“Where should I lend in DeFi?” is the wrong question.

The right question is: what kind of lender are you?

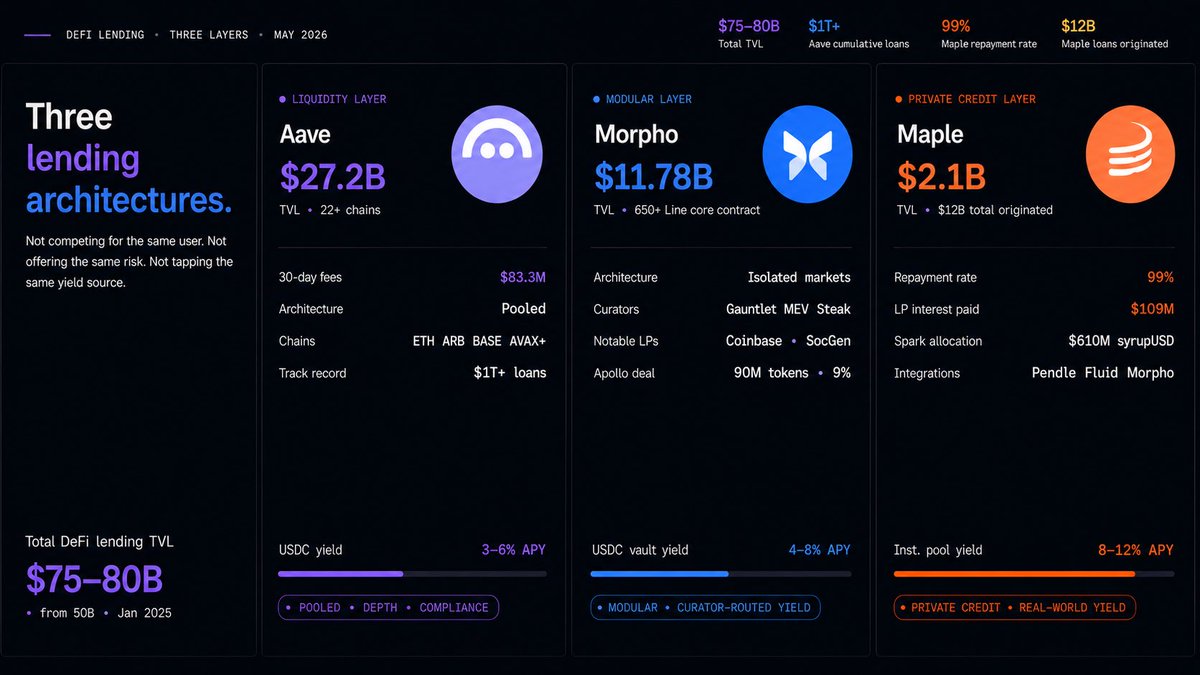

Because the three protocols that now dominate DeFi lending are not competing for the same user 👇

◢ Market Context

DeFi lending TVL crossed $75-80 billion in April 2026, up from $50 billion at the start of 2025.

✚ Aave crossed $1 trillion in cumulative loans, a first for the sector

✚ Morpho hit $11.78 billion in TVL on May 12, becoming the clear second-largest lending protocol

✚ Maple sits at $2.1 billion with a 99% repayment rate and $12 billion in total loans originated since 2021

Three protocols. Three architectures. Three different bets on DeFi lending.

◢ The Liquidity Layer: Aave

Aave is the benchmark.

✚ $27.2 billion in TVL

✚ 22+ chains

✚ $83.3 million in fees over the past 30 days

Its architecture is pooled: every USDC supplier earns the average rate generated by that pool’s borrowing demand.

Aave’s depth means large positions can move with minimal friction, while its multi-chain footprint gives access to markets across Ethereum, Arbitrum, Base, Avalanche, and more.

Current USDC yield: 3-6% APY depending on chain and utilization.

◢ The Modular Layer: Morpho

Morpho’s core contract is 650 lines of Solidity.

The architecture separates three functions other lending protocols bundle together:

✚ Market creation

✚ Risk curation

✚ Liquidity provision

Anyone can create an isolated market with custom parameters: loan asset, collateral asset, LTV ratio, oracle, and interest rate model.

Curators like Steakhouse Financial, Gauntlet, and MEV Capital assemble those markets into Vaults that optimize depositor yield.

USDC vault rates often run 4-8% APY, outperforming Aave on equivalent assets because capital is routed to stronger borrowing demand.

✚ Coinbase chose Morpho as infrastructure for its USDC lending product

✚ Apollo Global Management signed a 48-month agreement to acquire up to 90 million MORPHO tokens, around 9% of total supply

✚ Société Générale deploys through Morpho vaults

Choosing a vault means choosing a curator, and curator quality affects returns.

◢ The Private Credit Layer: Maple

Maple is not really competing with Aave or Morpho at the protocol level.

It is bringing institutional private credit onchain.

Capital providers supply stablecoins to professionally managed pools, while borrowers draw loans at pre-agreed rates with off-chain credit assessment and on-chain enforcement.

syrupUSD turns this into a permissionless entry point: deposit USDC and receive yield-bearing tokens backed by short-duration overcollateralized loans.

The numbers behind this model are unusual for DeFi:

✚ $12 billion in total loans originated since 2021

✚ $109 million in interest paid to LPs

✚ 99% repayment rate

✚ syrupUSD integrated with Spark, Morpho, Fluid, and Pendle

✚ Spark allocated $610 million to syrupUSD pools directly

Permissioned institutional pools sit around 8-12% APY, structurally higher because Maple accesses a different risk market.

◢ Three Lenders, Three Markets

The common mistake is applying a retail liquidity framework to a decision that requires understanding architecture.

✚ If your priority is depth, chain coverage, and zero setup: Aave

✚ If your priority is optimized stablecoin yield with professional risk management: Morpho, and spend 20 minutes choosing a curator

✚ If your priority is the highest available dollar-denominated yield with a defined risk model: Maple’s syrupUSD, or institutional pools if you qualify

The protocols are not interchangeable.

They were built for different users, risk models, and yield sources.

The $75-80 billion across DeFi lending is not one homogeneous pool of capital. It is three distinct markets running in parallel on the same rails.

Which layer is your capital actually in and why?

From X

Disclaimer: The above content reflects only the author's opinion and does not represent any stance of CoinNX, nor does it constitute any investment advice related to CoinNX.