$42 billion...

That's how much capital is locked in liquid staking protocols right now.

More than lending. More than DEXs. More than any other single category in DeFi.

Here's how $42 billion actually distributes 👇

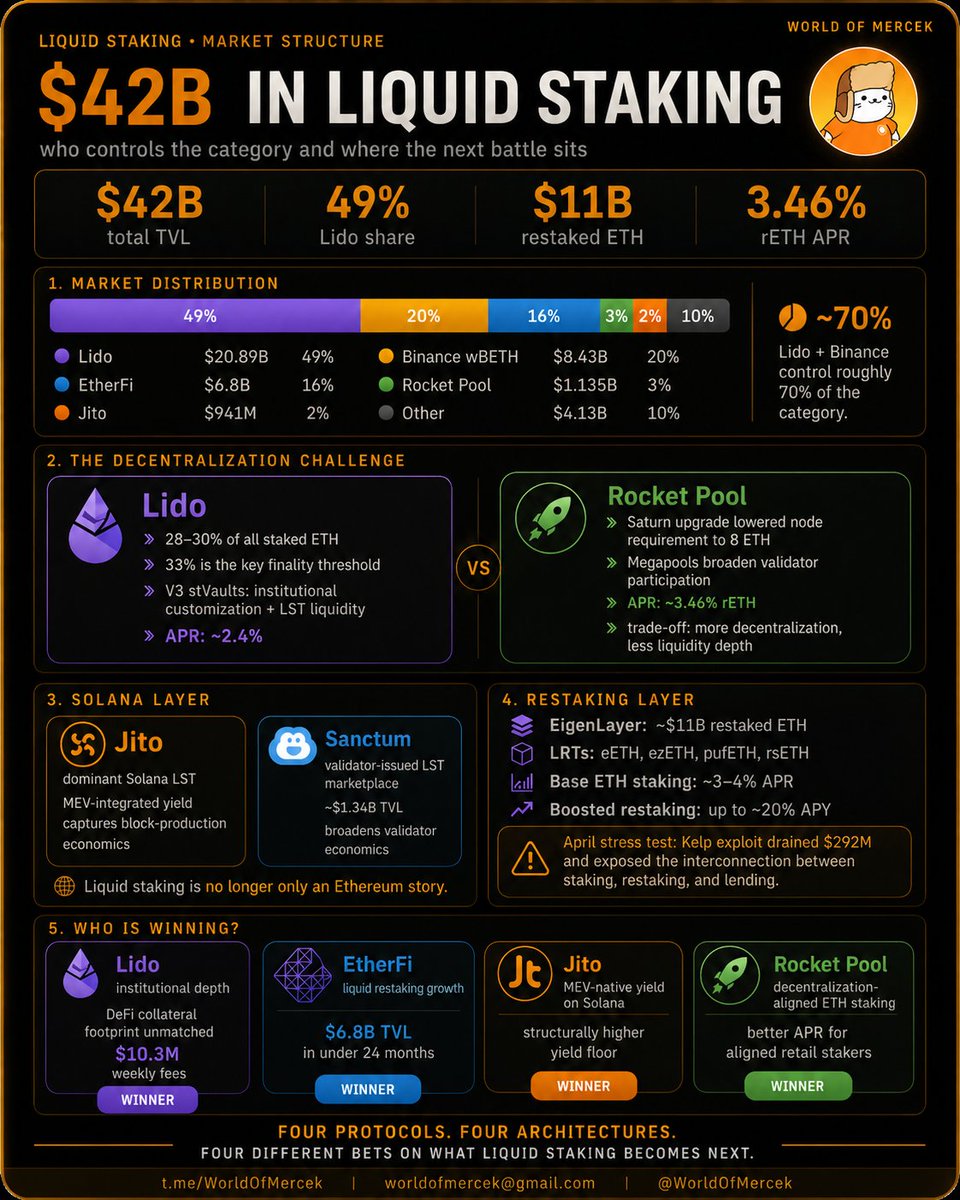

1️⃣ Market Distribution

@LidoFinance holds $20.89 billion: roughly 49% of the entire liquid staking market.

That's near-monopoly territory in a category worth $42 billion.

→ @binance Staked ETH (wBETH) sits second at $8.43 billion

→ @ether_fi at $6.8 billion

→ @Rocket_Pool at $1.135 billion

→ @jito_sol at $941 million in pure liquid staking TVL

The concentration at the top is more extreme than most DeFi analytics suggest.

Lido and Binance together control roughly 70% of the category. The remaining $12 billion is split across dozens of protocols.

That concentration is the most important structural tension in liquid staking right now and it's being actively contested from two directions simultaneously.

──────────────────────────────

2️⃣ Decentralization challenge

Lido controls an estimated 28-30% of all staked ETH on Ethereum.

Over dominance, this is a meaningful influence over Ethereum's validator set.

The Ethereum Foundation and core developers have raised this concern explicitly.

If Lido crosses 33% of staked $ETH, it gains theoretical influence over Ethereum's finality mechanism.

→ Lido's response is Lido V3: stVaults, a new architecture that allows large-scale institutional stakers to select specific node operators and customize their risk profile while maintaining LST liquidity.

It's a product designed to compete with solo staking from institutions who want customization without giving up composability.

Rocket Pool took the opposite approach.

→ The Saturn upgrade reduced the ETH requirement to run a node to 8 ETH and introduced megapools.

The result is a genuinely more decentralized validator set, at the cost of depth of liquidity.

→ Rocket Pool's rETH currently offers approximately 3.46% APR versus Lido's 2.4%.

──────────────────────────────

3️⃣ Solana layer

The Ethereum-centric view of liquid staking misses what's happening on Solana.

Jito is the dominant Solana liquid staking protocol and its differentiation is not just size.

→ Jito integrates MEV optimization directly into its staking mechanism, capturing additional value from transaction ordering and passing it back to JitoSOL holders on top of the base Solana staking yield.

That structural advantage guarantees yield from block production economics, not just consensus rewards and makes it a different product from stETH.

→ Sanctum's Validator LST model goes further.

Rather than a single monolithic LST, Sanctum lets individual Solana validators issue their own liquid staking tokens, creating a marketplace of LSTs at $1.34 billion TVL.

The model distributes validator economics across a much broader set of participants — and it's the most interesting architectural experiment in liquid staking that almost no one outside Solana is tracking.

──────────────────────────────

4️⃣ Restaking layer on top

EigenLayer represents $11 billion in restaked ETH

EtherFi's eETH, Renzo's ezETH, Puffer's pufETH, and Kelp's rsETH are all liquid restaking tokens: LSTs extended one layer further into AVS security.

→ Base Ethereum staking yields approximately 3-4% APR.

→ Restaking adds AVS rewards on top, paid in the AVS's own token

→ EtherFi has advertised up to 20% APY through boosted restaking

The Kelp DAO exploit in April was a stress test for exactly this architecture.

rsETH's cross-chain bridge vulnerability drained $292 million and triggered a $12 billion Aave TVL crash in a week.

The interconnection between liquid staking, restaking, and lending markets created cascading exposure that wouldn't have existed without the composability layer.

The DeFi United recovery fund and the Aave emergency response were the sector's response.

──────────────────────────────

5️⃣ Who is winning

The headline answer is Lido. The more interesting answer is that three different protocols are winning three different things simultaneously.

→ Lido is winning institutional depth: stETH is accepted as collateral on Aave, MakerDAO, Morpho, and dozens of lending protocols. It generates $10.3 million in fees every seven days. The DeFi integration footprint is unmatched.

→ EtherFi is winning the liquid restaking category: the only protocol that combines liquid staking, restaking, a crypto credit card, and institutional yield in a single product surface. It grew from near-zero to $6.8 billion in TVL in under 24 months.

→ Jito is winning the MEV-integrated yield category on Solana: a structurally higher yield floor than any Ethereum LST because it captures block production economics directly.

→ Rocket Pool is winning the decentralization-aligned ETH staker: and quietly delivering a better APR than Lido for retail participants who understand the product.

Lido, EtherFi, Jito, Rocket Pool are four different bets on what liquid staking becomes.

Which one is building for the cycle after this one?

From X

Disclaimer: The above content reflects only the author's opinion and does not represent any stance of CoinNX, nor does it constitute any investment advice related to CoinNX.