Notes

PENTAGON TARGETS CHINESE COMPANIES SUPPORTING MILITARY

The Pentagon has added several Chinese firms to its list of companies aiding the military:

Alibaba ( $BABA)

BYD ( $BYDDY)

Baidu ( $BIDU)

COSCO ( https://t.co/G9gsxivi0B)

Huawei (private)

NIO Inc ( $NIO)

📅 02월 09일 (월) 20:40 기준 | 주요 소식 정리

1️⃣ 홍콩, 지미 라이 20년형: 일국양제(一國兩制)의 종언과 투자 환경의 변모

• 홍콩의 저명한 민주화 운동가이자 언론인인 지미 라이(黎智英) 애플데일리 창업주에게 20년의 중형이 선고됨. 이는 홍콩 국가보안법 시행 이래 가장 주목받았던 사건 중 하나로, 과거 홍콩의 자유와 자치를 상징하던 인물에 대한 직접적인 탄압 사례임이 명백함. 베이징이 홍콩에 대한 통제를 강화하는 가운데, ‘일국양제’(一國兩制) 원칙의 실질적 붕괴를 보여주는 상징적 사건으로 평가됨.

• 라이는 외국 세력과의 공모 및 선동 혐의로 기소되어 총 20년의 징역형을 받음. 국가보안법 위반 혐의는 최대 무기징역까지 가능한 중대 범죄로 취급되며, 이번 판결은 홍콩 사법부가 독립성을 상실하고 중국 본토의 영향력 아래 있음을 시사하는 강력한 증거로 인식됨. 그의 언론사 애플데일리 역시 이미 폐간된 상태이며, 이는 홍콩 내 비판적 목소리를 제거하려는 의도가 확고함.

• 이번 판결은 홍콩의 법치주의와 언론의 자유가 심각하게 훼손되었음을 국제사회에 다시금 각인시킴. 장기적으로 홍콩이 아시아의 주요 금융 허브로서 가졌던 매력을 크게 감소시킬 것이며, 예측 불가능한 정치적 리스크는 서방 투자자들의 자본 이탈을 가속화하는 요인으로 작용할 전망임. 기업들은 이제 홍콩에서의 사업 지속 가능성에 대해 근본적인 의문을 제기하게 될 것이며, 이는 홍콩 경제 전반에 부정적 파급 효과를 야기함.

• 관련 섹터: 홍콩 증시 및 관련 상장지수펀드, 중국 기술주, 국제 금융 서비스 허브 관련 자산.

────────────────

2️⃣ 우크라이나-폴란드 연루 주장, 지정학적 위험 고조

• 러시아 연방보안국(FSB)이 러시아군 총정찰국(GRU) 고위 간부 암살미수 사건의 배후로 우크라이나와 폴란드를 지목하며 파장을 일으키는 모습임. 이번 주장은 단순히 우크라이나를 넘어 NATO 회원국인 폴란드까지 직접적으로 연루시켰다는 점에서 기존의 갈등 수준을 한층 격상시키는 시도로 풀이됨. 국제사회의 긴장감이 고조되는 상황임.

• FSB는 이번 사건이 우크라이나의 지시 하에 이루어졌으며, 폴란드 정보기관이 개입했다고 구체적으로 주장함. 러시아 내부 고위층에 대한 공격 시도와 NATO 회원국의 직접 개입 가능성 제기는 단순한 선전전을 넘어 실질적인 보복 조치나 외교적 충돌로 이어질 수 있는 명분을 제공하는 측면이 있음. 이는 동유럽 안보 지형에 새로운 불확실성을 가중시키는 요인으로 작용함.

• 이러한 러시아의 주장은 에너지 시장에 즉각적인 불안 요인으로 작용할 수 있음. 특히 유럽의 에너지 안보에 대한 우려가 커지며, 원유 및 천연가스 가격의 변동성 확대를 야기할 수 있음. 또한, 동유럽 전반의 지정학적 리스크가 증대됨에 따라 글로벌 방산 기업들에 대한 관심은 더욱 커질 것이며, 안전자산 선호 심리가 강화되는 흐름을 보일 것으로 예상됨. 투자자들은 단기적인 시장 변동성 확대에 대비할 필요가 있음.

• 관련 섹터: 에너지, 방산, 원자재

────────────────

3️⃣ 1조 달러 증발 후 대형 기술주 부유(浮遊), AI 지출 우려 심화됨

• 지난 한 주간 AI 하이퍼스케일러를 포함한 대형 기술주들이 1조 달러에 달하는 시가총액 증발을 경험하며 투자 시장의 냉정한 현실에 직면함. AI 성장 기대감에 취해 있던 시장이 막대한 지출 부담이라는 그림자에 주목하기 시작한 모양새임.

• CNBC에 따르면, 이들의 주가는 한 주 만에 1조 달러 이상 증발하며 투자자들의 불안감을 극명하게 드러냄. 이는 단순한 조정을 넘어, 그간 AI 기술의 맹목적 낙관론 뒤에 가려져 있던 천문학적인 투자 비용에 대한 시장의 냉철한 시각이 반영된 결과로 보임.

• 결국 AI 기술 개발 및 인프라 구축에 요구되는 막대한 자본 지출이 해당 기업들의 수익성을 압박할 수 있다는 우려가 표면화된 것임. 이러한 현상은 단기적 변동성을 넘어, 향후 AI 관련 기업 투자에 있어 성장성뿐 아니라 비용 효율성까지 종합적으로 고려해야 할 필요성을 시사함. 투자 심리 위축과 함께 향후 AI 관련 기업들의 옥석 가리기가 더욱 심화될 것으로 전망됨.

• 관련 섹터: AI 인프라, 클라우드 컴퓨팅, 반도체, 데이터센터

────────────────

4️⃣ 다카이치 승리와 일본 증시의 기만적 랠리

• 다카이치 총리의 압도적인 선거 승리 소식에 일본 증시가 사상 최고치를 경신함. 이는 총리가 수십 년 만에 최대 다수 의석을 확보하며 안정적인 국정 운영 기반을 마련했음을 의미함. 시장은 이러한 정치적 안정성을 긍정적으로 해석하며 즉각적인 랠리를 보인 것으로 분석됨.

• 구체적인 상승 폭은 명시되지 않았으나, '사상 최고치 경신'이라는 표현에서 시장의 강한 반응을 엿볼 수 있음. 이는 다카이치 내각이 강력한 정책 추진력을 가질 것이라는 기대감이 투영된 결과임. 과거 아베노믹스와 같은 확장적 정책 기조의 재현 가능성에 대한 막연한 희망이 작용한 것으로 판단됨.

• 그러나 표면적인 증시 강세는 일시적인 투자 심리 개선에 불과할 수 있음. 근본적인 경제 구조 개혁과 지속 가능한 성장 동력 확보 없이는 단순한 유동성 랠리에 그칠 위험이 상존함. 정치적 안정성이 곧 기업 실적 개선으로 이어질지는 미지수이며, 과도한 낙관론은 경계할 필요가 있음.

• 관련 섹터: 일본 증시 전반, 정책 수혜주, 대형 수출 기업

────────────────

출처 : CNBC, 블룸버그, 연합뉴스, 파이낸셜타임즈

#미국주식 #속보 #경제 #SK하이닉스 $EWJ #SK이노베이션 $XOM #한화에어로스페이스 $NVDA $MSFT $TSLA $META $HSI $TCEHY $AMZN $BABA $GOOGL $LMT #삼성전자

Diversify like never before with Gate.

Gate ETF, Convert, Trading Bots, Margin Trading, Earn, and Auto-Invest now fully support stock and metal tokens.

🔹 Covers $XAUT, $PAXG, $NVDA, $TSLA and more

🔹 Perpetuals available with 1–10x leverage on $JPM, $BABA, and $ACN, settled in $USDT

Expand your portfolio diversity on Gate.

Learn more: https://t.co/1hCDXg14U0

$WMT +3.5%, hits new ATH after recent partnership with @Google.

$BABA +4.3% as Qwen reached over 700M+ downloads.

$SOUN +4.7% due to renewed investor interest in AI-related stocks.

JUST IN: David Tepper via Appaloosa just released his new positions:

He reduced his $BABA, $AMZN, $GOOGL $JD, $MSFT, $PDD positions.

Added $TSM, $AMD, $BIDU, $QCOM, $KWEB, $WHR.

See the full list on Unusual Whales:

WEDBUSH’S DAN IVES RELEASED THE “IVES AI 30,” FEATURING TOP AI PLAYS:

🔸 Hyperscalers: $MSFT, $GOOGL, $AMZN, $ORCL

🔸 Software: $PLTR, $CRM, $IBM, $NOW, $SNOW, $PEGA, $MDB, $SOUN, $INOD

🔸 Consumer Internet: $BABA, $AAPL, $META, $BIDU, $RBLX

🔸 Cybersecurity: $PANW, $ZS, $CRWD

🔸 Autonomous/Robotics & Power: $TSLA, $OKLO, $GEV

🔸 Semiconductors/Hardware: $NVDA, $AMD, $TSM, $AVGO, $MU, $NBIS

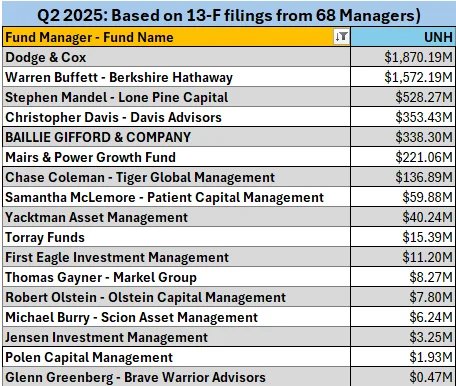

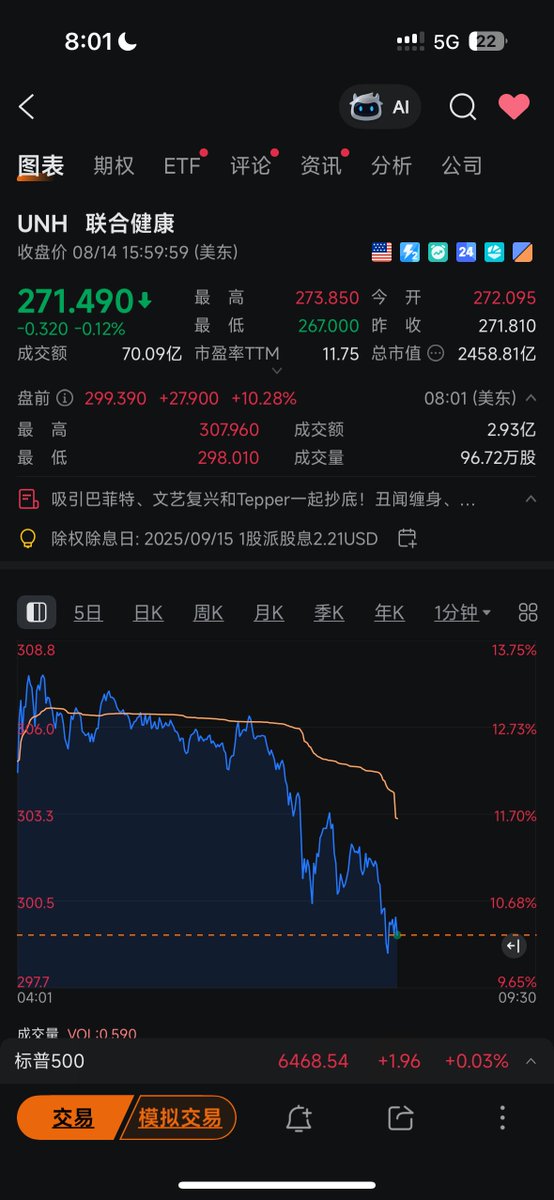

最近美股机构的13F报告集中披露,巴菲特公司伯克希尔,逆势抄底了联合健康(#UNH)深受瞩目,受此消息刺激,联合健康股价在今天盘前大涨10%,收回300美金以上。我决定今晚跟一手巴菲特的操作。🧐

今天在看美股机构13F报告时候,发现一个挺有意思的现象——市场大部分人避之不及,可巴菲特、David Tepper、文艺复兴、Michael Burry、沙特PIF这些大佬都在抄底。伯克希尔甚至是时隔14年重新杀回医疗保险板块,一口气买了504万股,价值15.7亿美元。

为什么我决定今晚跟一手呢?因为这帮老狐狸肯定不是为了短线博反弹,而是觉得这公司在被错杀。

📊先看 #UNH 基本面:

规模:美国最大医疗保险公司,2024年收入4003亿美元,净利润144亿美元,这规模在美股医疗板块里基本是“航空母舰”级别。

盈利能力:过去15年,分红每年都涨,而且盈利稳定——这是典型的“防御型现金牛”。

估值:现在的股价回到2020年的水平,市盈率只有12倍——这种龙头公司在正常市场环境下,保守预估20倍不算离谱。

我举个最直观的栗子🌰:

如果2003年底你花1万美元买了 #UNH,哪怕算上最近的暴跌,今天这笔钱大约还能变成10万美元,中途分红全程上调。要是暴跌前收益表现更佳,预估是18万美元。这种长期稳定复利能力,是真正的机构偏好标的。

📝#UNH 为什么暴跌?

这波下杀不是因为财务崩了,而是市场对风险的预期陡然升高:

1️⃣潜在刑事调查:司法部在查它,虽然公司说“充满信心”,但这种事一旦升级,可能影响合同、信誉。

2️⃣业绩指引暂停:7月公司直接取消年度业绩展望,还甩锅说“医疗需求激增导致环境突变”,这会让投资者觉得不确定性大增。

3️⃣高层变动:CEO Andrew Witty突然辞职(个人原因),临危换回老将Hemsley。换帅往往是风险信号,尤其是遇到监管风暴时。

4️⃣政策压力:美国政府削减医疗支出,医疗成本上涨,这对保险公司是双杀。

5️⃣网络安全和公众形象:网络攻击、CEO被枪杀这种黑天鹅事件,虽然和核心财务没直接关系,但对品牌和舆论压力不小。

我的抄底逻辑,其实很简单,首先肯定是这些大佬开始抄底了,给了我充足的信心支持。另外估值的确是便宜,虽然利空也不少,刑事调查、指引暂停、政策不确定性,这些事对股价冲击,已经实质性表现出来,也算消化的七七八八了,毕竟股价从600+跌下来的。

因为我个人是偏好价值长线投资,假如您跟我一样,是那种5年以上视野的价值投资者,这种时刻往往是布局的好机会。因为 #UNH 的基本盘——医疗保险的刚需性、行业龙头地位、庞大会员基础——没变。美国人口老龄化趋势还在,长期医疗需求只会更高。所以中长期来看,是相对确定性比较高的!

我觉得现在买 #UNH 有点像2008年买强生(#JNJ)——短期麻烦多、市场不爱,但长线可能是最甜的果子。跟随大佬们,用时间和耐心等市场情绪修复。🧐

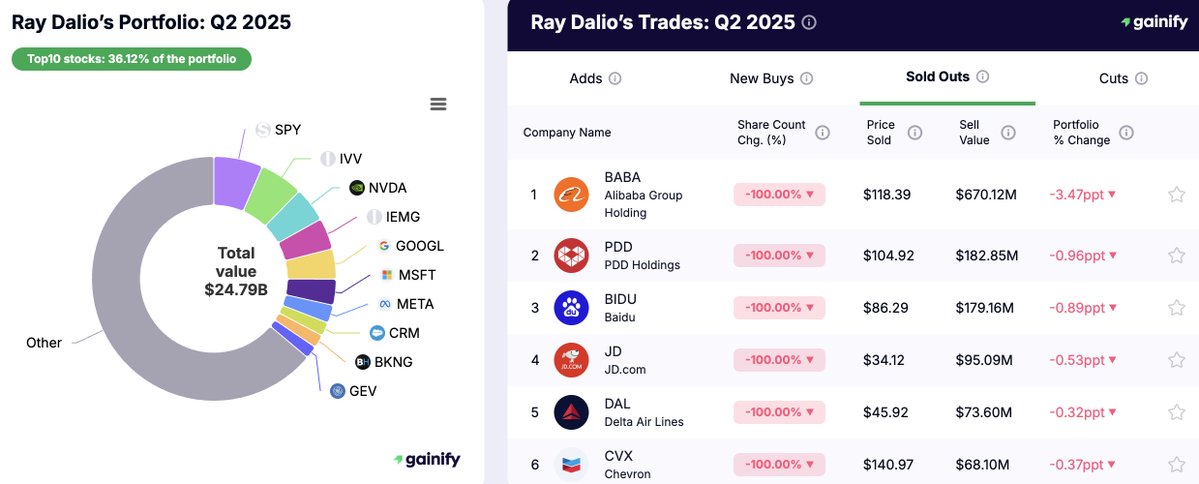

桥水清仓中概股的新闻,今天在各个金融群炸锅了,毕竟我也是买了桥水在中国的基金,华润创意桥云9号,今年业绩十分突出,有40%+回报率。但突然主体基金清仓中国的策略,让人始料未及!

我们仔细研究了Ray Dalio 这次 Bridgewater 2025年二季度的13F报告,简单一句话来看:老爷子这是彻底“弃船”中国互联网股,转头一头扎进了美股 AI 巨头的怀抱。

1️⃣彻底撤出中国互联网

Bridgewater 直接清仓了 $BABA 、 $PDD 、 $BIDU 、 $JD ,套现大约 11.3 亿美金。

这不只是“减仓”,这是“清空冰箱”式的退出。

在我看来,原因可能有三:

• 中国经济复苏不及预期,消费、出口两头承压

• 政策不确定性高,尤其是平台经济监管阴影尚存

• 美股这边 #AI 赛道收益率太诱人,机会成本太高

换句话说,Dalio 不是觉得中国没潜力,而是觉得短期内资本效率太低,不如直接把钱放到能立刻跑起来的赛道,尤其是 #AI 领域。

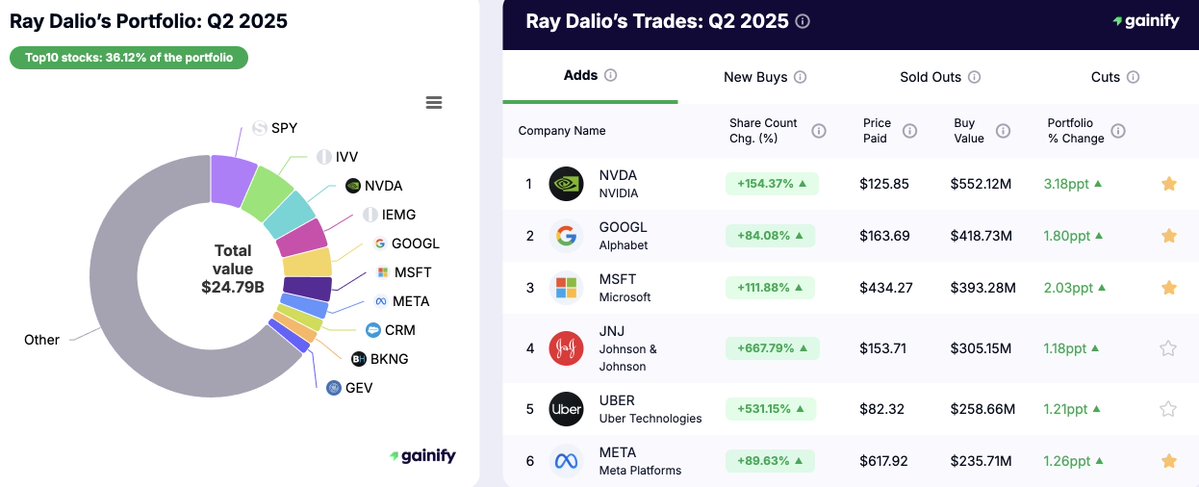

2️⃣重仓 #AI 和美股科技巨头

这季度的增持动作可以用“暴力”来形容:

• $NVDA 加了 154%,一下多了 5.52 亿美金,现在成了第三大持仓

• $MSFT 加了 3.93 亿

• $GOOGL 加了 4.18 亿

• 甚至 $UBER 也猛加 5.31 倍

这个组合直接把 #AI 核心硬件( $NVDA )+ AI 应用平台( $MSFT 、 $GOOGL 、 $META )绑成一个战车,明显是押注未来 3-5 年的 #AI 基础设施浪潮。而且 $Uber 也很有意思,说明他们看好 #AI 在出行、物流等实际场景的渗透。

3️⃣ETF 还是核心底仓,但开始“修剪”

虽然 $SPY 、 $IVV 、 $IEMG 还是大仓位,但 Dalio 这次减了 SPY 21.9%,套了 4.52 亿美金。

这是一种“从大水池里舀水出来,倒进 #AI 桶里”的操作。ETF 作为被动收益的底仓还在,但加了更多主动进攻型仓位。

整体思考来看,目前A股3700点,恒生25270点,标普500 6468点,美股目前历史高位,如此大力度加仓美股,撤出中国市场,说明以桥水为代表的外资,短期在中国市场看不到正向回报,就不占着资金池。而此刻这种历史高位,全面加码 #AI 赛道,把资金集中到最具确定性、最受资金追捧的核心标的上,这种抓大放小的策略,也是值得深思。作为全天候策略,依旧保留ETF被动敞口,用ETF来保底,防止单一赛道波动太大。投资组合上,攻守平衡,既追 #AI 大趋势,又保留防守余地!值得学习借鉴🧐