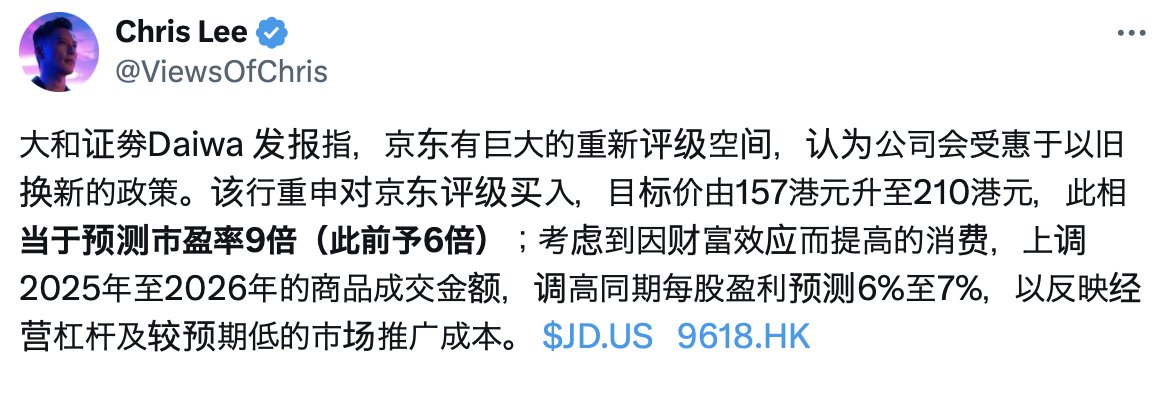

大和证劵Daiwa 发报指,京东有巨大的重新评级空间,认为公司会受惠于以旧换新的政策。该行重申对京东评级买入,目标价由157港元升至210港元,此相当于预测市盈率9倍(此前予6倍);考虑到因财富效应而提高的消费,上调2025年至2026年的商品成交金额,调高同期每股盈利预测6%至7%,以反映经营杠杆及较预期低的市场推广成本。 $JD.US https://t.co/tbMpyuRXLN

From X

Disclaimer: The above content reflects only the author's opinion and does not represent any stance of CoinNX, nor does it constitute any investment advice related to CoinNX.