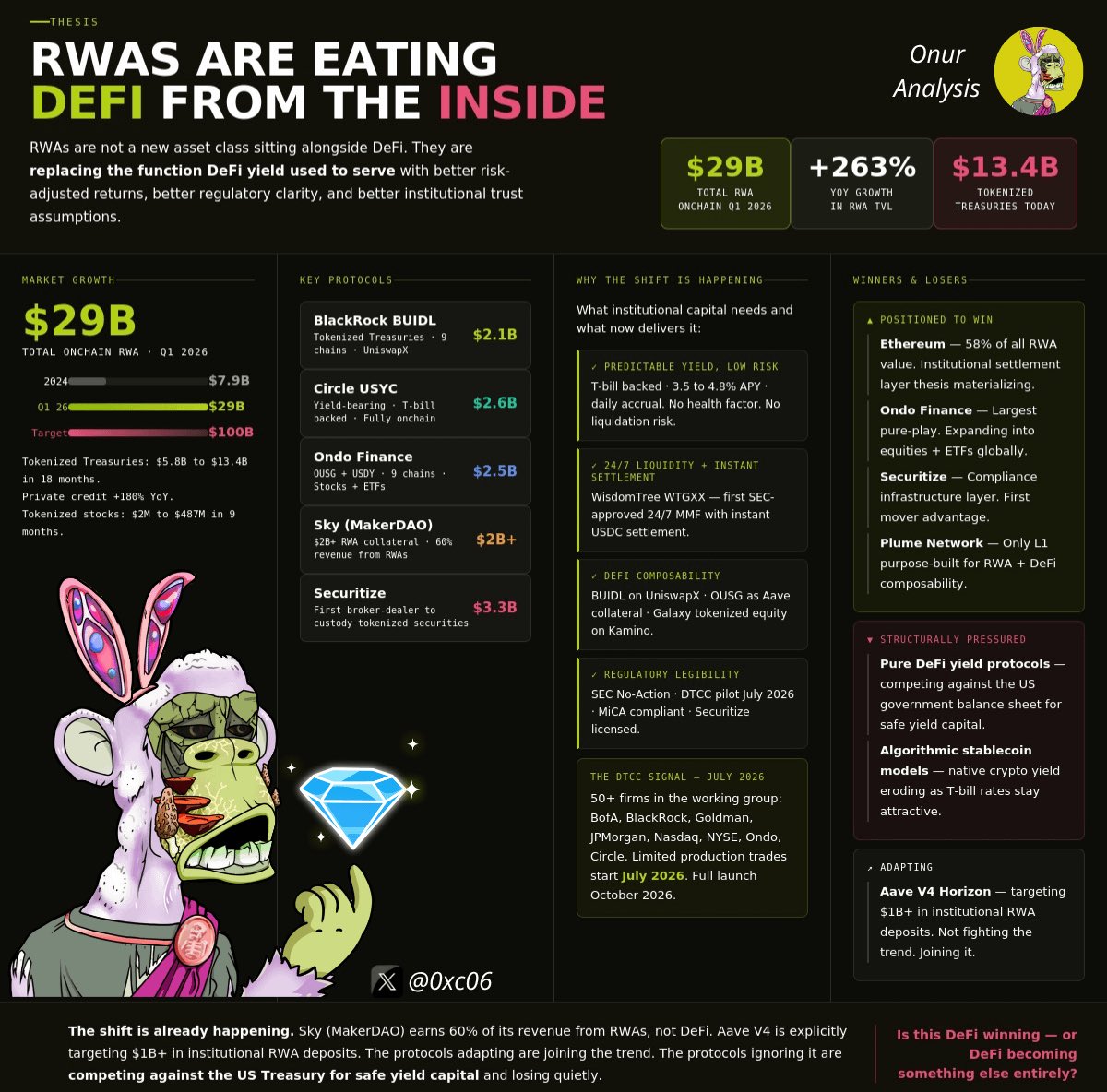

$6.1 billion in tokenized US Treasuries 18 months ago.

$13.4 billion today. Total tokenized RWA market at $29 billion in Q1 2026. +263% year over year.

Do you think it's bullish? This is how it will dismantle the yield layer DeFi was built on.

◢ The yield problem DeFi doesn't want to admit

DeFi's value proposition was always simple: higher yields than tradfi, accessible to anyone with a wallet.

Then US rates climbed above 5%. And the risk-adjusted comparison flipped.

Why take smart contract risk, bridge risk, and liquidation risk for 6% on Aave... when BlackRock's BUIDL on Ethereum pays 4.8% backed by US Treasuries with no health factor to monitor?

Institutional capital stopped trying to answer that question. It left.

◢ In numbers

✚ @BlackRock BUIDL: $2.1B AUM, live on 9 chains, now integrated into Uniswap

✚ @circle USYC: $2.6B market cap, yield-bearing, fully onchain

✚ @OndoFinance: $2.5B TVL across OUSG and USDY, live on 9 blockchains

✚ @SkyEcosystem: $2B+ in RWA collateral generating 60% of protocol revenue from real-world assets

Read again that last one number.

The largest decentralized stablecoin protocol on Ethereum now earns most of its revenue from tokenized real-world assets.

◢ What RWAs are replacing

RWAs shouldn't be considered a new asset class sitting alongside DeFi.

They're replacing the function DeFi yield used to serve... with better risk-adjusted returns, better regulatory clarity, and better institutional trust assumptions.

What does a treasury desk actually need?

✚ Predictable yield with low counterparty risk

✚ 24/7 liquidity and near-instant settlement

✚ Onchain composability: usable as collateral, across protocols

✚ Regulatory legibility: something compliance signs off on

Two years ago, nothing in DeFi met all four.

Today BUIDL does. USDY does. WisdomTree's WTGXX just got SEC approval for 24/7 trading with instant USDC settlement.

The product institutional capital was waiting for now exists. Several versions of it.

The DTCC confirmed limited production trades begin July 2026, full launch October with BofA, BlackRock, Goldman, JPMorgan, Morgan Stanley, Nasdaq, NYSE, Ondo, and Circle all in the working group.

This is the post-trade infrastructure of global capital markets being rebuilt onchain.

◢ Winners

✚ Ethereum: 58% of all tokenized RWA value. The institutional settlement layer thesis is no longer theoretical.

✚ Ondo — $2.5B TVL, largest pure-play RWA protocol, now tokenizing equities and ETFs

✚ @Securitize $3.3B under management, first broker-dealer approved to custody tokenized securities

✚ @plumenetwork: only L1 purpose-built for tokenized asset issuance with native DeFi composability

◢ Losers

Basically any protocol whose value proposition is primarily yield generation.

You're now competing against the US government's balance sheet.

@aave already knows this and their V4 Horizon platform is explicitly targeting $1B+ in institutional RWA deposits.

Protocols that don't adapt will watch TVL quietly migrate toward instruments offering T-bill yield with DeFi mechanics.

◢ Conclusions

Analysts project $100B in tokenized RWAs by end of 2026: a further 3-4x from here.

If that happens, "DeFi TVL" starts looking fundamentally different.

✚ Less algorithmic. Less reflexive.

✚ More institutional. More boring. More real.

RWAs aren't coming to DeFi. They're replacing what DeFi promised to be and delivering it better than DeFi ever did.

Is that the vision winning? Or the vision dying?

From X

Disclaimer: The above content reflects only the author's opinion and does not represent any stance of CoinNX, nor does it constitute any investment advice related to CoinNX.